Sports Drink Market Summary

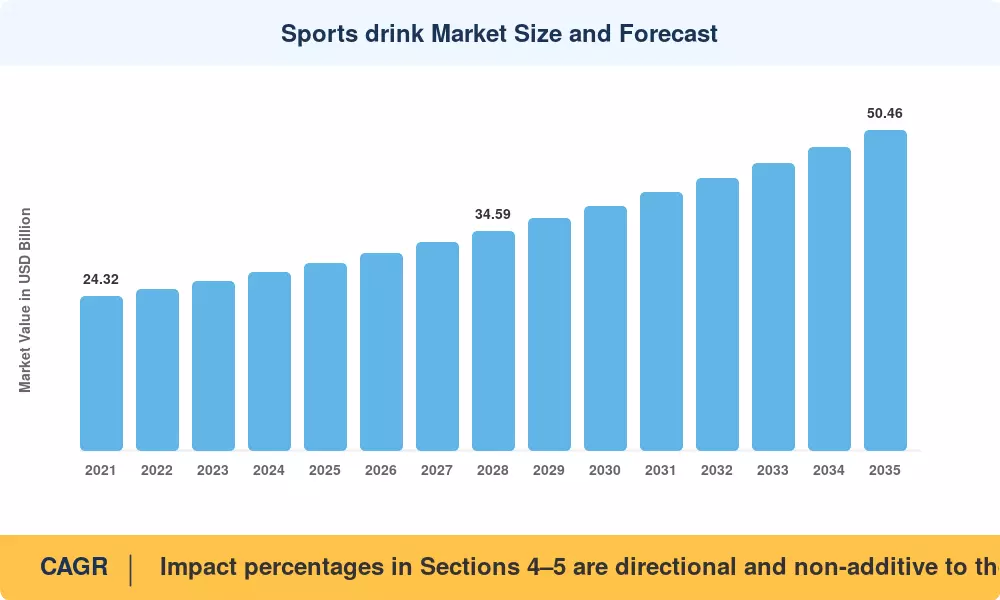

The global Sports Drink Market was valued at USD 29.42 billion in 2025 and is projected to grow from USD 31.05 billion in 2026 to USD 50.46 billion by 2035, registering a CAGR of 5.54% during the forecast period (2026–2035). Government-backed fitness promotion programs across 40+ countries and the mainstreaming of electrolyte hydration drink formats among non-athlete consumers have shifted this category from a niche athletic staple into a daily wellness product. The convergence of subscription-based direct-to-consumer channels with rising health consciousness among working-age populations continues to underpin demand acceleration.

Product innovation has reshaped the Sports Drink Market over the past three years. Legacy high-sugar formulations are giving way to zero-sugar, plant-based, and functional hydration blends enriched with vitamins, BCAAs, and adaptogens. PepsiCo alone committed over USD 550 million to reformulation and capacity expansion across its Gatorade franchise between 2023 and 2025, while Coca-Cola integrated its BodyArmor acquisition into a unified sports hydration portfolio [2]. These investments reflect a broader industry pivot toward clean-label transparency and science-backed efficacy claims.

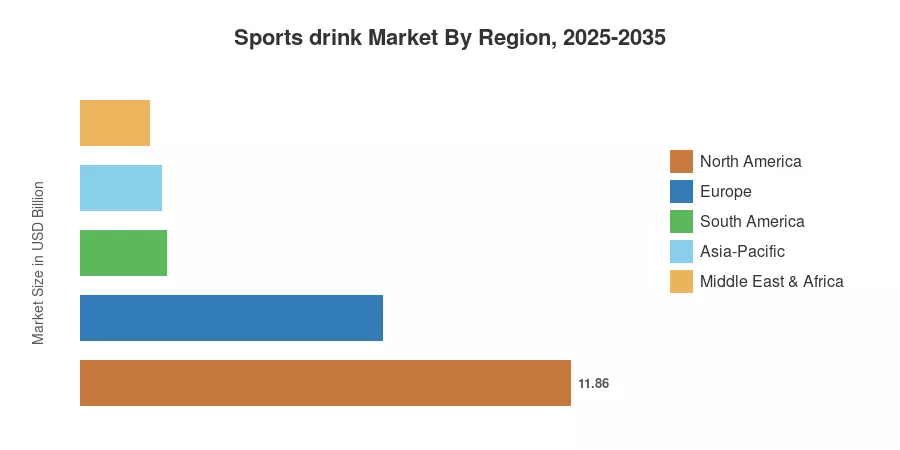

North America dominated the Sports Drink Market in 2025 with a 40.3% revenue share, driven by entrenched brand loyalty and robust convenience-store distribution networks. Asia-Pacific is set to register the fastest CAGR of 6.70% through 2035, fueled by urbanization, rising disposable incomes, and expanding gym culture in China, India, and Southeast Asia. Europe held the second-largest share at approximately 24.8%, supported by regulatory shifts encouraging reduced-sugar beverage reformulation. The decade ahead will likely see premiumization, wearable-linked personalized hydration, and powder-format convenience reshape the competitive landscape of the Sports Drink Market.

Key Report Takeaways

• By Soft Drink Type

- Isotonic beverages captured 56.2% of total Sports Drink Market volume in 2025, supported by broad consumer familiarity and clinical endorsement for moderate-intensity rehydration.

- Hypertonic variants are forecast to expand at a 7.12% CAGR through 2035 as endurance athletes seek higher carbohydrate concentrations for prolonged events.

• By Packaging Type

- PET bottles accounted for 60.3% of the Sports Drink Market revenue in 2025, remaining the preferred single-serve format across retail and on-the-go consumption.

- Aseptic packages are projected to grow at a 7.22% CAGR, gaining ground through e-commerce-friendly shipping profiles.

• By Region

- North America generated 40.3% of the global Sports Drink Market revenue in 2025.

- Asia-Pacific is expected to advance at a 6.70% CAGR during 2026–2035, the fastest among all regions.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework integrates primary trade interviews, import/export ledgers, manufacturer revenue disclosures, and distributor shipment data. Historical figures (2021–2024) rely on audited company financials and verified industry databases, while forecast figures (2026–2035) apply scenario-weighted regression against macroeconomic and consumer health indicators.

.webp?v=1782993230)