Home Decor Market Summary

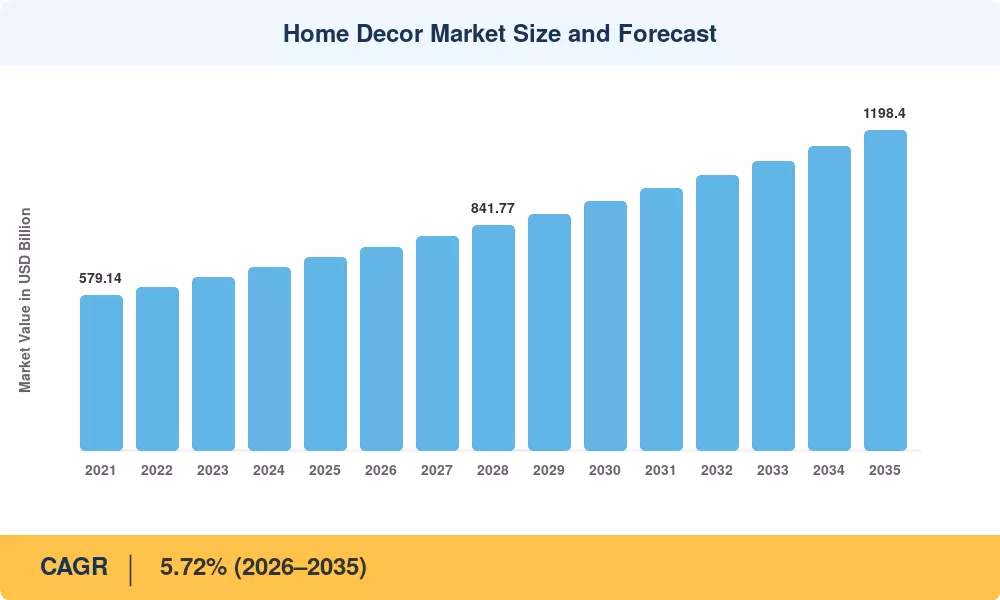

The Home Decor Market stood at an estimated USD 723.52 Billion in 2025 and is projected to reach USD 761.18 Billion in 2026, climbing to USD 1,198.40 Billion by 2035 at a CAGR of 5.72% during 2026–2035. Rising disposable incomes across emerging economies and a cultural shift toward curated living spaces have turned interior decoration products into a priority household spend rather than a discretionary afterthought. Government-backed housing stimulus programs — including India's Pradhan Mantri Awas Yojana targeting 20 million urban housing units and the US Inflation Reduction Act's energy-efficient home improvement incentives — are amplifying downstream demand for home furnishing and styling across both new-build and renovation channels [2].

Technology is rewriting how consumers discover and purchase wall art and decorative accessories. Augmented-reality visualization tools now let shoppers place virtual furniture in their rooms before buying, cutting return rates by up to 25% according to Shopify's 2024 commerce report [3]. Smart-home integration has expanded the definition of decorative lighting and rugs to include voice-controlled ambient systems and sensor-embedded textiles, blurring the line between function and aesthetics. Retailers like Wayfair and IKEA have invested over USD 1.2 billion collectively in AI-driven personalization engines that tailor seasonal home decoration items to individual browsing patterns [4].

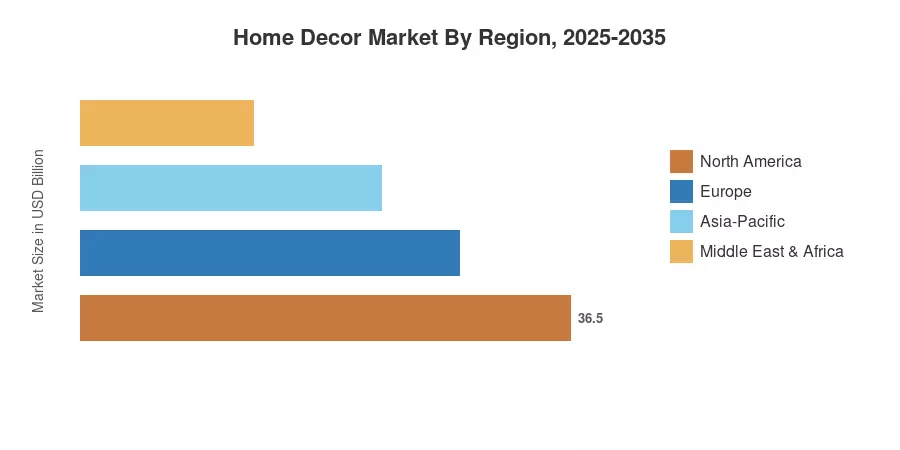

North America retained a commanding 44.89% share of the Home Decor Market in 2025, anchored by the mature renovation culture in the United States and Canada. Asia-Pacific is the fastest-growing region, advancing at an 8.76% CAGR through 2035, propelled by rapid urbanization in China and India. Europe held the second-largest share at approximately 24.3%, buoyed by sustainability-driven purchasing in Germany and the Nordic countries As hybrid work arrangements solidify, the Home Decor Market is poised for sustained expansion driven by consumers investing more in spaces where they live and work.

Key Report Takeaways

• By Product Category

- Floor coverings captured 38.27% of the Home Decor Market share in 2025, driven by laminate and luxury vinyl tile adoption in residential remodeling projects

- Textiles — including curtains, throws, and cushion covers — are forecast to grow at a 7.84% CAGR through 2035 as consumers refresh interior decoration products more frequently

- Furniture remains the largest revenue contributor to the Home Decor Market, valued at approximately USD 215.60 Billion in 2025

• By Distribution Channel

- Specialty stores held 49.38% share of the Home Decor Market in 2025, underscoring the continued importance of tactile, showroom-based purchasing for home furnishing and styling

- DIY and mass merchandisers are projected to register the fastest CAGR at 8.52% through 2035, as big-box retailers expand curated wall art and decorative accessories sections

• By Region

- North America led with 44.89% of the Home Decor Market in 2025

- Asia-Pacific is advancing at an 8.76% CAGR through 2035, with decorative lighting and rugs demand surging across tier-2 cities in India and Southeast Asia

Home Decor Market Size and Forecast (2021–2035)

MRFR's market sizing combines top-down revenue analysis from company filings with bottom-up demand modeling across product categories and distribution channels. Historical data (2021–2024) draws on verified trade statistics, retailer disclosures, and customs data. Forecast projections (2026–2035) apply econometric modeling calibrated against housing starts, consumer confidence indices, and e-commerce penetration trends across 32 countries.