Energy Bar Market Summary

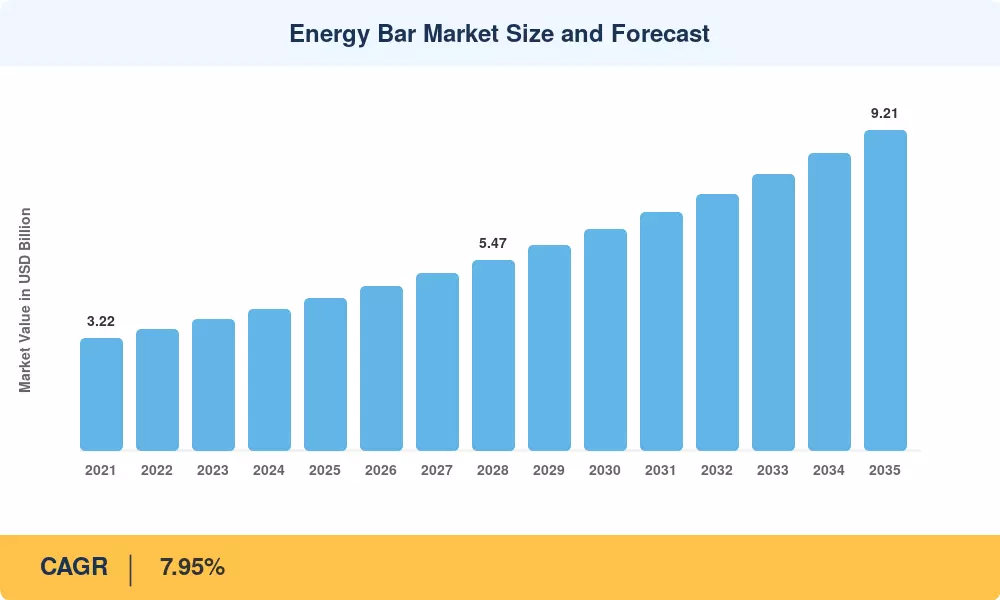

The Energy Bar Market was valued at USD 4.38 Billion in 2025, with the forecast opening at USD 4.73 Billion in 2026 and rising to USD 9.21 Billion by 2035 at a CAGR of 7.95% over the 2026–2035 window. Two catalysts anchor this trajectory: the U.S. FDA's 2025 updated definition of "healthy" food labeling, which has pushed reformulation across the protein energy snack bar category, and an estimated USD 1.8 billion in venture and strategic capital deployed into functional nutrition brands between 2023 and 2025 [1]. Demand has shifted from indulgent confectionery formats toward clean-label, macro-balanced products consumed across athletic, occupational, and meal-replacement occasions.

Reformulation is the dominant transformation underway in the Energy Bar Market. Legacy high-sugar, gelatin-bound bars are being displaced by natural whole-food energy bar formats using dates, nut butters, and pea or rice protein isolates. The International Food Information Council reports that 74% of U.S. consumers actively read protein content claims, and brands have responded with extrusion-free cold-pressed manufacturing lines — capital deployments for these lines exceeded USD 420 million globally in 2024 [2][7].

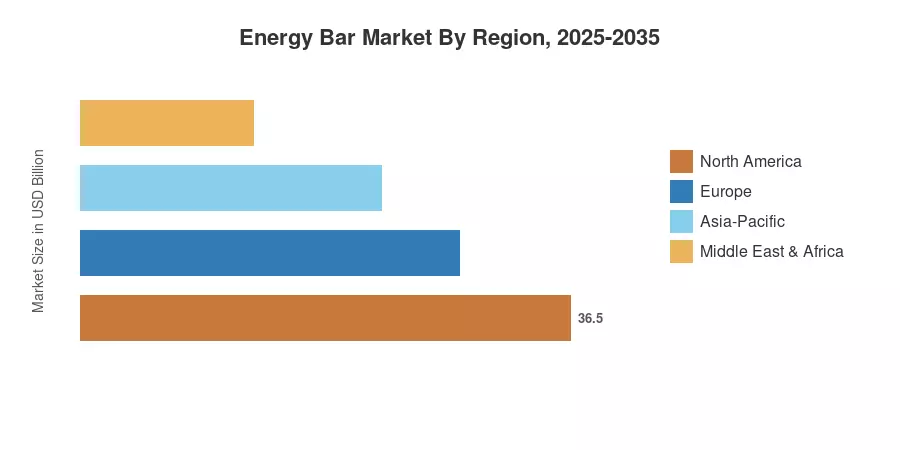

Regionally, North America leads the Energy Bar Market with a 38.6% share in 2025, supported by mature retail penetration and a deep base of sports performance energy bar SKUs. Asia-Pacific is the fastest-growing region at a 9.42% CAGR through 2035, propelled by gym memberships in India and China, while Europe holds the second-largest position at roughly 28.4% share, driven by clean-label regulation and organic certification depth. Convergence between functional nutrition and everyday snacking will define the Energy Bar Market through the next decade.

Key Report Takeaways

• By Product Type

- Conventional bars commanded approximately 74.2% of Energy Bar Market revenue in 2025, reflecting entrenched retail shelf dominance

- Organic bars are projected to expand at an 8.10% CAGR through 2035 on clean-label demand

• By Protein Source

- Plant-based formats generated an estimated USD 2.41 Billion in 2025 within the Energy Bar Market, anchored by pea and rice protein systems

- Animal-based bars, including whey and collagen formulations, are forecast to grow at an 8.32% CAGR

• By Function / Application

- Sports and endurance nutrition held 73.9% share of 2025 demand

- Weight-management and lifestyle-energy formats are tracking an 8.68% CAGR through 2035

• By Packaging

- Single-pack units captured roughly 50.5% of 2025 volume in the Energy Bar Market

- Multi-pack boxes are forecast to grow at an 8.35% CAGR, boosted by subscription channels

• By Distribution

- Supermarkets and hypermarkets accounted for approximately USD 1.76 Billion of 2025 revenue

- Online retail is the fastest-growing channel at a 9.05% CAGR

• By Region

- North America leads the Energy Bar Market with 38.6% share in 2025

- Asia-Pacific is the fastest-growing region at a 9.42% CAGR

- Europe contributes roughly USD 1.24 Billion of 2025 revenue

Market Size and Forecast (2021–2035)

Forecast values combine top-down sizing from retail scanner data (Circana, NielsenIQ), bottom-up shipment estimates from leading manufacturers, and triangulation against trade flow data from UN Comtrade. Volumes are reported in units; values in USD Billion.

.webp?v=1783326287)