Face Mask Market Summary

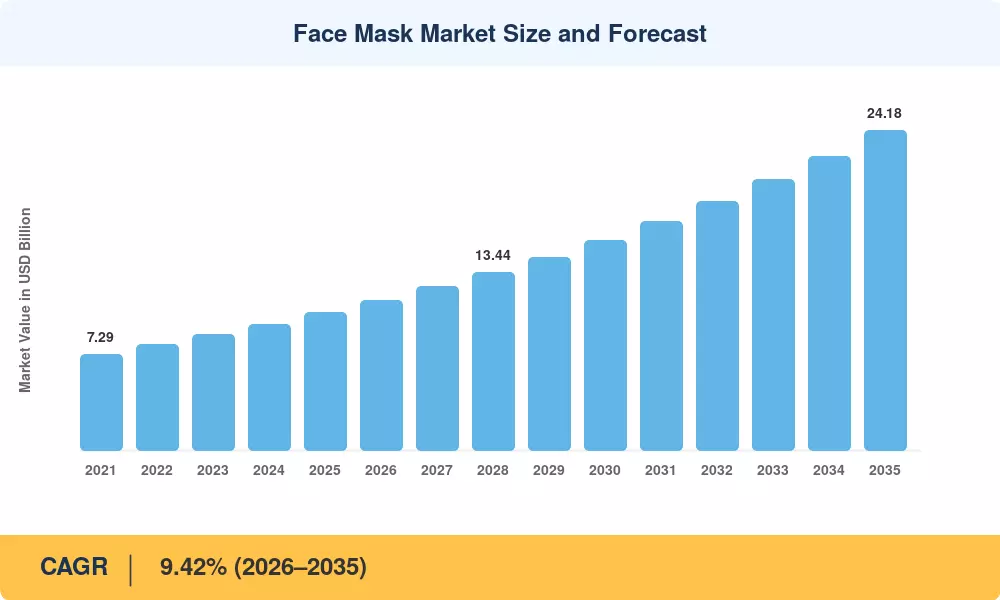

The Face Mask Market was valued at USD 10.45 billion in 2025 and is projected to reach USD 11.38 billion in 2026 before climbing to USD 24.18 billion by 2035, registering a CAGR of 9.42% during 2026–2035. This expansion is anchored in a global consumer pivot toward skincare facial treatment masks that deliver targeted results — driven by rising dermatological awareness and clean-beauty mandates across the EU and East Asia. The global skincare economy exceeded USD 180 billion in 2024, and facial masks remain one of its fastest-growing sub-categories as ingredient-conscious consumers demand more from every application.

A significant transformation is currently taking place in the manner in which brands create and distribute clay masks and sheet masks. Biocellulose, hydrogel, and sustainably sourced fiber substrates that are infused with encapsulated actives are replacing legacy single-use cotton masks. Between 2022 and 2024, Korean beauty conglomerates alone invested more than USD 1.2 billion in next-generation mask research and development. This investment has facilitated the advancement of hydrating and anti-aging face masks that integrate microbiome science with device-assisted delivery [3]. Across the Face Mask Market, the real-time inventory and fulfillment strategies have been reshaped as a result of the compression of the discovery-to-purchase cycle to under three minutes by live-commerce platforms.

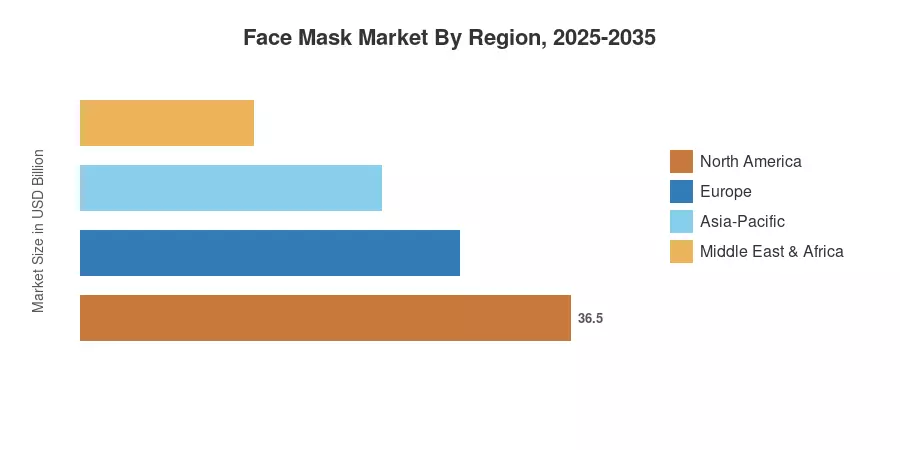

The Face Mask Market is dominated by the Asia-Pacific region, with a revenue share of approximately 70.8% in 2025. This dominance is attributed to the profoundly ingrained masking rituals in South Korea, Japan, and China With a projected compound annual growth rate (CAGR) of 4.89%, North America is the fastest-growing region, driven by dermatologist-backed brands' entry into mass retail. Europe's second-largest share, at approximately 14.2%, is supported by the EU's increasingly stringent cosmetic safety regulations, which prioritize premium, clean-label formulations. Companies that maintain omnichannel agility and possess proprietary active-delivery IP will be rewarded in the coming decade.

Key Report Takeaways

• By Product Type

- Cream and gel masks commanded approximately 50.1% of Face Mask Market revenue in 2025, driven by consumer preference for mess-free, leave-on skincare facial treatment masks

- Clay masks are forecast to expand at a 3.01% CAGR through 2035 as detoxifying, exfoliating and peel-off masks gain traction among combination-skin consumers

- Sheet masks represented USD 2.88 billion in 2025 sales, supported by single-dose convenience and K-beauty influence

• By End User & Ingredient

- Women accounted for 62.9% of Face Mask Market sales in 2025, though men's grooming routines are broadening rapidly

- Conventional formulations held a 74.4% share; natural and organic variants are growing at a 4.22% CAGR as clean-label demand intensifies

• By Geography

- Asia-Pacific led the Face Mask Market at USD 7.40 billion in 2025

- North America is expected to register the fastest CAGR at 4.89% through 2035, with overnight sleeping face mask formats gaining shelf space

- Europe contributed 14.2% share, anchored by regulatory-driven ingredient transparency

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue modeling from 450+ brand-level data points, validated against import/export databases, retail panel data, and proprietary consumer surveys across 32 countries.