Driving Simulator Market Summary

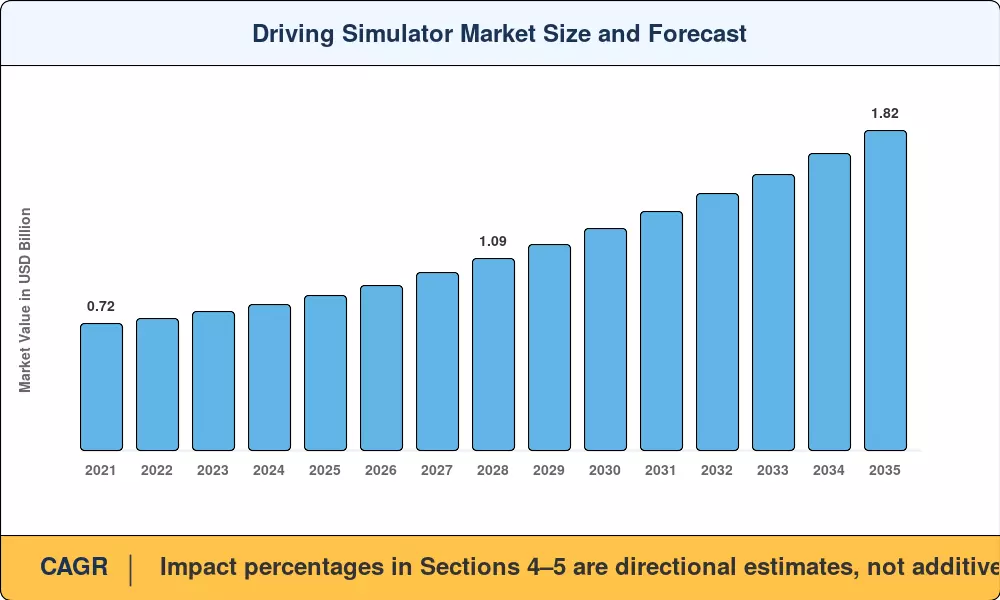

The driving simulator market was valued at USD 0.88 billion in 2025 and is projected to reach USD 0.94 billion in 2026 before climbing to USD 1.82 billion by 2035, expanding at a CAGR of 7.6% over the forecast period (2026–2035). Two forces are accelerating this trajectory: tightening road-safety certification mandates—particularly the EU's revised Directive 2006/126/EC and India's Motor Vehicles (Amendment) Act 2019—and the automotive industry's pivot toward virtual validation of advanced driver-assistance systems [1]. Commercial fleet operators spent an estimated USD 2.3 billion globally on driver training infrastructure in 2024, and a growing share of that budget now flows into simulation-based programs that compress recruitment timelines from weeks to days [2].

There’s a technical inflection point that’s changing the way driving simulations are designed and delivered. Motion-cueing rigs, real-time physics engines, digital-twin road networks and cloud-streamed scenario libraries are replacing legacy fixed-base platforms with simple visual rendering. In 2024 alone, OEMs, such as BMW and Stellantis, announced R&D investments of more than USD 400 million in total for software-in-the-loop test beds, indicating that the testing on virtual tracks will supplement—and in many cases replace—physical proving grounds in the next decade [3].

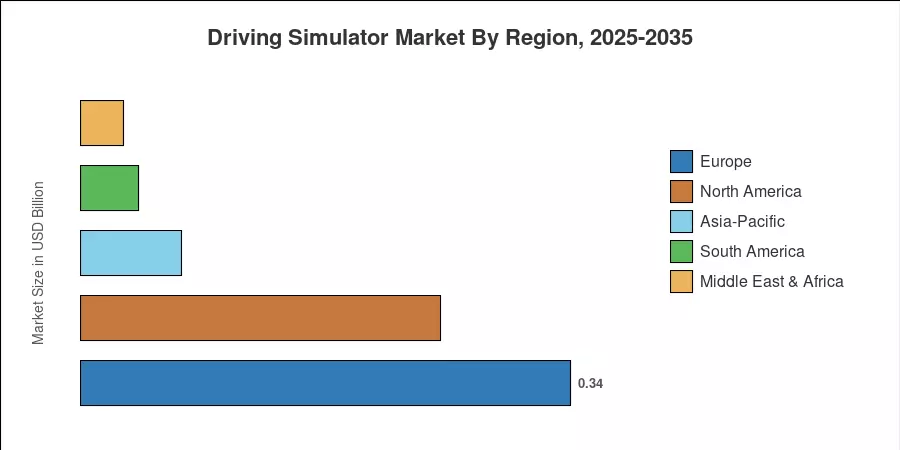

Europe accounts for over 39% of the driving simulator industry, owing to the presence of Germany’s automotive OEM cluster and the extensive regulatory environment for driver licensing on the continent. Asia-Pacific is the fastest-growing market with a predicted CAGR of 7.65%, attributable to the developing logistics networks in China and India. North America has the second-highest proportion, at about 28%, driven by the FMCSA-mandated entry-level driver training requirements for commercial vehicle operators [4]. With autonomous-vehicle validation roadmaps ramping up in all three areas, the driving simulator industry should experience sustained double-digit investment growth through the mid-2030s.

Key Report Takeaways

• By Vehicle Type

- Passenger cars accounted for 64% of the driving simulator market in 2025, reflecting high volumes of learner-driver and OEM R&D simulation demand.

- Commercial vehicles are forecast to post the fastest segment CAGR of 7.6% through 2035, fueled by fleet-operator training mandates.

• By Application

- Training represented 54% of the driving simulator market share in 2025, underpinned by driving-school adoption across Europe and Asia-Pacific.

- Testing and research will expand at a 7.7% CAGR as OEMs shift validation workloads from physical tracks to simulation environments.

• By Geography

- Europe led the driving simulator market with a 39% revenue share in 2025.

- Asia-Pacific is advancing at the fastest regional CAGR of 7.65% toward 2035.

Driving Simulator Market Size and Forecast (2021–2035)

Market Research Future (MRFR) employs a triangulation of primary research interviews with tier-1 simulator OEMs, regulatory filings from transport ministries across 28 countries, and revenue-weighted analysis of publicly listed simulation technology businesses in its forecasting methodology. Historical figures are based on verifiable firm financials and import/export databases, and forecasts use a bottom-up build based on segment-level demand models.