Human Augmentation Market Summary

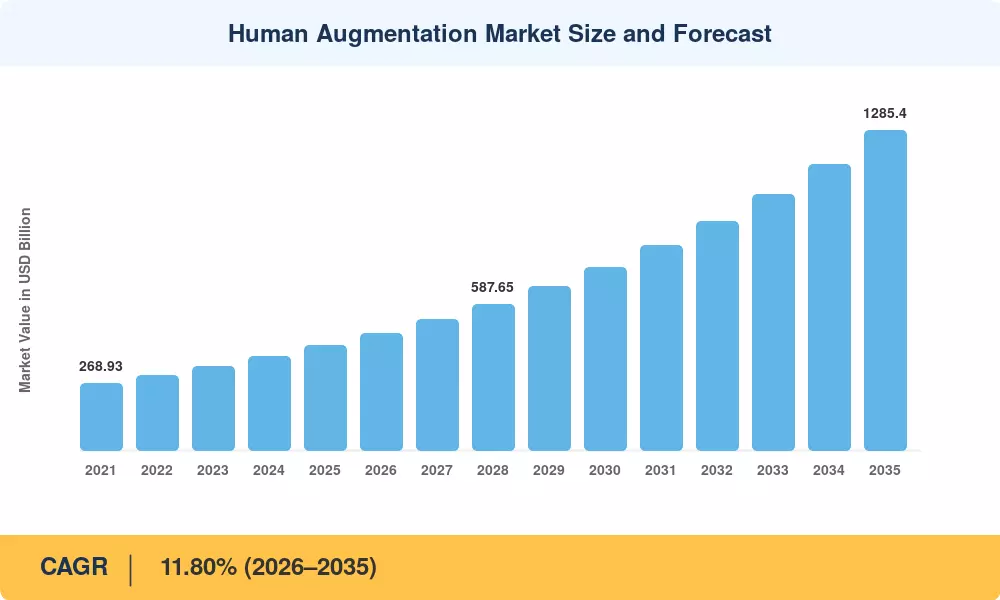

The Human Augmentation Market reached an estimated USD 420.18 billion in 2025 and is projected to grow from USD 469.76 billion in 2026 to USD 1,285.40 billion by 2035, registering a CAGR of 11.80% across the forecast period (2026–2035). Two catalysts anchor this trajectory: annual corporate R&D commitments exceeding USD 88 billion into augmentation platforms, and the U.S. Centers for Medicare & Medicaid Services' landmark decision to reimburse personal exoskeleton technology prescriptions under durable medical equipment codes[2]. These policies and capital signals confirm that the Human Augmentation Market has moved decisively from prototype laboratories into regulated commercial deployment.

A sweeping technology shift is replacing passive prosthetics and manual rehabilitation tools with AI-driven bionic implants and adaptive cognitive augmentation devices. Between 2023 and 2025, the FDA granted more than 45 breakthrough device designations to neural-interface and wearable technology enhancement products, compressing approval timelines by roughly 40% [3]. Corporate venture arms—led by Alphabet, Samsung, and Medtronic—collectively deployed over USD 12 billion in Series B-and-later rounds targeting human-machine interface start-ups during 2024 alone [4].

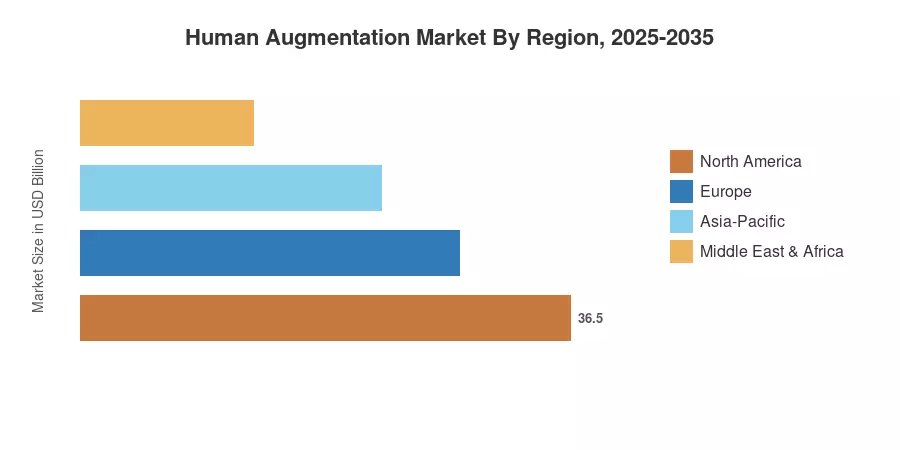

North America commands a dominant 36.20% revenue share of the Human Augmentation Market, buoyed by defense procurement cycles and a mature reimbursement ecosystem. Asia-Pacific is the fastest-growing region, advancing at a 23.30% CAGR through 2035 as China, India, and South Korea expand national assistive-technology programs. Europe holds the second-largest share at roughly 27.50%, propelled by the EU's Horizon Europe grants earmarked for exoskeleton technology and cognitive augmentation devices As regulatory frameworks mature and component costs decline, the Human Augmentation Market is poised to integrate into everyday healthcare, industrial, and consumer environments over the coming decade.

Key Report Takeaways

• By Product Type

- Wearable devices led the Human Augmentation Market with a 58.70% share in 2024, driven by enterprise adoption of AR headsets and medical-grade biosensors

- Smart exoskeletons are forecast to post the highest product-type CAGR at 23.90% through 2035, reflecting industrial safety mandates and rehabilitation demand

- Prosthetics segment revenue reached approximately USD 42.50 billion in 2024, underpinned by growing acceptance of myoelectric and bionic implants

• By Functionality

- Physical augmentation accounted for 43.80% of the Human Augmentation Market in 2024, spanning exoskeleton technology, powered orthoses, and haptic wearable technology enhancement systems

- Cognitive augmentation is advancing at a 25.80% CAGR to 2035, fueled by neural-feedback headbands and AI-powered cognitive augmentation devices

• By Region

- North America contributed USD 152.10 billion to the Human Augmentation Market in 2024

- Asia-Pacific is set to accelerate at a 23.30% CAGR, led by China's "Made in China 2025" assistive-robotics allocations and India's National Policy on Assistive Devices

- Europe captured approximately 27.50% share, anchored by Germany's Industry 4.0 exoskeleton technology pilots

Market Size and Forecast (2021–2035)

MRFR's market sizing draws on a triangulated approach combining bottom-up revenue tracking across 120+ companies, top-down macroeconomic modeling using WHO disability prevalence data and defense spending forecasts, and cross-validation with regulatory filing databases. Historical figures (2021–2024) reflect reported revenues; the 2025 base year blends Q1–Q3 actuals with Q4 estimates; forecast years (2026–2035) apply the calibrated 11.80% CAGR with year-specific adjustments for known policy triggers and supply-chain events.

.webp?v=1784639825)