Floor Coatings Market Summary

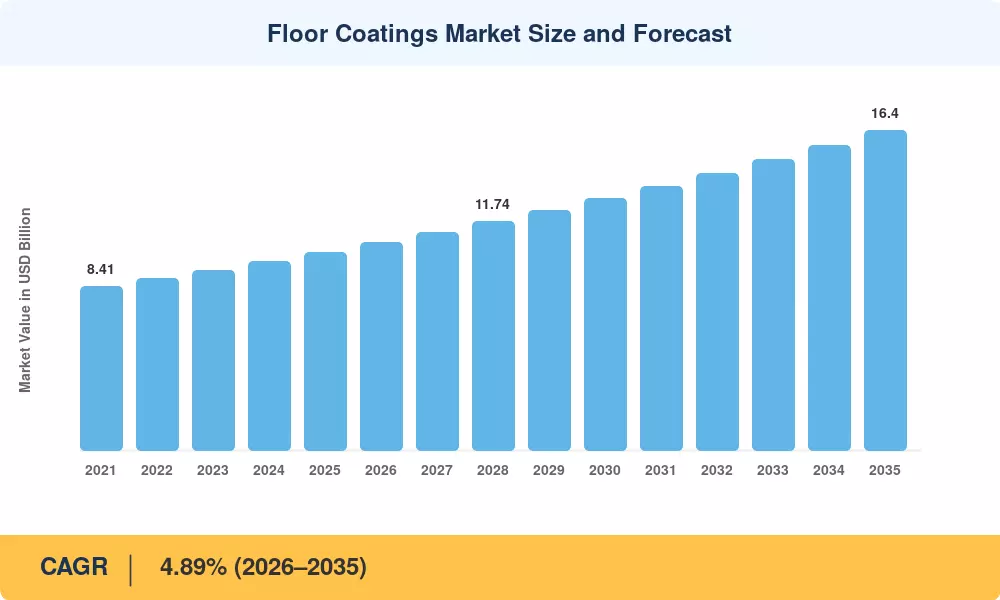

The Floor Coatings Market reached an estimated USD 10.17 Billion in 2025 and is projected to grow from USD 10.67 Billion in 2026 to USD 16.40 Billion by 2035, registering a CAGR of 4.89% across the forecast window. This expansion is anchored in two powerful catalysts: the accelerating build-out of cold-chain logistics infrastructure — where antimicrobial epoxy floor coatings have become the default specification — and the global wave of EV-battery gigafactory construction, which mandates conductive and electrostatic-dissipative protective flooring systems[2]. Tightening VOC emission regulations across the European Union and Nordic countries continue to redirect formulation budgets toward low-emission, high-performance chemistries.

A genuine technology shift is underway within the Floor Coatings Market. Legacy solvent-borne systems, which dominated specifications for decades, are ceding ground to UV-cured and water-borne formulations that cut facility downtime from days to hours. The EU's revised Decopaint Directive (2024 amendment) now caps VOC content in industrial floor paints at 100 g/L for interior applications, compelling formulators to reformulate or lose access to one of the world's largest coating markets [3]. Investment in UV-cured line capacity across Asia exceeded USD 420 million during 2023–2024 alone, according to industry estimates [4].

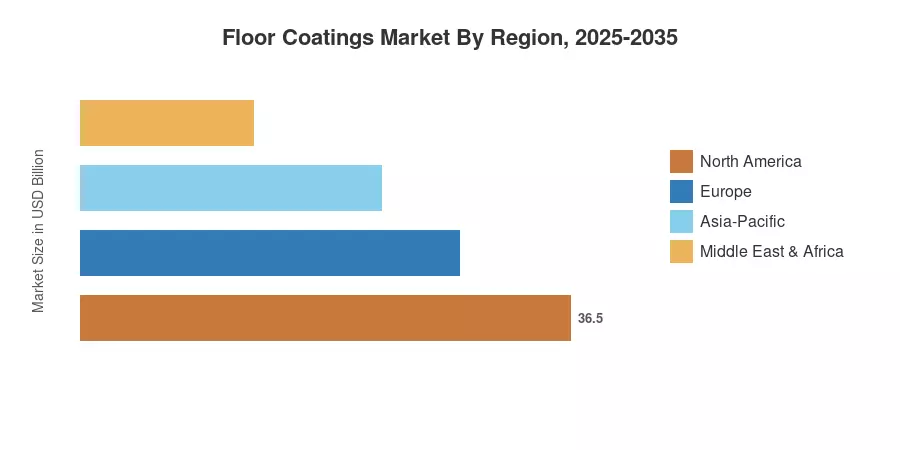

Asia-Pacific commands roughly 41.3% of global Floor Coatings Market revenue, driven by China's warehouse construction boom and India's expanding pharmaceutical manufacturing base. The region also registers the fastest CAGR at 5.14% through 2035. North America holds approximately 24.8% share, buoyed by reshoring-driven industrial construction, while Europe accounts for 22.1%, led by sustainability-linked concrete floor protection mandates. As clean-room and food-grade facility standards tighten worldwide, demand for polyurethane floor coatings and decorative floor coatings in commercial environments will sustain above-average growth across the coming decade.

Key Report Takeaways

• By Product Type

- Epoxy floor coatings commanded a 53.9% revenue share of the Floor Coatings Market in 2025, reflecting dominant specification in warehousing and manufacturing facilities.

- Polyurethane floor coatings are forecast to expand at a 5.06% CAGR through 2035, driven by abrasion-resistance requirements in automotive plants.

- Polyaspartic systems are gaining traction in rapid-return-to-service applications, particularly in retail and healthcare environments.

• By Technology

- UV-cured formulations captured 37.8% of the Floor Coatings Market share in 2025, reflecting a migration away from solvent-borne surface coating materials.

- Water-borne systems are expanding at the fastest pace among conventional technologies, supported by regulatory tailwinds in Europe and North America.

• By Region

- Asia-Pacific accounted for 41.3% of global Floor Coatings Market revenue in 2025, with China and India together representing over 60% of regional demand.

- North America's industrial floor paints segment is benefiting from over USD 200 billion in committed manufacturing reshoring investments through 2030.

Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework triangulates supply-side revenue data from publicly listed coatings manufacturers, downstream distributor surveys across 32 countries, and project-level tracking of industrial and commercial construction permits. Historical figures are calibrated to audited annual reports; forecast values apply a compound-growth model adjusted for macroeconomic cyclicality and regulatory phase-in schedules.