Flue Gas Desulfurization Market Summary

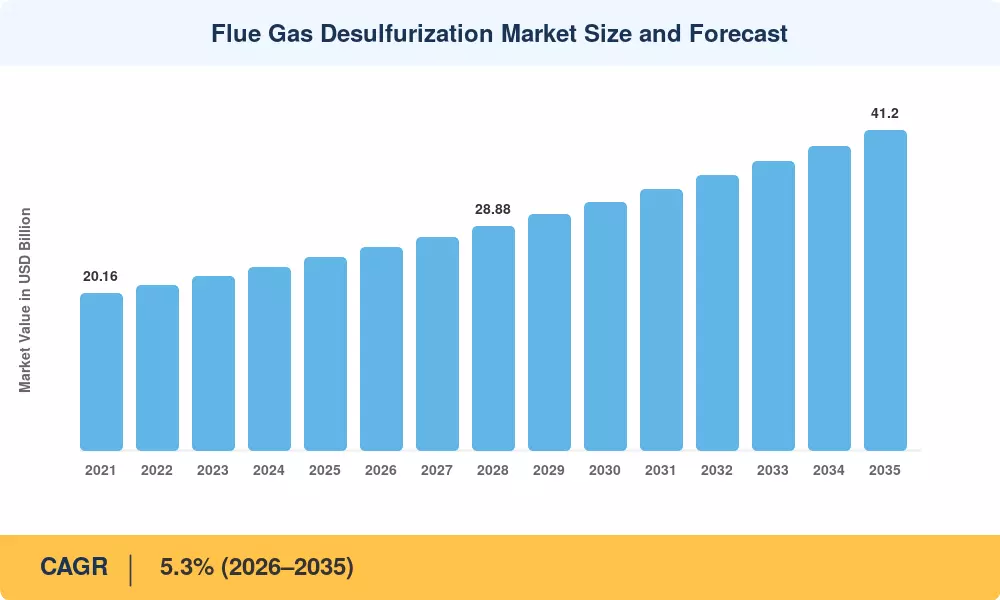

The Flue Gas Desulfurization Market reached an estimated USD 24.8 billion in 2025 and is projected to grow from USD 26.1 billion in 2026 to USD 41.2 billion by 2035, registering a CAGR of 5.3% during the forecast period (2026–2035). Two forces are converging to push this expansion: tightening sulfur dioxide (SO₂) emission limits under the EU Industrial Emissions Directive revision and China's Ultra-Low Emission (ULE) mandate, which together compel more than 1,200 GW of coal-fired capacity to install or upgrade wet limestone FGD scrubber systems by 2030 [1][2]. Globally, cumulative investment in SO₂ control equipment exceeded USD 9.4 billion in 2024 alone, a figure the IEA expects to climb as emerging economies adopt stricter air-quality standards [3].

Technology transformation is transforming the Flue Gas Desulfurization Market at all levels. Regenerable spray dry absorber SDA FGD systems are replacing legacy once-through sorbent systems with reagent costs down by 30–40% and removal efficiencies of > 95% [4]. Meanwhile, dry sorbent injection DSI FGD technology is gaining momentum in smaller industrial boilers where capital budgets are tight. More than 200 power units across 23 states face accelerated conversion timetables under the U.S. EPA’s Good Neighbor Plan, prompting a USD 2.1 billion surge in FGD upgrade contracts between 2024 and 2026 [5].

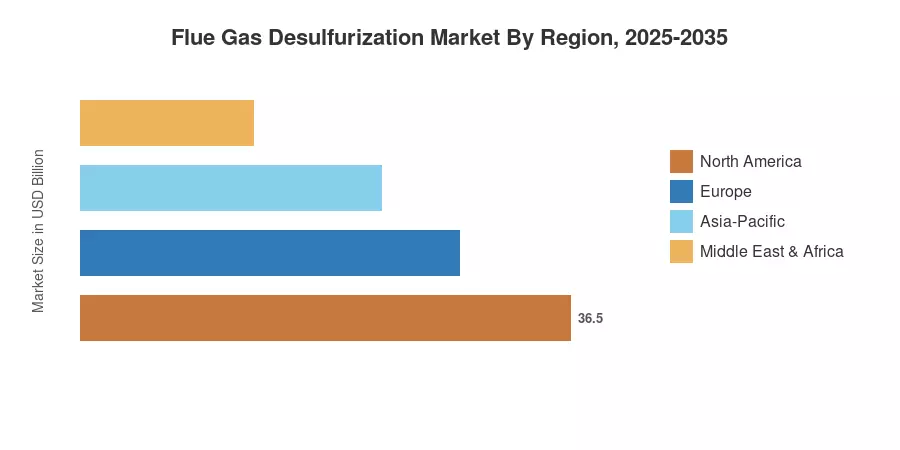

Asia-Pacific Leads Largest Flue Gas Desulfurization Market with ~42% Global Revenue Share Driven by Coal-Heavy Energy Mixes in China and India. The region also has the highest CAGR of 6.1% till 2035. The EU has a share of around 24%, supported by stringent Large Combustion Plant BAT findings requiring near-zero SO₂ limits [6]. North America holds over 20% market while the combined share of the Middle East & Africa and South America accounts for the rest 14%, with cement and refinery applications contributing to the incremental demand.

Key Report Takeaways

• By Technology

- Wet limestone FGD scrubber technology commands roughly 58% of global revenue, underpinned by its proven >97% SO₂ removal rate in utility-scale power plants

- Spray dry absorber SDA FGD system installations are expanding at a CAGR of 6.8%, the fastest among all technology segments

- Dry sorbent injection DSI FGD is projected to reach USD 3.9 billion by 2035, driven by retrofit demand in sub-200 MW industrial boilers

• By Application

- The power generation sector accounts for 64% of the total Flue Gas Desulfurization Market value, reflecting its outsized coal consumption

- Cement and metal smelting collectively represent a CAGR of 5.9% as emission norms extend beyond the power sector

• By Region

- Asia-Pacific's Flue Gas Desulfurization Market is forecast to exceed USD 17.3 billion by 2035

- Europe's share is supported by the EU Emissions Trading System carbon-price signal, which indirectly incentivizes multi-pollutant control

- North America's FGD seawater scrubbing SO₂ removal niche is growing in coastal refinery clusters along the U.S. Gulf Coast

Market Size and Forecast (2021–2035)

The market sizing model by Market Research Future (MRFR) takes into account bottom-up equipment shipment data from 14 OEM filings and cross-verifies it with top-down macro variables from the IEA World Energy Investment report. Historical values (2021–2024) are from audited revenue reports and customs trade records. Forecast values (2026–2035) are from a hybrid econometric-diffusion model adjusted to regulatory compliance deadlines for 48 nations.