Glass Fiber Reinforced Plastic GFRP Market Summary

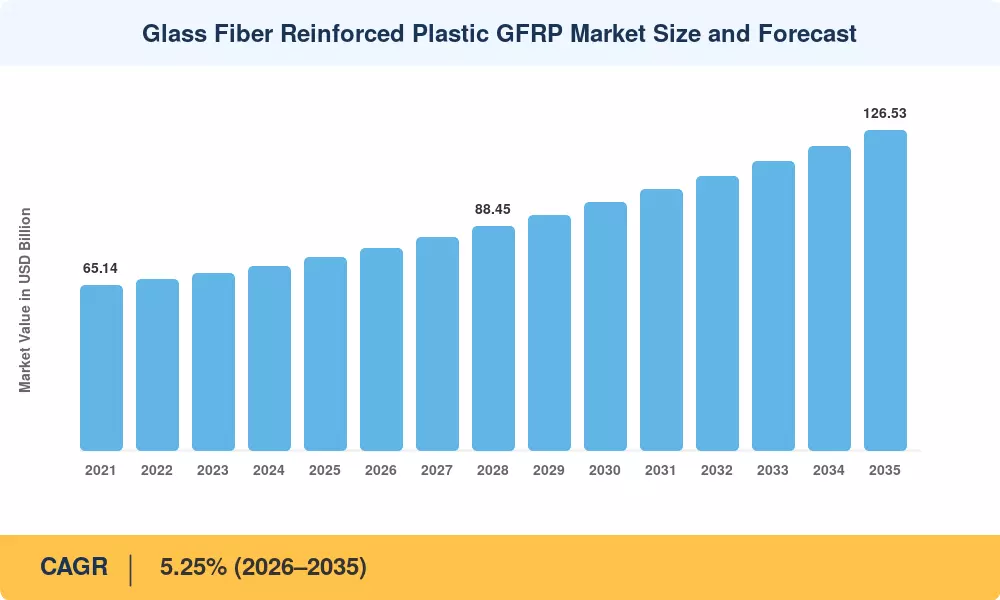

The Glass Fiber Reinforced Plastic Market reached an estimated USD 76.20 billion in 2025 and is projected to climb from USD 79.85 billion in 2026 to USD 126.53 billion by 2035, registering a 5.25% CAGR across the forecast window. Automotive electrification mandates and global offshore-wind capacity targets exceeding 380 GW by 2030 are channeling capital toward glass fiber composites that outperform steel and aluminum on strength-to-weight performance while resisting corrosion in marine and chemical environments[2]. Governments in the EU, China, and the United States have collectively earmarked more than USD 120 billion in green-infrastructure incentives since 2022, directly boosting demand for GFRP pipes, rebar, and cladding systems.

The Glass Fiber Reinforced Plastic market is undergoing a material revolution. Pultruded profiles are replacing traditional steel rebar, sheet-molding compounds are replacing aluminum body panels, and injection-molded GFRP components are replacing concrete utility poles. Polyester-resin solutions remain the cost leaders in high-volume production. Epoxy formulations are making inroads in aerospace spars and 700-bar hydrogen pressure tanks where fatigue resistance justifies premium pricing [3]. Automated compression-molding and continuous-pultrusion lines have reduced cycle times by 30–40% since 2021, helping producers to counter margin pressure from carbon-fiber price deflation and tighter occupational-health standards in the EU and North America.

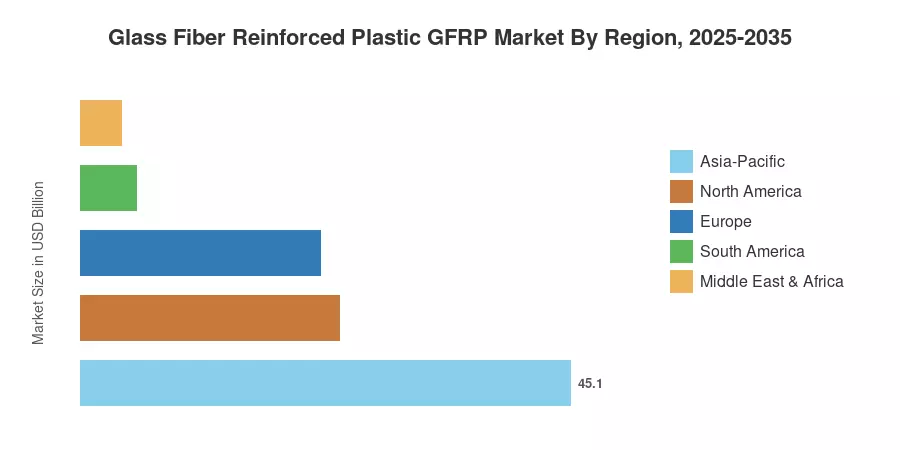

Asia-Pacific Glass Fiber Reinforced Plastic Market is dominant and accounts for over 45.1% of worldwide revenue in 2025, due to China’s construction boom and India’s developing wind-energy fleet. This region also has the fastest CAGR of 5.34% until 2035. North America (~23.8%) benefits from US infrastructure renovation under the Bipartisan Infrastructure Law, and Europe (~22.1%) is driven by Germany and the Nordic countries’ offshore-wind build-out. The Glass Fibre Reinforced Plastic Market is set for continued double-digit volume growth in niche areas through the mid-2030s, supported by expansion in hydrogen distribution networks and EV battery enclosures.

Key Report Takeaways

• By Resin Type

- Polyester resin held a 57.2% share of the Glass Fiber Reinforced Plastic Market in 2025, driven by cost-effective construction and infrastructure applications.

- Epoxy resin is forecast to expand at a 5.42% CAGR from 2026 to 2035, propelled by demand in aerospace and hydrogen-storage applications.

• By Process

- Compression molding accounted for 28.6% of the Glass Fiber Reinforced Plastic Market in 2025, serving as the backbone process for automotive and electrical enclosure manufacturing.

- Injection molding is projected to grow at a 5.32% CAGR through 2035, benefiting from faster cycle times and high-volume automotive production.

• By End-User Industry

- Construction and infrastructure commanded the largest end-user share of the Glass Fiber Reinforced Plastic Market in 2025, underpinned by corrosion-resistant rebar and cladding demand.

- Wind energy is anticipated to post the fastest growth at a 5.58% CAGR through 2035, reflecting offshore capacity additions globally.

• By Geography

- Asia-Pacific captured 45.1% of the Glass Fiber Reinforced Plastic Market in 2025 and leads all regions in forecast growth.

- North America is the second-largest region at 23.8% share, supported by federal infrastructure spending.

Glass Fiber Reinforced Plastic Market Size and Forecast (2021–2035)

MRFR’s predictions are based on a combination of primary interviews with 120+ industry leaders, trade-association shipment statistics, and proprietary demand modeling calibrated against customs records and resin-consumption levels. Historical figures (2021–2024) are based on actual reported data, 2025 is the base-year projection, and 2026–2035 values are anticipated in a moderate-growth scenario.