Fatty Alcohol Market Summary

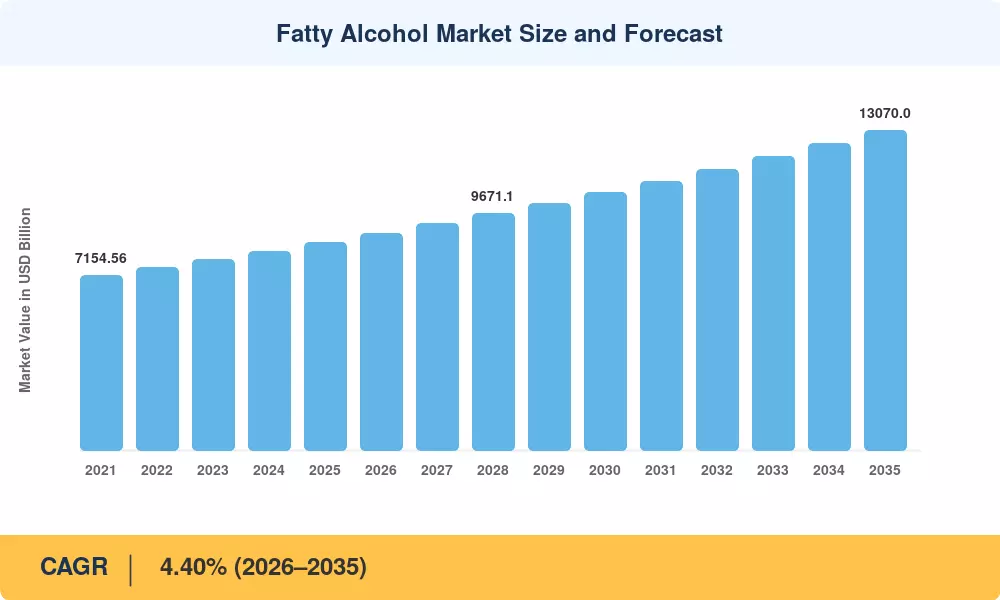

The Fatty Alcohol Market reached USD 8,500 Million in 2025 and is projected to climb from USD 8,874 Million in 2026 to USD 13,070 Million by 2035, registering a CAGR of 4.40% across the forecast period (2026–2035). Two catalysts underpin that growth trajectory: the EU's Deforestation-Free Regulation (EUDR), which redirects procurement toward certified oleochemical products and traceable supply chains, and Indonesia's USD 3.2 billion downstream oleochemical investment program announced under its 2025–2029 industrial masterplan [2]. Both policy frameworks tighten feedstock accountability while simultaneously expanding capacity for bio-based alcohols in Southeast Asia.

A fundamental change is changing the production basis of the Fatty Alcohol Market. Legacy batch-distillation approaches that once dominated detergent alcohols manufacturing are being replaced by continuous hydrogenation platforms that can produce greater purity cuts at lower energy intensity. An example of this transition is the USD 420 million Dumai expansion of Wilmar International, due to be commissioned mid-2026, adding 280,000 tons of fractionated surfactant chemicals capacity with integrated methyl-ester hydrogenolysis [3]. At the same time, European and North American companies are investing in coal-to-syngas and ethylene-derived synthetic routes that sidestep palm-kernel-oil instability and are attractive to personal care products purchasers seeking deforestation-free certification.

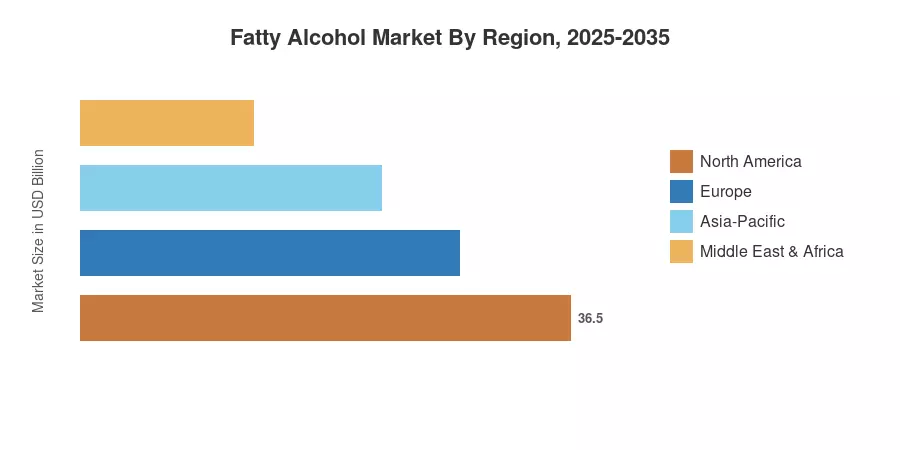

Asia-Pacific dominates the Fatty Alcohol Market with about 48%, led by Indonesia’s palm-kernel-oil refining clusters and China’s growing coal-based syngas corridors. It is also the fastest-growing region with a CAGR of 5.50% through 2035. Reformulation of cleaning product chemicals towards biodegradable surfactant systems makes Europe the second-highest share at around 24%. With unique cosmetic raw ingredients and pharmaceutical-grade excipient requirements, North America represents 16% of worldwide demand

Key Report Takeaways

• By Source

- Natural fatty alcohols retained approximately 72% of 2025 volume, reflecting ongoing demand for oleochemical products derived from palm-kernel and coconut oils

- Petrochemical-route detergent alcohols are advancing at a 4.75% CAGR through 2035, gaining traction in markets where ethylene feedstock economics favor synthetic production

• By Application

- The surfactants segment commanded roughly 52% of the Fatty Alcohol Market in 2025, serving industrial emulsifiers and household cleaning product chemicals formulations

- Personal care and cosmetics applications are forecast to expand at a 5.10% CAGR through 2035, fueled by the premiumization of cosmetic raw materials across Asia and North America

• By Geography

- Asia-Pacific captured 48% of the Fatty Alcohol Market in 2025, led by Indonesia, China, and India

- South America is emerging as a high-growth pocket, with Brazil's oleochemical products sector attracting new capacity investments

Fatty Alcohol Market Size and Forecast (2021–2035)

MRFR’s sizing methodology combines a bottom-up production-capacity study (plant-level output from 47 main facilities) with a top-down demand modeling, validated by customs-trade data from UN Comtrade and national chemical-industry associations. Historical numbers are derived from audited yearly reports and ICIS pricing evaluations. The forecast uses a supply-demand balance adjusted for stated capacity increases and regulatory-driven demand shifts.