Hydroponics Market Summary

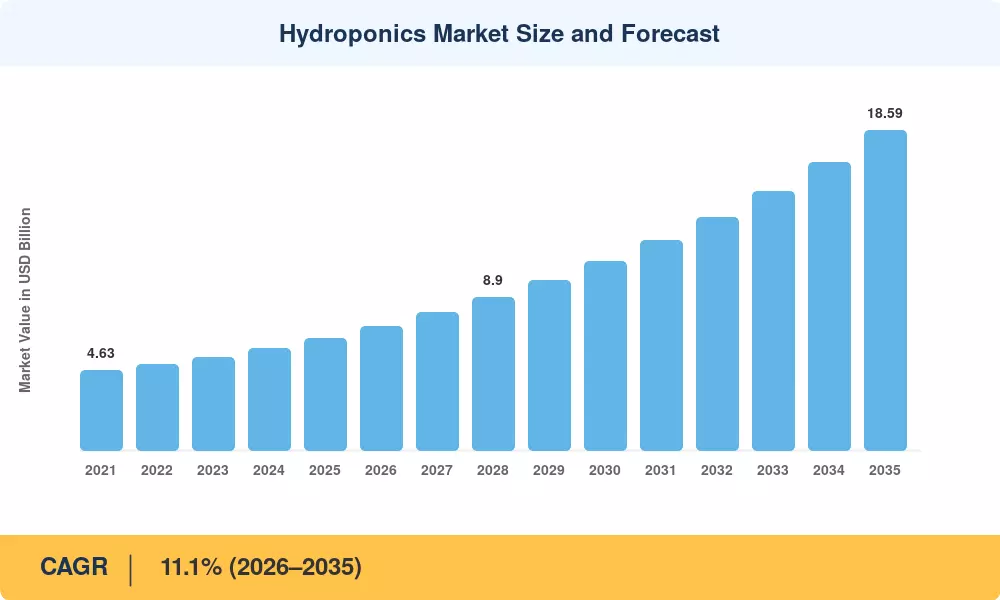

The Hydroponics Market reached an estimated USD 6.50 Billion in 2025 and is projected to grow from USD 7.21 Billion in 2026 to USD 18.59 Billion by 2035, registering a CAGR of 11.1% across the forecast period. Structural constraints on arable land, rising municipal water costs, and climate volatility are pushing commercial growers toward closed-loop cultivation at an accelerating pace. The USDA's Specialty Crop Research Initiative, which channels roughly USD 10 million per year into controlled-environment agriculture studies, has repositioned the Hydroponics Market from an experimental niche to a recognized food-security infrastructure [1].

A measurable technology transition is underway. Legacy open-field and soil-based greenhouse operations are giving way to sensor-integrated, climate-controlled hydroponic facilities that recirculate up to 90% of irrigation water. Private-equity investment in indoor farming exceeded USD 1.3 billion globally in 2024, underscoring institutional confidence in the Hydroponics Market trajectory [2]. LED spectral-tuning platforms now allow growers to manipulate crop cycle length and nutrient density, a capability that traditional agriculture cannot replicate at comparable cost.

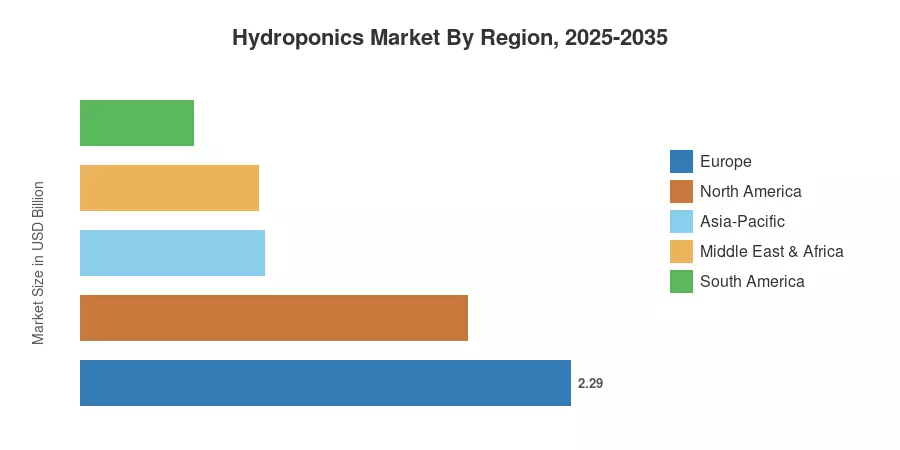

Europe commands the largest regional share of the Hydroponics Market at approximately 35.2% of global value in 2025, driven by the Netherlands' dense greenhouse infrastructure and the EU Farm to Fork Strategy's pesticide-reduction mandates [3]. Asia-Pacific is the fastest-growing region with a projected CAGR of 13.2%, fueled by urban food-security programs in China, Japan, and South Korea. North America holds the second-largest share at roughly 27.8%, supported by retailer demand for year-round domestic leafy-green supply. The convergence of carbon-credit monetization and renewable-energy integration positions the Hydroponics Market for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Production System

- Greenhouse hydroponics accounted for 63.0% of the Hydroponics Market in 2025, reflecting decades of accumulated infrastructure in the Netherlands, Spain, and North America.

- Indoor vertical farms are forecast to expand at a 14.3% CAGR through 2035, driven by urban food-security mandates and retailer traceability requirements.

• By Crop Type

- Leafy greens captured 44.0% of Hydroponics Market value in 2025, led by lettuce, spinach, and kale cultivars optimized for recirculating systems.

- Herbs and microgreens are projected to advance at a 13.4% CAGR to 2035, pulled by biopharma and premium foodservice demand.

• By Production Scale

- Large commercial operations held 52.0% of the Hydroponics Market share in 2025, leveraging purchasing power in lighting, substrates, and nutrient chemistry.

- Small-scale systems are projected to grow at a 14.4% CAGR between 2026 and 2035 as modular plug-and-play kits lower entry barriers.

• By Equipment

- Lighting systems accounted for 46.5% of Hydroponics Market equipment expenditure in 2025, reflecting ongoing LED adoption and spectral-tuning upgrades.

• By Region

- Europe led the Hydroponics Market with a 35.2% share in 2025, while Asia-Pacific is forecast to register the fastest CAGR of 13.2%.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up revenue aggregation from equipment suppliers, nutrient-solution vendors, and commercial growers with top-down validation against national agricultural trade statistics. Historical figures (2021–2024) are based on reported revenues; 2025 is the base-year estimate; 2026–2035 values represent forecast projections at the stated CAGR.

.webp?v=1783518754)