Gaskets And Seals Market Summary

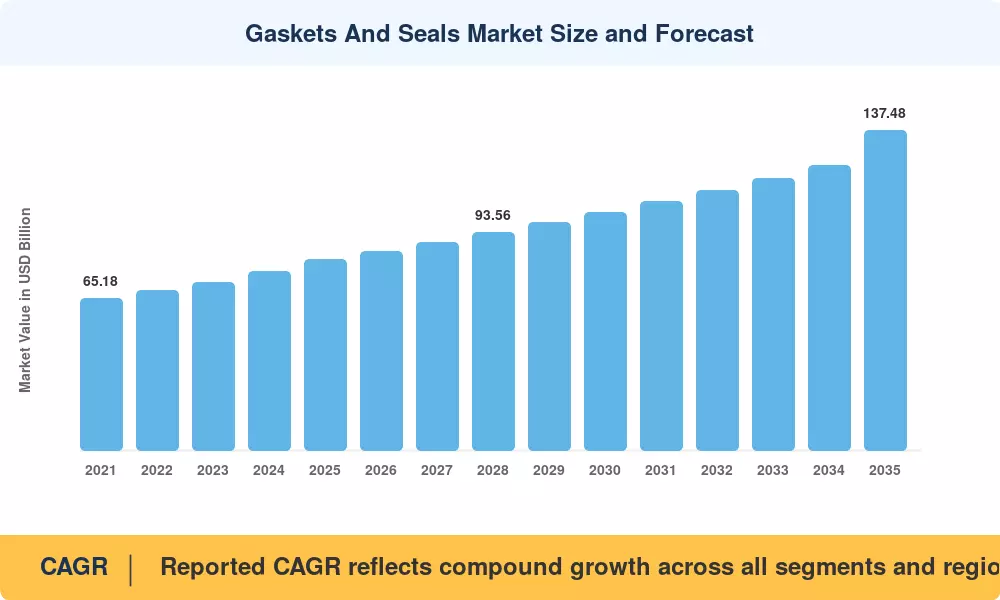

The Gaskets and Seals Market stood at an estimated USD 82.12 billion in 2025 and is projected to reach USD 85.58 billion in 2026 before climbing to USD 137.48 billion by 2035, registering a CAGR of 4.56% during 2026–2035. Two catalysts anchor this trajectory: first, the global push to expand LNG regasification capacity — with over USD 45 billion committed to new terminals between 2024 and 2030 [2] — is driving demand for spiral wound gasket flange assemblies rated to cryogenic service; second, electric-vehicle battery enclosure programs now require PTFE gasket chemical resistance standards that did not exist five years ago, creating an entirely new replacement cycle for automakers and Tier-1 suppliers.

Legacy compressed-fiber and cork-based sealing products are giving way to engineered elastomers and metallic gasket ring joint configurations designed for hydrogen-blend pipelines and high-pressure fuel-cell stacks. The U.S. Department of Energy's Hydrogen Shot initiative targets USD 1/kg clean hydrogen by 2030 [3], and every new hydrogen pipeline segment demands O-ring sealing elastomer components certified to ISO 23936-2. Meanwhile, fire safe valve seal certifications under API 607 continue to tighten, forcing midstream operators to accelerate replacement schedules for gate and ball valve assemblies.

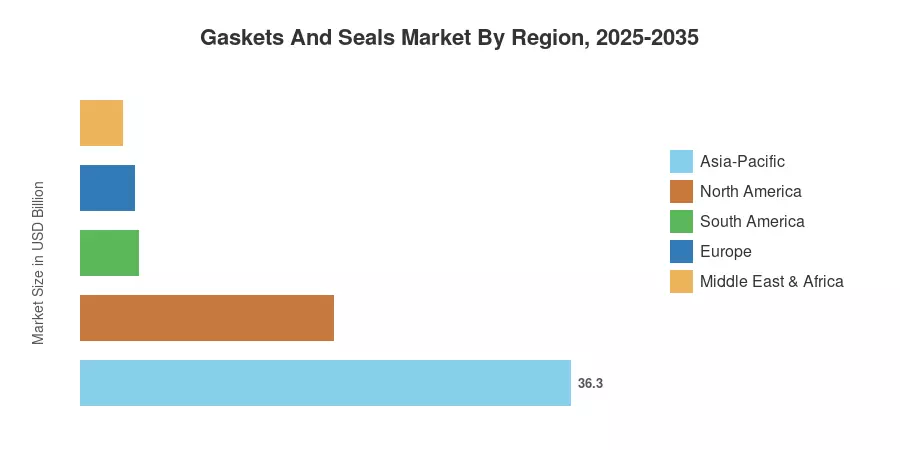

Asia-Pacific commands roughly 44.2% of global revenue, led by China's aggressive new-energy-vehicle build-out and India's refinery modernization push North America holds the second-largest share at approximately 22.8%, buoyed by wind-turbine repowering programs and shale-gas infrastructure maintenance. Europe follows closely, with its Green Deal Industrial Plan channeling investment into hydrogen-ready pipeline retrofits. The Gaskets and Seals Market is poised for sustained expansion as decarbonization mandates convert one-time capital projects into recurring seal-replacement revenue streams.

Key Report Takeaways

• By Product

- Seals accounted for approximately 62.3% of the Gaskets and Seals Market revenue in 2025, driven by hydraulic cylinder rod seal applications in mobile equipment and industrial automation

- Gaskets are forecast to grow at a 3.38% CAGR through 2035, with metallic gasket ring joint variants gaining share in LNG turnaround cycles

• By Material

- Metals represented the leading material category in 2025, anchored by spiral wound gasket flange demand in petrochemical and power-generation facilities

- Rubber compounds — including new fluoro-silicone and perfluoroelastomer grades — are expanding at the fastest pace, as automakers specify O-ring sealing elastomer solutions for battery thermal management

• By Sales Channel

- OEM shipments constituted roughly 60.1% of the 2025 Gaskets and Seals Market turnover, reflecting strong original-equipment integration cycles

- Aftermarket/MRO purchases will accelerate at a 5.34% CAGR as petrochemical operators extend asset life cycles beyond 30 years

• By Application

- Oil and gas held approximately 42.1% of the 2025 value, underpinned by fire-safe valve seal mandates across upstream and midstream operations

- Automotive OEM demand is advancing at the fastest rate through 2035, fueled by EV battery-enclosure sealing requirements and SAE J3277 compliance

• By Region

- Asia-Pacific generated the largest share and is climbing at the quickest CAGR among all regions, led by China and India

- North America benefits from hydrogen pilot lines and wind-turbine MRO spending

Gaskets and Seals Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework triangulates supply-side shipment data, downstream procurement records, and macroeconomic proxies (industrial production indices, refinery throughput, vehicle production volumes) to derive annual market-size estimates. Historical figures (2021–2024) rely on audited company filings and trade-association data; the base year (2025) reflects preliminary full-year estimates updated as of Q4 2025; and the forecast period (2026–2035) applies a calibrated compound growth model validated against bottom-up segment builds.