Graphene Battery Market Summary

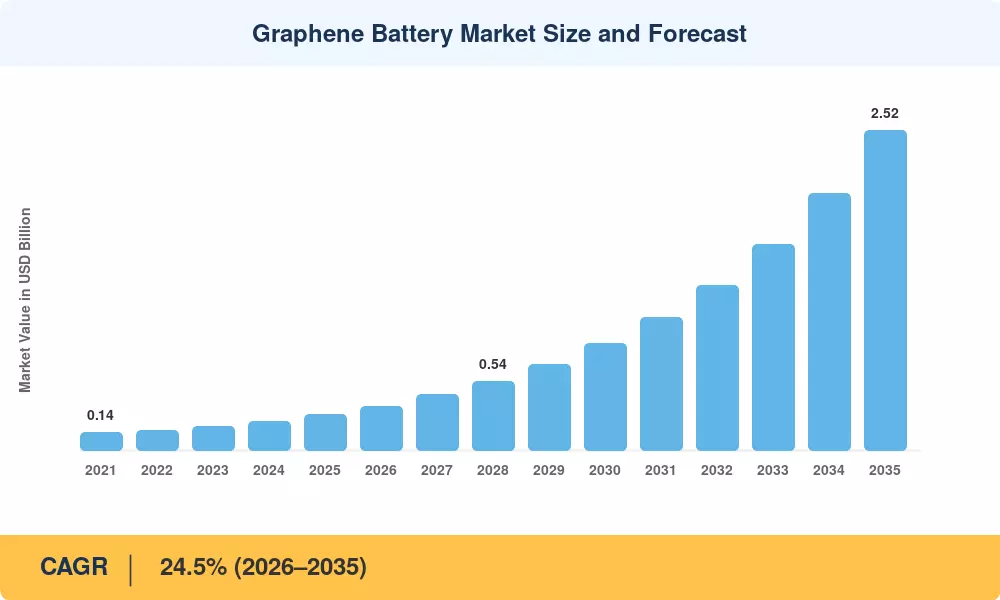

The Graphene Battery Market stood at USD 0.28 Billion in 2025 and is projected to reach USD 0.35 Billion in 2026 before climbing to USD 2.52 Billion by 2035, expanding at a compound annual growth rate of 24.5% over the forecast window. Policy-driven electrification mandates across China, the European Union, and California are compressing acceptable EV charging windows below fifteen minutes, creating urgent demand for electrode architectures that pair high energy density with rapid charge acceptance. The U.S. Department of Energy's USD 4 million grant to Lyten for pilot-scale graphene anode production signals that public capital is beginning to de-risk the technology at scale [1].

A generational shift in cell chemistry is now underway. Conventional carbon-black additives that have served lithium-ion cathodes for two decades are approaching performance ceilings, and graphene-enhanced electrodes offer a credible path to 350 Wh/kg cells that charge in under ten minutes. The EU's EUR 4.5 million GRAPHERGIA consortium and the U.S. Navy's SBIR Phase II holey-graphene anode contract confirm that both civilian and defense stakeholders view graphene integration as a strategic priority rather than a laboratory curiosity [2][3].

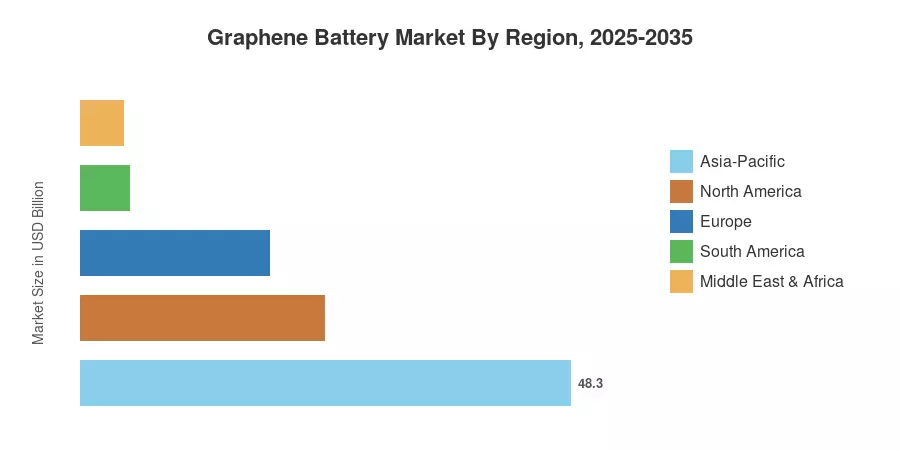

Asia-Pacific commands the largest share of the Graphene Battery Market at 48.3% of 2025 revenue, underpinned by China's dominance in cell manufacturing and South Korea's advanced materials ecosystem. The region also registers the fastest forecast CAGR at 25.8% through 2035. North America holds the second-largest share at 24.1%, buoyed by defense procurement and venture-backed startups. Europe trails at 18.6% yet benefits from the EU Battery Regulation's sustainability mandates that favor graphene's recyclability profile. As electrochemical exfoliation costs fall toward parity with carbon black, tier-one cell makers across all three regions are expected to accelerate qualification timelines through the late 2020s [4][5].

Key Report Takeaways

• By Battery Chemistry

- Lithium-Ion Graphene Batteries captured 58.4% of the Graphene Battery Market revenue in 2025, driven by drop-in compatibility with existing gigafactory lines.

- Solid-State Graphene Batteries are forecast to register the highest segment CAGR through 2035, reflecting breakthrough potential in solid electrolyte integration.

- Graphene Supercapacitors accounted for USD 0.04 Billion in 2025 as grid-edge and regenerative braking use cases gained traction.

• By Application

- Automotive led the Graphene Battery Market with 45.2% revenue share in 2025, supported by OEM partnerships targeting sub-15-minute fast charging.

- Energy Storage is positioned as the fastest-expanding application through 2035, fueled by grid-scale deployment mandates and behind-the-meter installations.

- Consumer Electronics generated steady demand through premium smartphone and laptop integrations.

• By Region

- Asia-Pacific dominated the Graphene Battery Market with 48.3% share in 2025, led by Chinese cell manufacturers and Japanese materials suppliers.

- North America contributed 24.1% of global revenue, anchored by U.S. defense programs and DOE-backed pilot facilities.

- Europe accounted for 18.6% of the Graphene Battery Market, with the EU Battery Regulation creating preferential conditions for graphene-enhanced chemistries.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework synthesizes primary interviews with cell manufacturers, graphene producers, and OEM procurement teams alongside secondary datasets from national energy agencies, patent filings, and trade databases. All figures are calibrated to the most recent available data as of Q1 2026.