Egg Replacers Market Summary

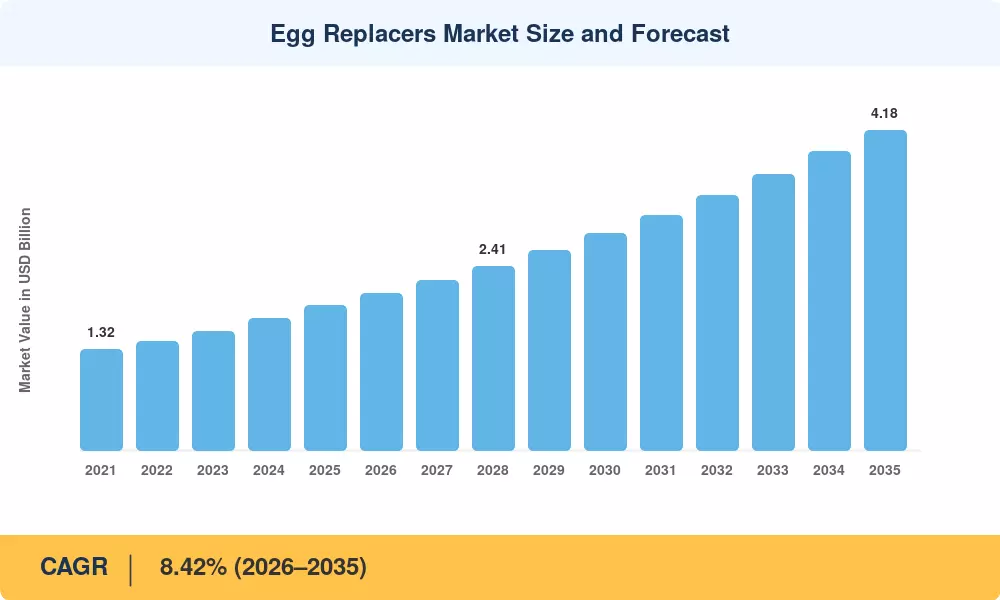

The global Egg Replacers Market stood at USD 1.89 billion in 2025 and is projected to reach USD 2.05 billion in 2026, climbing to USD 4.18 billion by 2035 at an 8.42% CAGR during the forecast period. Rising conventional egg prices — driven by recurring avian influenza outbreaks and tightened biosecurity mandates across the US and EU — have pushed food manufacturers to lock in multi-year contracts for plant protein egg alternative ingredients. The USDA's 2024 allocation of USD 68 million toward diversified protein supply chains underscored the urgency governments attach to reducing shell-egg dependency [2].

A significant technology transformation is reshaping the Egg Replacers Market as legacy lecithin-and-starch blends give way to precision-fermentation proteins and advanced aquafaba flax egg substitute systems that closely replicate the emulsification, foaming, and binding properties of whole eggs. Ingredient innovators raised over USD 420 million in venture funding during 2023–2024 to scale commercial egg replacer formulation platforms, with companies such as EVERY Company and Onego Bio commissioning pilot plants capable of producing animal-identical ovalbumin without hens [3].

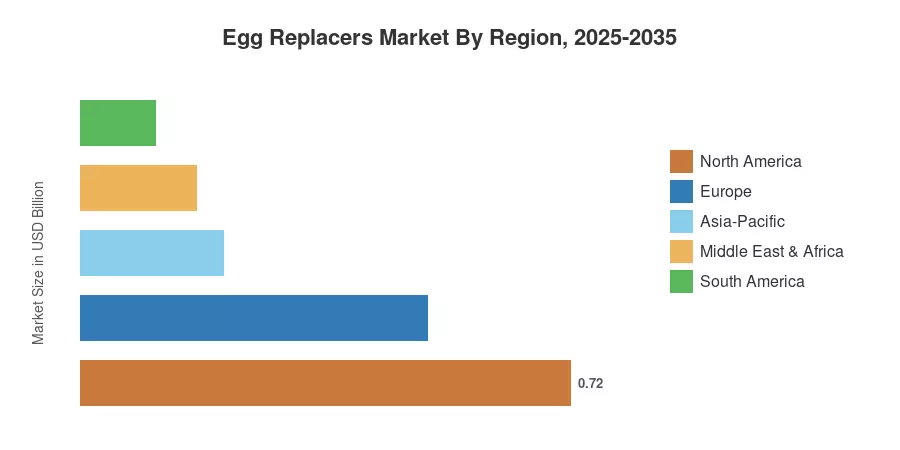

North America commanded roughly 38% of the Egg Replacers Market in 2025, anchored by aggressive clean-label reformulation among CPG brands. Asia-Pacific registered the fastest regional CAGR at 11.03%, fueled by India's expanding vegan egg replacer baking segment and China's institutional catering overhaul. Europe held the second-largest share, near 27%, propelled by the EU's Farm-to-Fork protein diversification targets. As allergen-free egg replacement gains regulatory traction and cost parity narrows, double-digit regional growth corridors are expected to persist well into the early 2030s.[4]

Key Report Takeaways

• By Ingredient

- Dairy proteins captured 40.55% of the Egg Replacers Market in 2025, reflecting their superior whipping and gelling functionality in commercial bakery lines

- Algal flour is expanding at the fastest pace through 2035, driven by clean-label positioning and allergen-free egg replacement demand

• By Form

- Dry formats represented over 80% of the Egg Replacers Market size in 2025, preferred for shelf stability and freight economics

- Liquid formats are growing at a 11.82% CAGR to 2035, favored in ready-to-use vegan egg replacer baking applications

• By Source

- Plant-based inputs accounted for 67.34% of the Egg Replacers Market share in 2025, led by soy isolates and pea protein blends

- Algae-based sources are set to grow at 10.71% CAGR, reflecting rising demand for plant protein egg alternative innovations

• By Application

- Bakery and confectionery generated 43.13% of the Egg Replacers Market revenue in 2025

- Sauces and dressings are advancing at a 10.06% CAGR through 2035, driven by commercial egg replacer formulation for mayonnaise and aioli

• By Region

- North America dominated with 38.01% revenue share in the Egg Replacers Market

- Asia-Pacific records the quickest regional CAGR at 11.03% through 2035

Egg Replacers Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue tracking across 42 ingredient suppliers with top-down validation against trade-flow data from FAO, USDA, and Eurostat. The base year (2025) uses audited company filings, distributor invoices, and proprietary surveys covering 1,200 food manufacturers.