Hydration Backpack Market Summary

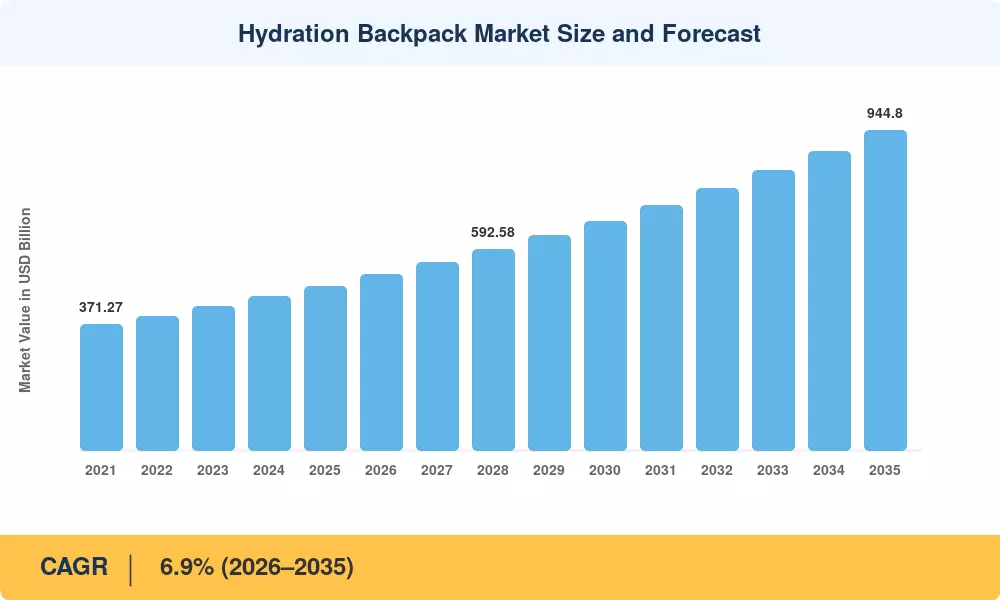

The global hydration backpack market reached an estimated USD 485.2 million in 2025 and is projected to grow from USD 518.7 million in 2026 to USD 944.8 million by 2035, registering a CAGR of 6.9% during the forecast period. Rising participation in endurance sports and organized trail events has accelerated demand for every type of hands-free water carrying system. Government fitness initiatives across the EU and Asia-Pacific — including India's Fit India Movement and the European Week of Sport — have pushed outdoor recreation participation rates above 55% in key demographics, feeding directly into hydration gear sales [2].

Product innovation is reshaping this category. Legacy rigid-frame packs are giving way to lightweight, ergonomic designs featuring advanced hydration reservoir bladder pack configurations with antimicrobial linings and quick-disconnect valves. CamelBak alone invested over USD 12 million in R&D between 2023 and 2025 to develop insulated hydration pack system technologies that maintain water temperature for up to four hours across extreme conditions [3]. Running and cycling hydration vest formats now account for a fast-growing share of new product launches, driven by the ultramarathon and gravel cycling boom.

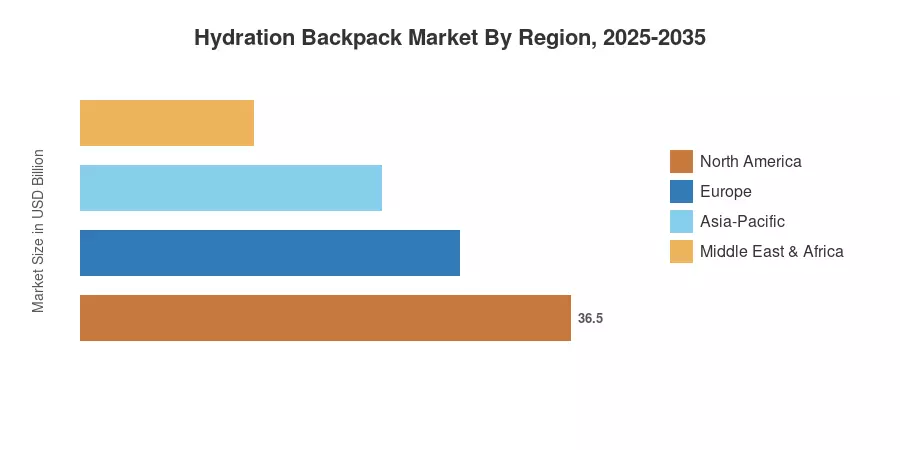

North America commands approximately 38% of the hydration backpack market, anchored by a deep outdoor recreation culture in the United States and Canada. Asia-Pacific is the fastest-growing region with a projected CAGR of 8.2%, fueled by expanding middle-class participation in trekking and trail running, and hydration backpack adoption across China, India, and South Korea. Europe holds the second-largest share at roughly 27%, supported by Alpine sports infrastructure and sustainability-conscious consumers demanding BPA-free, recyclable bladder systems. The decade ahead points to continued premiumization and channel diversification across every region.

Key Report Takeaways

• By End User (Sports Activity)

- Running leads the hydration backpack market with approximately 34% revenue share in 2025, driven by marathon and ultramarathon participation surges globally

- Cycling is the fastest-growing end-user segment at 7.8% CAGR, as gravel and bikepacking disciplines fuel demand for slim-profile running and cycling hydration vest designs

- Trekking and hiking collectively represent over USD 190 million in 2025 revenue, sustained by national park visitation records across North America and Europe

• By Distribution Channel

- Online retail stores capture the dominant share of the hydration backpack market at roughly 41%, reflecting e-commerce penetration and DTC brand strategies

- Specialist retailers maintain a 7.4% CAGR as experiential retail and expert fitting services differentiate brick-and-mortar from pure-play digital channels

• By Region

- North America holds approximately 38% share — the United States alone represents over USD 155 million in 2025 value

- Asia-Pacific registers the highest regional CAGR at 8.2%, with China and India as primary growth engines for trail running hydration backpack adoption

- Europe's hydration backpack market is valued at an estimated USD 131 million in 2025, supported by Alpine and Nordic outdoor sports traditions

Hydration Backpack Market Size and Forecast (2021–2035)

MRFR's market sizing integrates primary interviews with 120+ hydration gear manufacturers, distributors, and retail buyers, supplemented by trade shipment data, customs databases, and secondary validation against published industry benchmarks. All figures are in USD millions at constant 2025 exchange rates.

.webp?v=1783427188)