Distributed Control System Market Summary

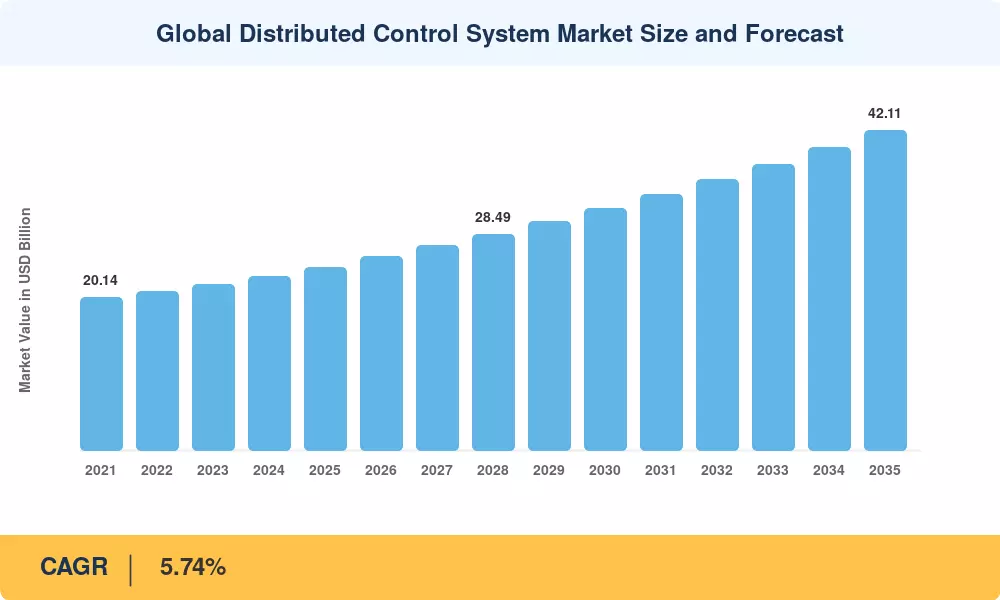

The Distributed Control System Market was valued at USD 24.10 billion in 2025 and is projected to grow from USD 25.48 billion in 2026 to USD 42.11 billion by 2035, expanding at a 5.74% CAGR during the forecast period. Two capital-intensive trends anchor this trajectory: a global wave of refinery brownfield retrofits — driven by tightening IEC 61511 functional-safety mandates [1] — and the rapid build-out of green-hydrogen electrolyzer trains that require tight closed-loop control across hundreds of I/O points [2]. Both catalysts channel sustained investment into controller hardware, engineering services, and increasingly, cloud-connected analytics software.

Many asset owners were not prepared for the rapid end-of-support of legacy proprietary control platforms installed in the 1990s and early 2000s. According to a 2024 ARC Advisory Group poll [3], hyperscale cloud providers currently collaborate with controller OEMs to provide consumption-based supervisory workloads, which can reduce commissioning timeframes by up to 35%. In the Distributed Control System Market, operators' allocation of capital versus operating budgets is changing as a result of the transition from periodic control-room upgrades to subscription-based predictive-maintenance modules.

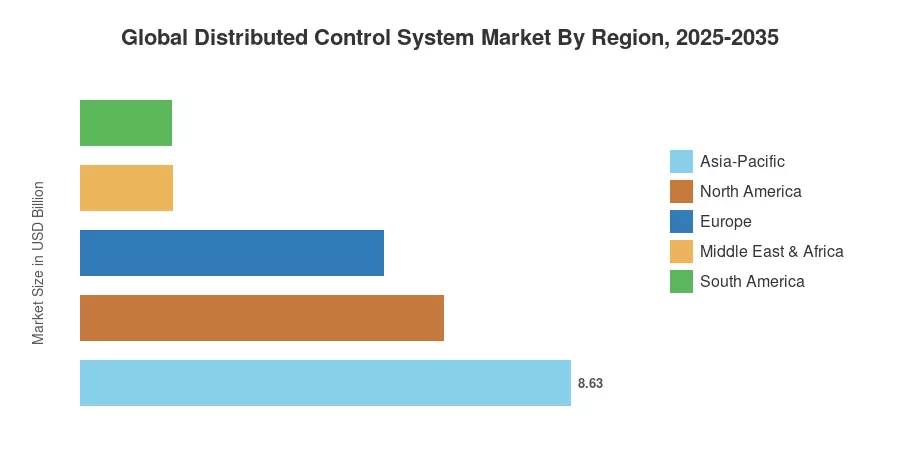

With 35.8% of the 2025 Distributed Control System Market, Asia-Pacific holds the biggest revenue share, driven by India's refinery capacity increases under the Hydrocarbon Vision 2030 program and China's coal-to-gas conversion regulations [4]. With a CAGR of 6.72%, the Middle East and Africa area is expected to grow at the fastest rate due to Saudi Arabia's efforts to diversify downstream. Due to carbon-capture retrofit spending along the U.S. Gulf Coast, North America has the second-largest share at 26.5%. The distributed control system market is set for ten years of consistent, policy-backed growth as decarbonization regulations tighten globally.

Key Report Takeaways

• By Component & Architecture

- Hardware accounted for 52.2% of the Distributed Control System Market in 2025, reflecting the capital-intensive nature of controller and I/O replacements.

- Software revenue is set to register a 6.38% CAGR through 2035 as containerized analytics and digital-twin subscriptions gain traction.

- Hybrid and distributed-hybrid architectures captured 43.5% of 2025 revenue, outpacing centralized designs.

• By Deployment

- On-premises installations held 79.3% of the Distributed Control System Market share in 2025.

- Cloud- and edge-hosted deployment configurations are forecast to grow at a 6.11% CAGR through 2035

• By End user

- Pharmaceuticals and life sciences verticals are expected to register a 7.62% CAGR, the fastest among end-use sectors.

• By Geography

- Asia-Pacific led the Distributed Control System Market with 35.8% of 2025 revenue.

- The Middle East & Africa region is projected to record the fastest regional CAGR of 6.72% through 2035.

Market Size and Forecast (2021–2035)

Market sizing relies on a bottom-up methodology combining controller-vendor shipment data, engineering-services revenue disclosures, and plant-level I/O-count databases. Historical figures (2021–2024) draw on audited annual reports, while forecast values (2026–2035) apply the calibrated 5.74% CAGR with adjustments for identified capex cycles.