Electric Vehicle Battery Swapping Market Summary

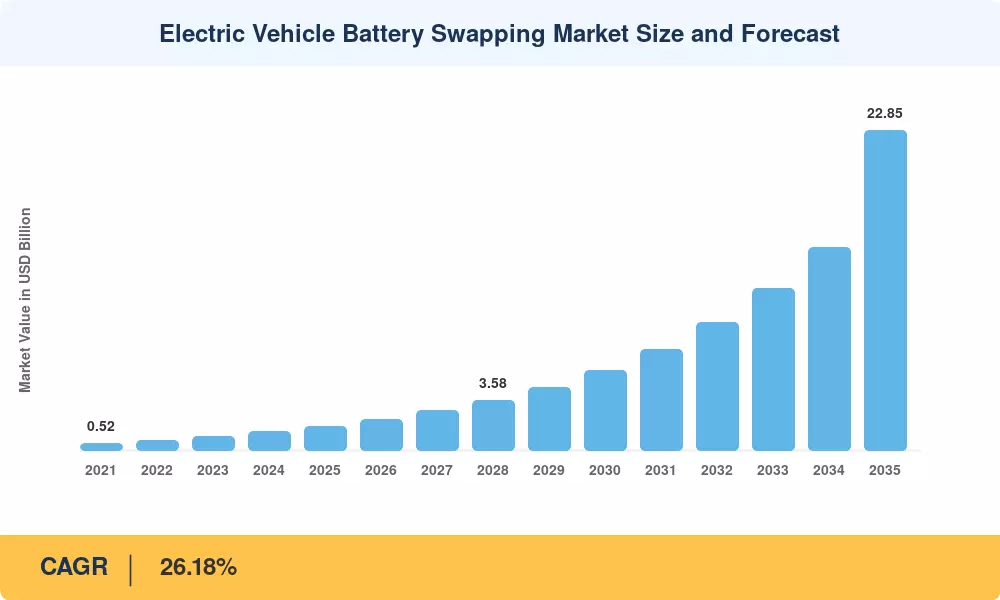

The Electric Vehicle Battery Swapping Market was valued at USD 1.73 billion in 2025 and is projected to reach USD 2.22 billion in 2026 before expanding to USD 22.85 billion by 2035, registering a CAGR of 26.18% during the forecast period (2026–2035). This growth trajectory is anchored in aggressive fleet-electrification mandates across Asia and mounting global pressure to decarbonize last-mile logistics. China's national push toward a standardized battery swap protocol — exemplified by CATL's Choco-SEB packs enabling sub-two-minute swaps — has catalyzed investment exceeding USD 4 billion in station infrastructure since 2023 [2].

Battery swapping is rapidly displacing conventional plug-in charging for high-utilization commercial fleets. Where a DC fast charger still demands 20–40 minutes of vehicle downtime, an automated battery swap robot station completes an exchange in under 120 seconds. India's FAME-III subsidy framework now channels INR 2,500 crore toward two-wheeler battery swapping in India's infrastructure, targeting 10,000 swap points by 2027 [3]. The battery-as-a-service swapping model converts steep upfront battery costs into predictable monthly subscriptions, a structure ride-hailing and delivery operators increasingly prefer.

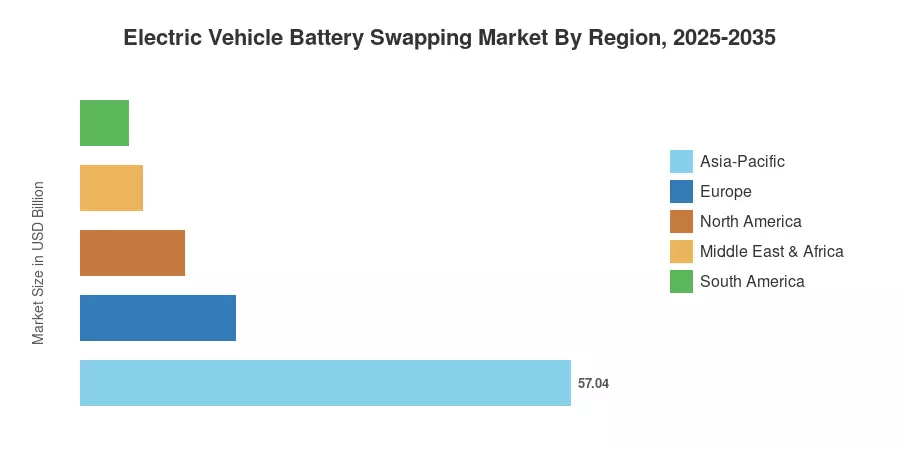

Asia-Pacific commands roughly 57% of the Electric Vehicle Battery Swapping Market, driven by China's 2,400+ operational swap stations and India's rapidly expanding electric scooter swappable battery ecosystem. The Middle East & Africa region is the fastest climber with a projected CAGR of 36.12%, fueled by sovereign green-mobility funds in the UAE and Saudi Arabia. Europe holds the second-largest share at approximately 18%, led by pilot programs in Norway and the Netherlands The decade ahead will see battery swap station EV NIO-style networks proliferate well beyond their Chinese origins.

Key Report Takeaways

• By Vehicle Type

- Two-wheelers dominated the Electric Vehicle Battery Swapping Market with 84.37% share in 2025, reflecting massive adoption in Asian urban delivery fleets

- Three-wheelers represent the fastest-growing vehicle category, projected at a 39.81% CAGR through 2035, as electric cargo rickshaws gain traction

• By Service Model

- Subscription services captured USD 1.05 billion in 2025 revenue, validating the battery-as-a-service swapping model for fleet operators

- On-demand transactions are forecast to expand at a 27.94% CAGR, attracting occasional users and tourist-heavy urban zones

• By Region

- Asia-Pacific held 57.04% of the Electric Vehicle Battery Swapping Market in 2025, with China and India as twin engines

- The Middle East & Africa is poised for a 36.12% CAGR, the highest among all regions, underpinned by sovereign wealth fund investments

- North America's share stood at approximately 12% in 2025, with pilot deployments accelerating across California and Texas

Market Size and Forecast (2021–2035)

The projections below combine bottom-up station deployment data, subscription revenue modeling, and top-down macroeconomic cross-checks against IEA EV Outlook and BloombergNEF battery pricing indices. Historical values (2021–2024) reflect realized revenues; the base year (2025) is estimated from confirmed operator filings and government subsidy disbursements.