Home Remodeling Market Summary

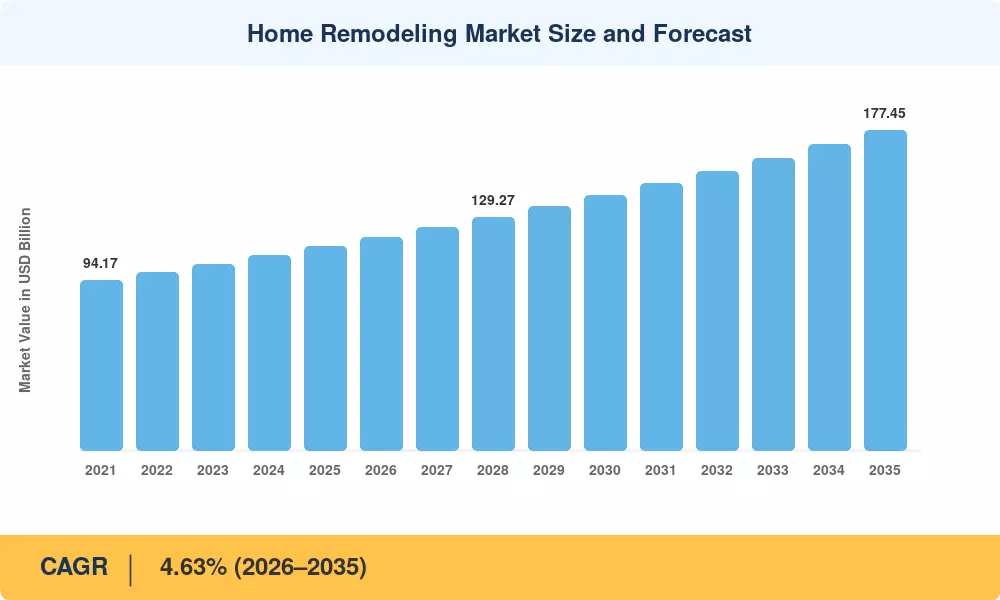

The home remodeling market reached an estimated USD 112.86 trillion in 2025, positioning it among the largest segments within the global construction and real estate ecosystem. Starting from a projected USD 118.09 trillion in 2026, the home remodeling market is forecast to expand at a CAGR of 4.63% through 2035, reaching approximately USD 177.45 trillion by the end of the forecast period. Rising disposable incomes across both developed and emerging economies, combined with aging housing stock in North America and Europe, are anchoring sustained demand for kitchen and bathroom renovation, structural upgrades, and energy-efficient retrofits [2].

A pronounced technology shift is reshaping how homeowners and residential remodeling contractors approach projects. Legacy pen-and-paper estimating is giving way to 3D visualization software, augmented reality room planners, and AI-driven home renovation cost and planning tools. The U.S. Department of Energy's Weatherization Assistance Program alone allocated over USD 3.5 billion during 2022–2025 to support home improvement and repair for low-income households, while the EU renovation wave targets aim to double building renovation rates by 2030 [3][4].

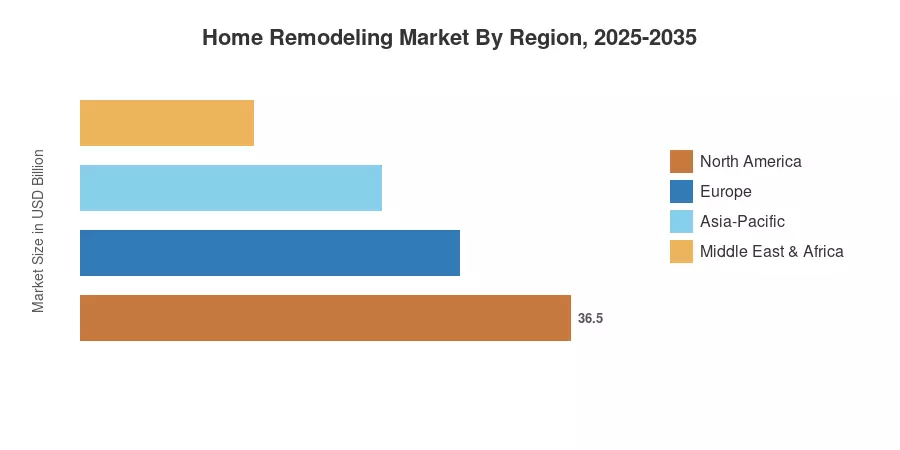

North America commands roughly 35% of the global home remodeling market, driven by high homeownership rates and robust contractor infrastructure. Asia-Pacific is the fastest-growing region with a projected CAGR near 5.4%, fueled by urbanization in China, India, and Southeast Asia. Europe holds approximately 27% share, supported by stringent energy-efficiency mandates and green building incentives. The next decade will reward players who blend digital design platforms with sustainable material supply chains

Key Report Takeaways

• By Project Type

- Professional remodeling accounts for roughly 62% of the home remodeling market, reflecting homeowner preference for licensed residential remodeling contractors on high-value structural work

- DIY home remodeling projects are growing at a CAGR of approximately 5.1%, boosted by online tutorial ecosystems and big-box retailer tool-rental programs

• By Application

- Kitchen and bathroom renovation remains the highest-revenue application segment, valued at over USD 31 trillion in 2025

- Windows and Doors is the fastest-growing application subsegment in the home remodeling market, registering a CAGR near 5.3%

• By Region

- North America leads with a 35% share, underpinned by USD 4.2 trillion in annual spending on home improvement and repair

- Asia-Pacific is projected to add over USD 18 trillion in incremental value through 2035

Market Size and Forecast (2021–2035)

MRFR's market sizing draws on primary interviews with residential remodeling contractors, distributor channel audits, government housing statistics, and proprietary demand modeling calibrated against census and building-permit data across 42 countries.

.webp?v=1783427189)