Geosynthetics Market Summary

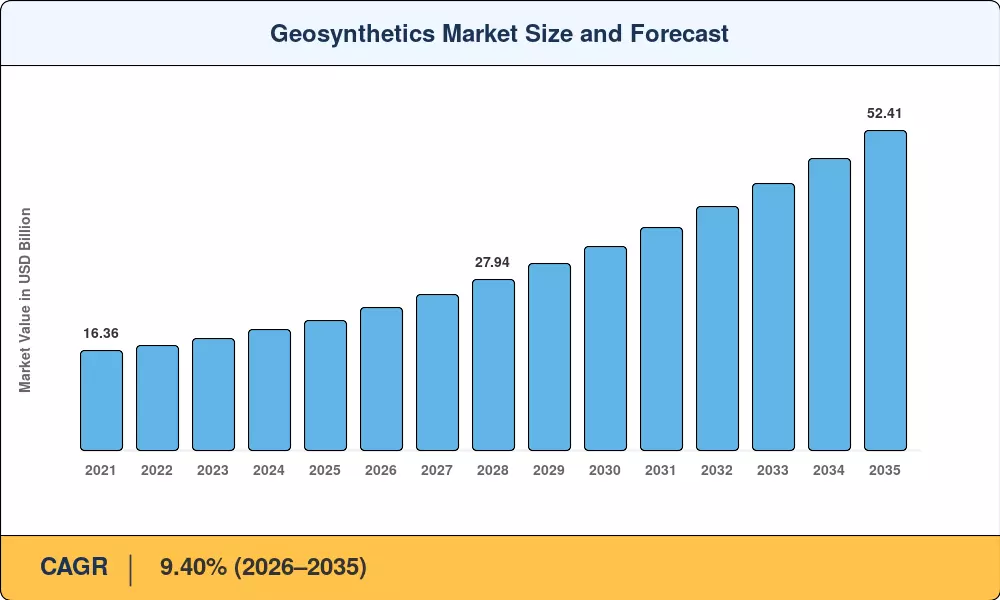

The Geosynthetics Market reached an estimated USD 21.34 Billion in 2025 and is forecast to climb from USD 23.35 billion in 2026 to USD 52.41 billion by 2035, registering a CAGR of 9.40% across the forecast window. Government-mandated infrastructure renewal programs—particularly the USD 1.2 trillion US Infrastructure Investment and Jobs Act and China's 15th Five-Year Plan expressway rollouts—are channeling unprecedented capital into polymer-based ground-improvement solutions that reduce aggregate consumption and shorten build cycles [1][2].

The Geosynthetics Market's procurement practices are changing due to a technological shift. Advanced synthetics, geogrids, and engineered polymer sheets are gradually replacing conventional compacted-gravel subgrade designs. For a fraction of the material weight and related supply chain carbon cost, these materials provide mechanical soil stabilization and comparable or better load-bearing capability.

Recent modifications to environmental waste management regulations, such as the fundamental Landfill Directive frameworks of the European Union, legally require the incorporation of continuous high-density polyethylene liners throughout new confinement cells. These flexible polymer barriers, which adhere to a baseline 1.5 mm to 2.5 mm thickness profile depending on chemical aggressiveness, are now codified civil standards required to prevent hazardous leachate migration into regional groundwater tables rather than serving as optional value-engineering substitutes.

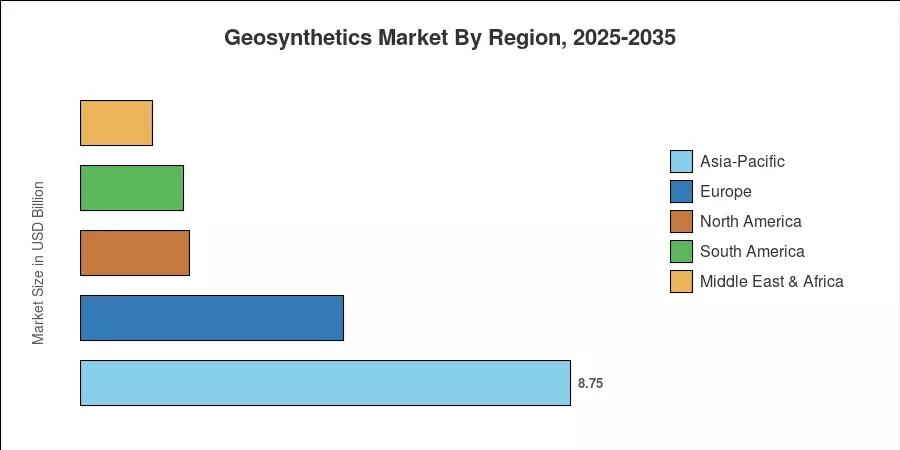

With almost 41% of 2025 revenue, Asia-Pacific leads the geosynthetics market, driven by spending on rail embankments and expressways in China and India. With a predicted 10.38% CAGR through 2035, the region is also the fastest-growing. With the help of DOT resilience retrofits and EPA Subtitle D liner upgrades, North America accounts for about 24% of worldwide demand. In comparison, Europe holds a 22% share thanks to flood defense upgrading and circular economy regulations. The geosynthetics market is positioned for steady double-digit growth in a few corridors through the mid-2030s as long as sovereign infrastructure pipelines continue to receive adequate funding.

Key Report Takeaways

• By Material

- Polypropylene, polyethylene, and polyester collectively commanded an 88% share of the Geosynthetics Market in 2025, underscoring the dominance of commodity polymers in civil works applications.

- Other materials—including polyamide and natural-fibre blends—are expanding from a narrow base as bio-based product certifications gain traction.

• By Type

- Geomembranes captured the single largest type-level share at roughly 37% of 2025 revenue, reflecting tightening containment regulations worldwide.

- Geotextiles remain the highest-volume category by area shipped, with woven variants gaining ground in road-separation applications across the Geosynthetics Market.

• By Function

- Reinforcement retained the leading functional share at approximately 29% in 2025, driven by mechanically stabilized earth wall projects.

- Containment and barrier functions posted the fastest functional CAGR at 9.78%, propelled by landfill and tailings-dam mandates.

• By Application

- Construction held the largest application share at roughly 40% of the 2025 Geosynthetics Market revenue.

- Transportation is projected to expand at a 9.73% CAGR through 2035, outpacing all other end-use verticals.

• By Geography

- Asia-Pacific accounted for 41% of 2025 revenue and is forecast to grow at a 10.38% CAGR—the fastest regional trajectory in the Geosynthetics Market.

- North America and Europe together represent 46% of global demand, anchored by regulatory compliance cycles.

Geosynthetics Market Size and Forecast (2021–2035)

Market sizing relies on a bottom-up aggregation of manufacturer shipments, distributor sell-through data, and public procurement databases across 42 countries, cross-validated against customs trade codes (HS 5911.90, 3921.90) and polymer resin consumption volumes. The Geosynthetics Market forecast applies segment-level growth assumptions tied to infrastructure pipeline visibility, regulatory phase-in schedules, and raw-material price indices.