Green Building Materials Market Summary

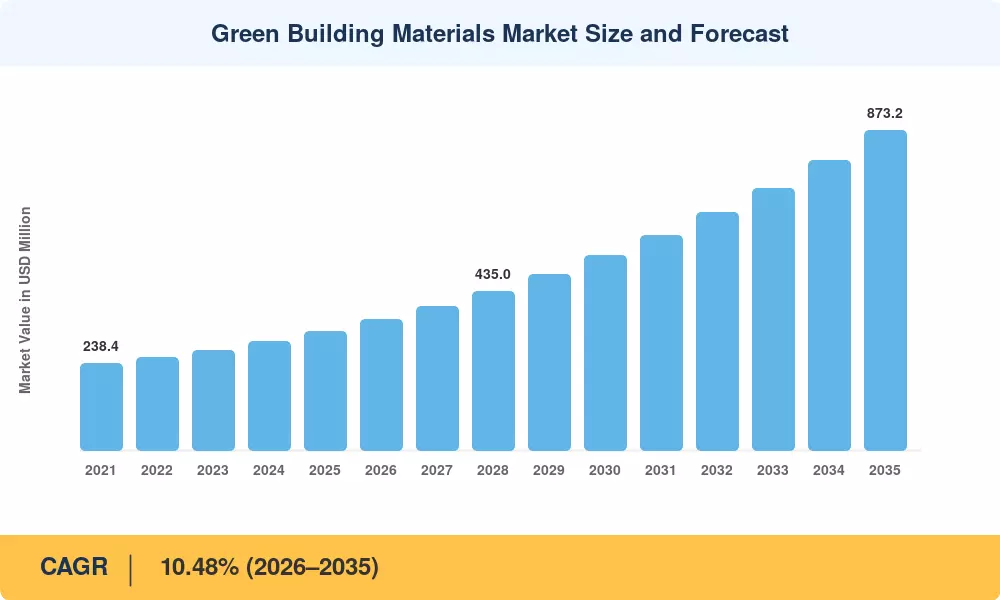

The Green Building Materials Market was valued at USD 324.50 Million in 2025 and is projected to grow from USD 356.30 Million in 2026 to USD 873.20 Million by 2035, registering a CAGR of 10.48% during the forecast period (2026–2035). Federal procurement mandates in the United States now require Environmental Product Declarations (EPDs) for all materials used in publicly funded construction exceeding USD 35 Million, a threshold that channeled an estimated USD 12 Billion in institutional spending toward verified low-carbon suppliers in 2024 alone [1]. Europe's Digital Product Passport regulation, scheduled for full enforcement by 2028, is further accelerating the shift toward traceable, third-party-certified building inputs [2].

Material science is undergoing a generational transition within the Green Building Materials Market. Conventional Portland cement — responsible for roughly 8% of global CO₂ emissions — is ceding ground to calcined-clay blends and geopolymer binders that cut embodied carbon by up to 40% [3]. Mass-timber framing, once confined to low-rise residential projects, now appears in commercial structures exceeding 18 stories, supported by updated International Building Code provisions adopted across 14 U.S. states [4]. Cellulose insulation derived from post-consumer newsprint is displacing fiberglass in retrofit applications, driven by vapor-permeability requirements in revised energy codes.

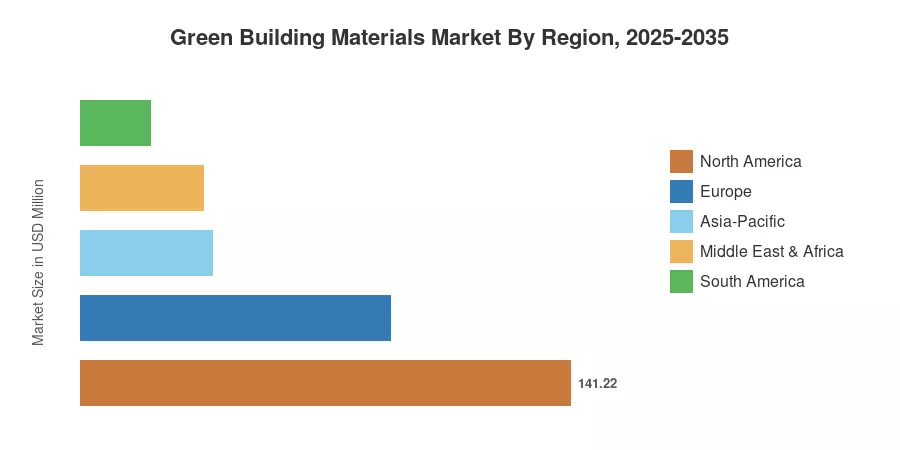

North America commands a 43.52% share of the Green Building Materials Market, anchored by Buy Clean mandates and LEED-driven institutional procurement. Asia-Pacific is the fastest-growing region with a projected 11.76% CAGR through 2035, as China's 14th Five-Year Plan targets 50% certified green urban construction by 2030 [5]. Europe holds the second-largest share at approximately 27.50%, propelled by the EU Taxonomy Regulation and Renovation Wave strategy. The convergence of tightening carbon budgets and urbanization in developing economies positions this market for sustained double-digit expansion through the next decade.

Key Report Takeaways

• By Material Type

- Low-Carbon Concrete and Cement led the Green Building Materials Market with a 25.89% revenue share in 2025, driven by federal EPD mandates and carbon border adjustments

- Cellulose and Bio-Foam Insulation is advancing at an 11.24% CAGR through 2035, outpacing traditional fiberglass as vapor-permeability codes tighten

• By Application

- Framing captured 24.78% of the Green Building Materials Market share in 2025, reflecting mass-timber adoption in mid-rise commercial construction

- Insulation is forecast to expand at a 10.82% CAGR through 2035 as retrofit mandates scale across North America and Europe

• By End-Use Industry

- Residential construction accounted for 42.45% of 2025 demand in the Green Building Materials Market, supported by green mortgage incentive programs

- Commercial projects are projected to grow at a 10.67% CAGR to 2035 as tenant ESG specifications penalize high-carbon finishes

• By Region

- North America leads the Green Building Material Market with a 43.52% of 2025 revenue share.

- Asia-Pacific is poised to register an 11.76% CAGR through 2035, making it the fastest-expanding region within the Green Building Material Market.

Green Building Materials Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining bottom-up revenue analysis of manufacturer shipments, top-down validation against national construction spending databases (U.S. Census Bureau, Eurostat, China NBS), and cross-referencing with EPD registry filings across 40+ countries. Historical figures (2021–2024) reflect audited shipment data; 2025 is the base-year estimate; 2026–2035 values are forecast at a constant 10.48% CAGR.