General Aviation Market Summary

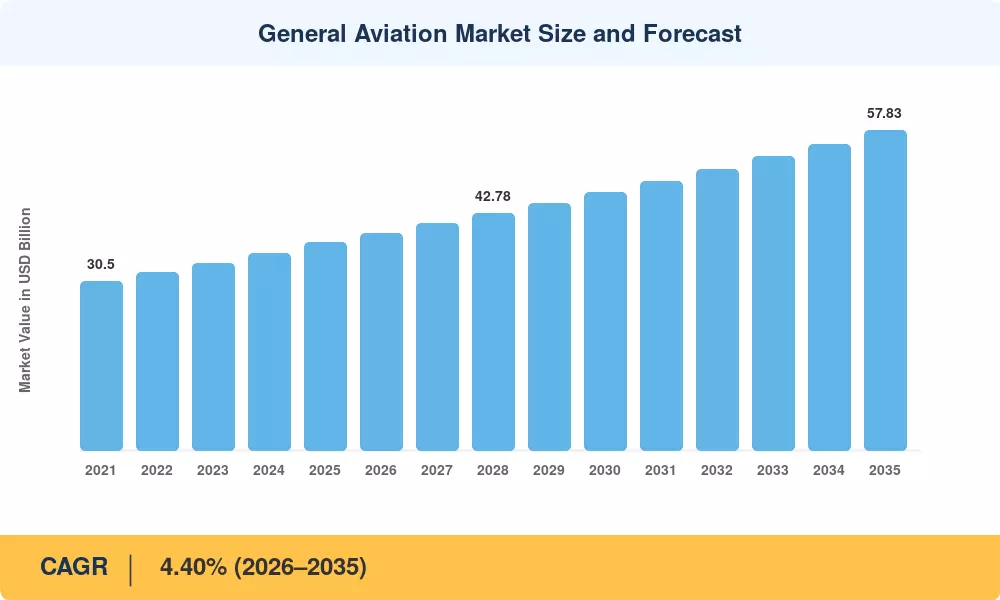

The general aviation market stood at USD 37.60 Billion in 2025 and is projected to reach USD 39.25 Billion in 2026 before climbing to USD 57.83 Billion by 2035, registering a CAGR of 4.40% across the forecast window. Sustained wealth accumulation among high-net-worth individuals and improving corporate profitability are channeling fresh capital into fleet expansion. The FAA Reauthorization Act of 2024 earmarked over USD 4.6 Billion for airport infrastructure modernization, directly benefiting non-commercial airfields and heliports that anchor the general aviation market ecosystem [1].

Propulsion technology is the headline transformation story. Conventional piston and turboprop powertrains remain the workhorse, yet hybrid-electric demonstrators from multiple OEMs logged certification milestones in 2024, pulling forward timelines for sub-regional commuter platforms. The European Union's ReFuelEU Aviation mandate, requiring a 2% sustainable aviation fuel blend by 2025, is pressuring operators and fuel distributors to invest in SAF supply chains that will reshape the general aviation market cost structure over the next decade [2].

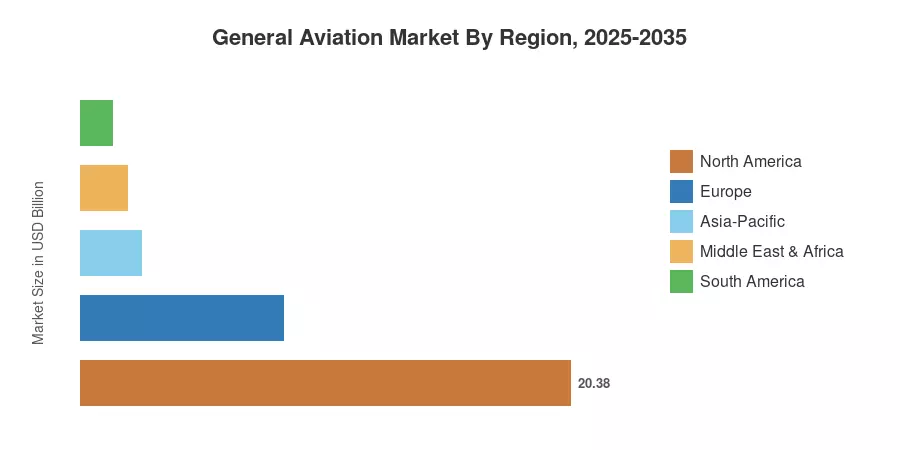

North America commands roughly 54.2% of the general aviation market, buoyed by the world's largest installed fleet of over 210,000 registered aircraft. Asia-Pacific is the fastest-growing region at a projected 6.75% CAGR, driven by greenfield airport construction in India and China. Europe holds the second-largest share at approximately 22.5%, supported by strong business-jet traffic corridors between London, Geneva, and Paris. The interplay of electrification, fractional ownership growth, and next-generation air-traffic management will determine how value is distributed across geographies through 2035.

Key Report Takeaways

• By Aircraft Type

- Business jets accounted for 49.8% of the general aviation market share in 2025, reflecting sustained corporate demand for intercontinental-range platforms.

- Turboprop and piston-engine aircraft delivered combined revenues exceeding USD 12.30 billion in 2025, serving training, agricultural, and regional connectivity roles.

- eVTOL and advanced air-mobility vehicles are projected to expand at a 3.90% CAGR through 2035 as certification pathways crystallize.

• By Ownership

- Full private ownership commanded 60.5% of the general aviation market in 2025.

- Charter and air-taxi operators are pacing at a 3.85% CAGR, broadened by on-demand booking platforms.

• By End Use

- Emergency medical services represent the fastest-growing end-user segment at a 5.35% CAGR to 2035.

• By Region

- North America captured over 54% of the general aviation market revenues in 2025.

- Asia-Pacific is logging the fastest regional CAGR at 6.75% through 2035.

- Europe contributed approximately USD 8.46 Billion in 2025 general aviation market value.

Market Size and Forecast (2021–2035)

Figures below combine primary research interviews with OEM delivery data, aircraft registry filings, FAA and EASA annual reports, and proprietary econometric modeling. Historical values (2021–2024) reflect actual deliveries and fleet utilization rates; forecast values (2026–2035) apply a constant CAGR anchored to the 2025 base year.