Enterprise Key Management Market Summary

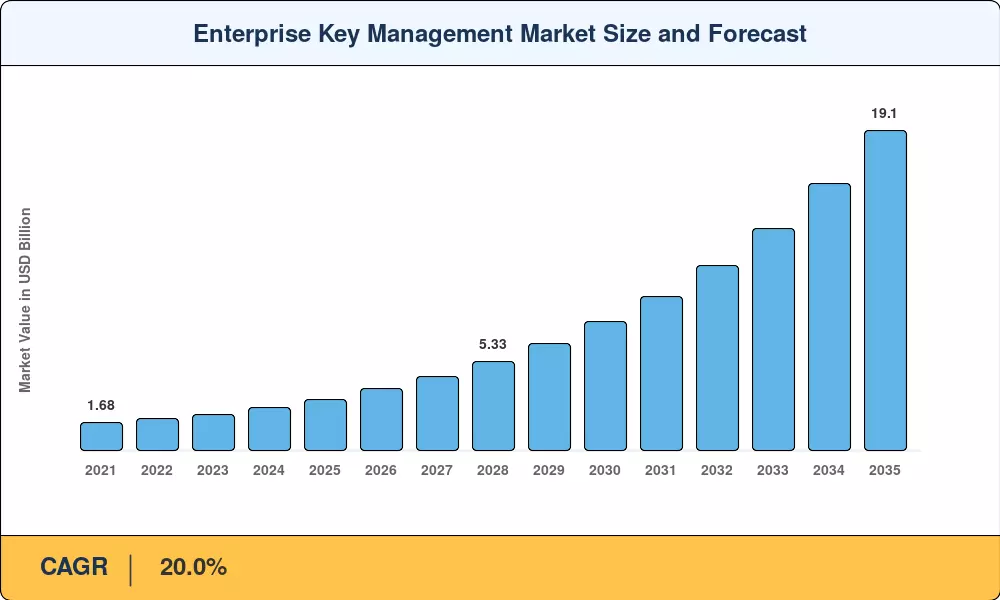

The Enterprise Key Management Market was valued at USD 3.04 Billion in 2025 and is projected to reach USD 3.70 Billion in 2026 before climbing to USD 19.10 Billion by 2035, registering a compound annual growth rate of 20.0% during the 2026–2035 forecast window. Regulatory pressure continues to act as the single largest catalyst — the European Union's revised NIS2 Directive now mandates cryptographic key governance for all essential-service operators, while the U.S. Executive Order 14028 on cybersecurity pushed federal agencies toward zero-trust architectures that depend on centralized encryption key lifecycle management [1]. These twin policy anchors converted what was discretionary security spending into board-level compliance line items.

Legacy, on-premises hardware security modules are giving way to cloud-native and hybrid key management platforms capable of orchestrating millions of cryptographic keys across multi-cloud environments. estimated that enterprises managing workloads on three or more public clouds doubled between 2022 and 2025, fueling demand for interoperable key governance [2]. The shift is not merely operational: organizations now treat encryption keys as strategic assets whose mismanagement can trigger data-breach penalties exceeding USD 20 million under GDPR alone.

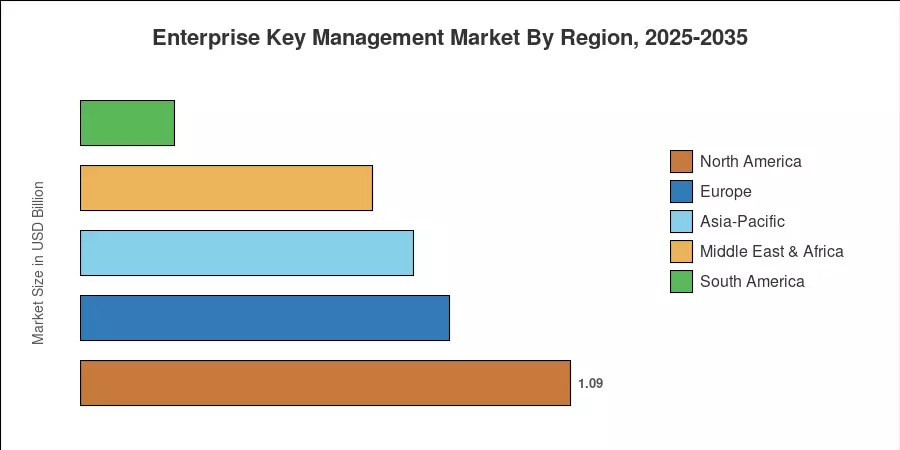

North America commands roughly 36.0% of the Enterprise Key Management Market, anchored by concentrated financial-services and federal IT spending. Asia-Pacific is the fastest-growing region at an estimated 24.2% CAGR, driven by India's Digital Personal Data Protection Act and China's expanding Cybersecurity Law enforcement. Europe trails as the second-largest contributor, with approximately 27% share backed by DORA and post-quantum cryptography preparedness mandates [3]. As hybrid-cloud adoption accelerates globally, the Enterprise Key Management Market is poised to remain one of the fastest-expanding segments within the broader cybersecurity landscape through 2035.

Key Report Takeaways

• By Deployment Type

- Cloud deployment accounted for an estimated 58.2% of the Enterprise Key Management Market in 2025, reflecting the rapid migration of encrypted workloads to public and hybrid environments.

- On-premises deployment is forecast to grow at approximately 16.8% CAGR through 2035, sustained by defense and government buyers with air-gapped network requirements.

• By Enterprise Size & Application

- Large enterprises held a 53.7% revenue share in 2025, driven by complex multi-cloud estates requiring unified key orchestration.

- Cloud encryption led application segments with 35.7% share in 2025, while disk encryption is projected to reach a 21.8% CAGR over the forecast period.

• By End-User Vertical

- Banking, financial services, and insurance captured 33.4% of the Enterprise Key Management Market in 2025, reflecting stringent PCI-DSS and SOX compliance mandates.

• By Region

- Asia-Pacific is the fastest-expanding region at a projected 24.2% CAGR, while North America contributed 36.0% of global revenue in 2025.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework triangulates vendor revenues, enterprise IT security budgets, and regulatory-driven adoption curves to produce the year-by-year trajectory below. Historical values (2021–2024) rely on audited company filings and verified procurement databases; forecast values (2026–2035) apply the calibrated 20.0% CAGR with adjustments for anticipated regulatory inflections in 2028 and 2032.