Floating Power Plant Market Summary

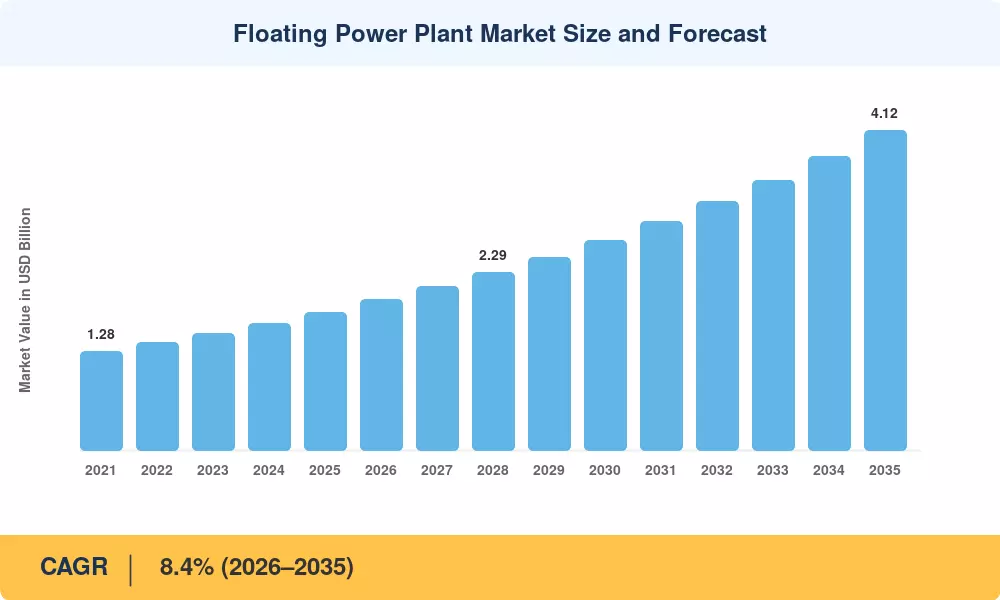

The Floating Power Plant Market reached an estimated USD 1.78 billion in 2025 and is projected to grow from USD 1.93 billion in 2026 to USD 4.12 billion by 2035, registering a CAGR of 8.4% across the forecast window. Two catalysts anchor this trajectory: the European Union's revised Offshore Renewable Energy Strategy targeting 300 GW of offshore wind by 2050, and a surge of sovereign-backed tenders across Southeast Asia seeking barge-mounted floating power plant solutions to electrify remote archipelagic communities [2]. Governments that once treated floating generation as a niche are now writing it into national energy security roadmaps.

A technology shift is reshaping how electricity reaches coastal and island populations. Legacy diesel-fired shore plants and aging grid extensions are giving way to modular floating power unit deployments, floating LNG power plant FSRP conversions, and pilot-scale floating nuclear SMR power barge concepts. The International Renewable Energy Agency (IRENA) estimates that floating wind alone attracted over USD 3.5 billion in committed capital between 2022 and 2024, while floating solar PV power plant installations crossed the 6 GW cumulative mark globally [3]. Automation and digital twins are compressing commissioning timelines for FPSO floating power generation vessel retrofits from 18 months to under 12 months.

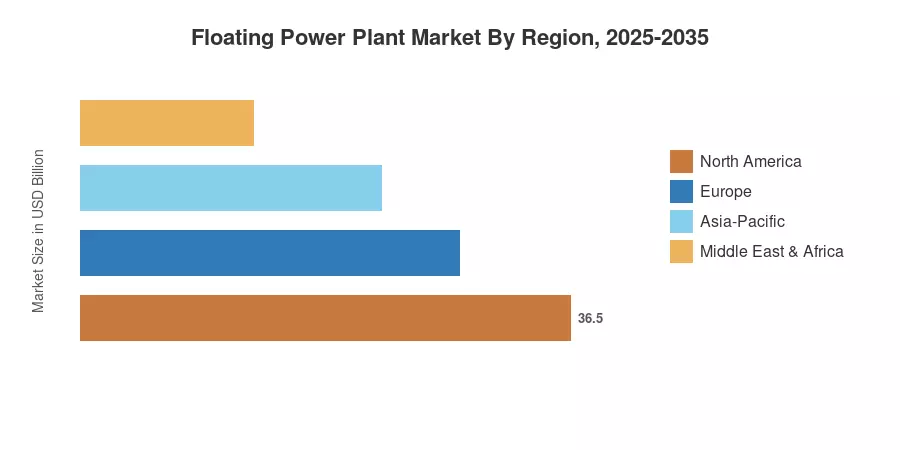

Europe commands roughly 38% of the Floating Power Plant Market, buoyed by nine announced offshore floating wind projects and favorable feed-in tariff regimes. Asia-Pacific is the fastest-growing Region with a projected CAGR of 10.2%, driven by Japan, South Korea, and India scaling floating solar PV power plant farms. North America holds approximately 22% share, led by U.S. Department of Energy grants for deepwater floating wind demonstrations off California and Maine [4]. The decade ahead will reward players who master hull-integrated power systems and hybrid renewable-gas configurations.

Key Report Takeaways

• By Source

- The Renewable segment accounts for nearly 62% of the Floating Power Plant Market in 2025, propelled by declining levelized costs for offshore floating wind turbines and growing policy mandates favoring clean energy

- Non-Renewable floating power generation—primarily floating LNG power plant FSRP units and barge-mounted floating power plant diesel conversions—is forecast to grow at a CAGR of 5.8% as island nations seek transitional bridge fuels

• By Technology Platform

- Floating wind turbine platforms represent the single largest investment category, with European developers committing over USD 2.1 billion to semi-submersible and tension-leg designs between 2023 and 2025

- Floating solar PV power plant installations are expanding at 11.3% CAGR, especially across reservoirs in India and Southeast Asia, where land scarcity drives adoption of modular floating power unit arrays

• By Region

- Europe dominates the Floating Power Plant Market, contributing approximately USD 0.68 billion in 2025 revenue

- Asia-Pacific is on track to surpass North America in absolute value by 2029, as Japan, South Korea, and ASEAN nations accelerate offshore floating wind pilot-to-commercial transitions

Market Size and Forecast (2021–2035)

MARKET RESEARCH FUTURE (MRFR)'s market sizing combines bottom-up project-level revenue tracking across 42 countries with top-down cross-validation against publicly reported contract values, FPSO floating power generation vessel order books, and regulatory capacity auction results. Historical figures (2021–2024) rely on confirmed deployment data; the 2025 base year blends actual H1 results with H2 pipeline estimates. Forecast years apply the calibrated 8.4% CAGR, adjusted for known project delays and policy phase-ins.