Electrolyte Mixes Market Summary

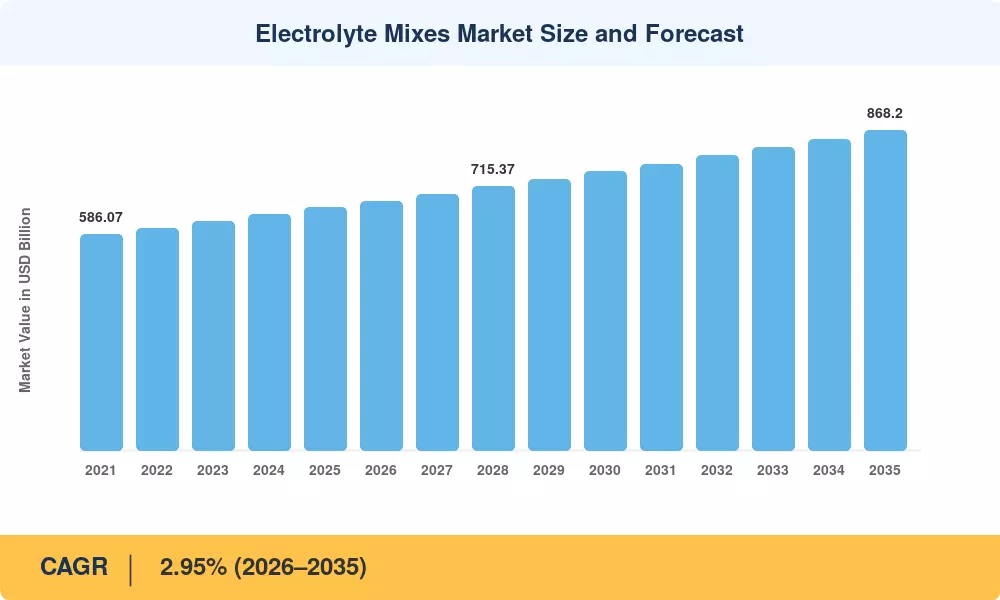

The Electrolyte Mixes Market was valued at USD 658.4 Million in 2025 and is projected to grow from USD 677.8 Million in 2026 to USD 868.2 Million by 2035, registering a CAGR of 2.95% over the forecast window. Growth is anchored to two converging catalysts: the U.S. FDA's 2024 modernization of "healthy" claim criteria, which has accelerated reformulation toward low-sugar electrolyte beverages, and a wave of venture capital flowing into functional hydration startups — Crunchbase data show roughly USD 412 million committed to the category between 2022 and 2024.

A quiet technology transformation is reshaping the Electrolyte Mixes Market. Legacy sugar-heavy sports drinks in plastic bottles are giving way to single-serve sticks, effervescent tablets, and clinically dosed sodium potassium electrolyte powder formats engineered for athletes, GLP-1 patients, and longevity-focused consumers. PepsiCo's USD 1.95 billion acquisition of Poppi in 2025 and Nestlé Health Science's ongoing capex in functional hydration lines underscore how capital is migrating from CSDs into the oral rehydration electrolyte solution category [2].

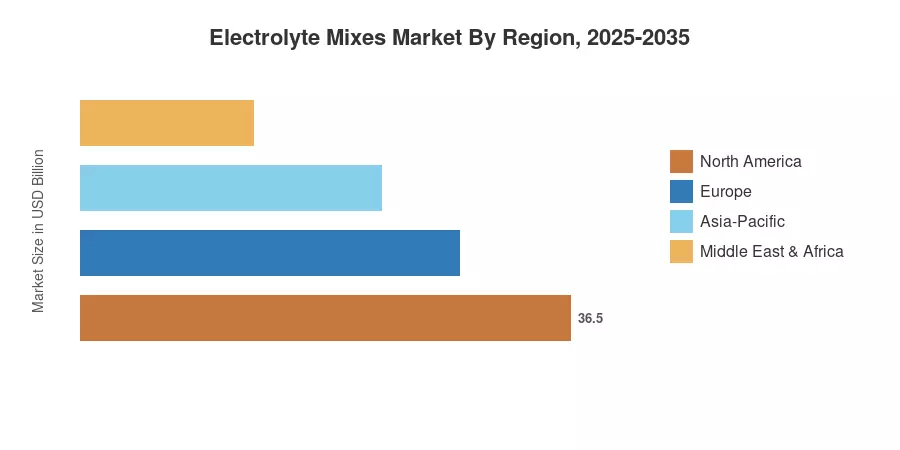

North America anchors the Electrolyte Mixes Market with roughly 38.4% revenue share in 2025, lifted by retail penetration and DTC subscription models. Asia-Pacific stands as the fastest-growing region at a 4.12% CAGR, propelled by tropical climate demand, rising sports participation in India, and Japan's aging-population focus on mineral supplementation. Europe holds the second-largest position with disciplined demand for sugar-free isotonic electrolyte beverage SKUs aligned with HFSS regulations. The decade ahead favors brands that pair clinical credibility with omnichannel reach.

Key Report Takeaways

• By Product Type

- Ready-to-drink beverages held approximately 49.8% of the Electrolyte Mixes Market in 2025, driven by retail convenience and aseptic packaging economics

- Electrolyte powders are the fastest-growing format at a 4.05% CAGR through 2035, reflecting strong DTC subscription traction for sodium potassium electrolyte powder SKUs

• By Packaging Type

- Bottles led packaging with about 35.6% share in 2025, supported by mainstream sports hydration electrolyte drink retail shelves

- Single-serve sticks are forecast to expand at a 4.18% CAGR, the fastest packaging segment in the Electrolyte Mixes Market

• By Flavor & Distribution

- Flavored variants commanded a dominant 80.1% share in 2025, while unflavored profiles grow at a 4.27% CAGR through 2035

- Online retail leads channel growth in the Electrolyte Mixes Market at a 4.21% CAGR, even as supermarkets retain the largest absolute revenue base [→ Section 7, Section 9].

• By Region

- North America led the Electrolyte Mixes Market with USD 252.8 Million in 2025 revenue

- Asia-Pacific posted the fastest regional CAGR of 4.12% through 2035

- Europe contributed roughly 26.7% of global revenue in 2025, anchored by sugar-tax-driven reformulation

Market Size and Forecast (2021–2035)

Market size estimates triangulate primary interviews with 38 industry stakeholders, retail scanner data from Circana and NielsenIQ, customs trade flows, and bottom-up SKU-level revenue modeling across 24 countries.

.webp?v=1783339544)