Electronic Components Market Summary

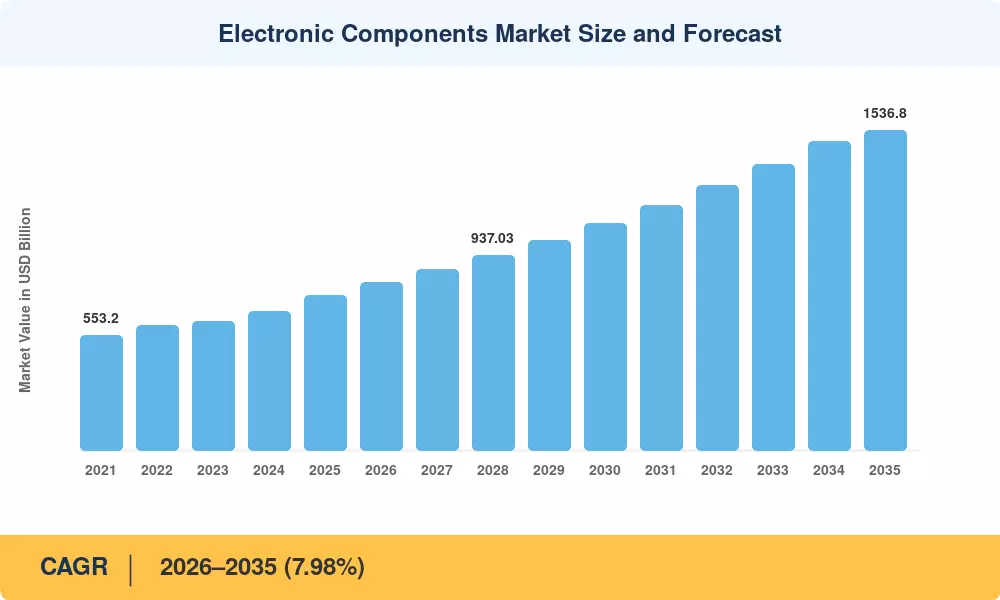

The electronic components market reached an estimated USD 745.06 billion in 2025 and is projected to climb from USD 804.53 billion in 2026 to approximately USD 1,536.80 billion by 2035, registering a CAGR of 7.98% across the forecast window. Two policy catalysts anchor this trajectory: the USD 52.7 billion U.S. CHIPS and Science Act, which has already triggered over USD 200 billion in private fab commitments on American soil, and the EUR 43 billion EU Chips Act redirecting semiconductor capacity toward European sovereignty [1][2]. Together, these programs are reshaping where discrete electronic devices and passive electronic parts are manufactured and consumed.

A sweeping technology transition is underway across the electronic components market. Legacy through-hole assemblies are yielding ground to advanced surface-mount configurations, while silicon-based power switches are being displaced by wide-bandgap gallium-nitride and silicon-carbide alternatives capable of handling higher voltages and frequencies. Global fab equipment spending on 300 mm production lines alone is forecast to exceed USD 420 billion between 2025 and 2027, underscoring the capital intensity required to keep PCB component supply aligned with surging AI-server and electric-vehicle demand [2][3].

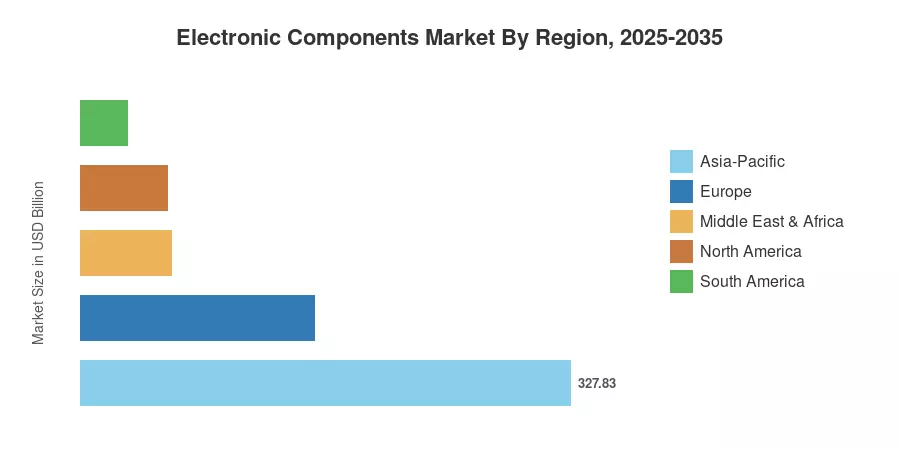

Asia-Pacific remains the dominant geography in the electronic components market, commanding roughly 44% of 2024 revenue, followed by North America at approximately 24%. The Middle East & Africa region, though comparatively small, is the fastest-growing at an 8.15% CAGR through 2035, driven by smart-city buildouts in Saudi Arabia and the UAE. As capacity diversification accelerates across India, Europe, and the Americas, the next decade will reward suppliers who balance geographic resilience with technology leadership in resistor capacitor components and compound semiconductor devices [4][5].

Key Report Takeaways

• By Component

- Active components held the lion's share of the electronic components market in 2024, accounting for roughly 86% of total revenue — a dominance driven by semiconductor IC demand across AI accelerators and automotive ECUs

- Passive electronic parts, including resistors, capacitor components, and ceramic dielectrics, are projected to expand at a 9.05% CAGR through 2035 as electric-vehicle power trains and 5G base stations raise content-per-board requirements

• By Mounting Technology

- Surface-mount devices captured approximately 75% of the electronic components market revenue in 2024, reflecting their advantages in automated high-volume PCB assembly

- Through-hole devices continue to serve niche military and industrial applications where the mechanical strength of electronic circuit elements outweighs density concerns

• By Region

- Asia-Pacific represented the largest share of the electronic components market in 2024, anchored by China, Japan, and South Korea's combined fab output

- The Middle East & Africa region is advancing at an 8.15% CAGR, the fastest among all geographies, fueled by government-led digital-infrastructure programs

Electronic Components Market Size and Forecast (2021–2035)

MRFR's market sizing draws on a bottom-up approach combining company revenue disclosures, fab utilization trackers from SEMI and WSTS, and end-market demand models validated against customs and trade data. Historical figures (2021–2024) rely on audited financials and association statistics; the base-year 2025 estimate is triangulated from preliminary shipment data, while the 2026–2035 forecast applies the calibrated 7.98% CAGR with adjustments for cyclical inventory corrections.

.webp?v=1783415684)