Agricultural Enzymes Market Summary

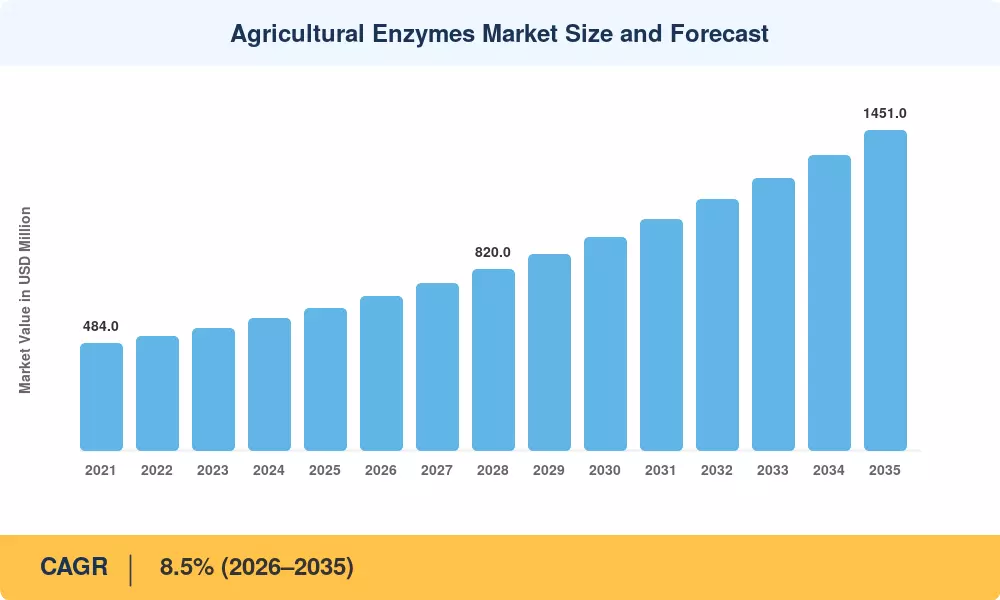

The Agricultural Enzymes Market was valued at USD 642 million in 2025 and is projected to reach USD 697 million in 2026 before climbing to USD 1,451 million by 2035, registering a CAGR of 8.5% during the 2026–2035 forecast window. Two forces are converging to drive this expansion: tightening pesticide-residue regulations across the EU and North America, and a sharp rise in public-sector funding for sustainable agriculture. The European Commission's Farm to Fork strategy alone targets a 50% reduction in chemical pesticide use by 2030, opening a widening lane for enzyme-based alternatives [2].

Bio-catalytic enzyme formulations, which may release bound phosphorus, speed up cellulose breakdown, and improve nutrient cycling without leaving hazardous residues, are gradually displacing conventional synthetic soil conditioners and chemical growth accelerators. Enzyme manufacturing costs are being reduced by 20–30% in comparison to 2020 benchmarks thanks to commercial-scale precision fermentation facilities, several of which are supported by expenditures surpassing USD 200 million [3]. Multi-enzyme cocktails customized for particular crop-soil systems can now be commercialized more quickly thanks to AI-driven protein engineering platforms, which have reduced development schedules from five years to less than eighteen months [4].

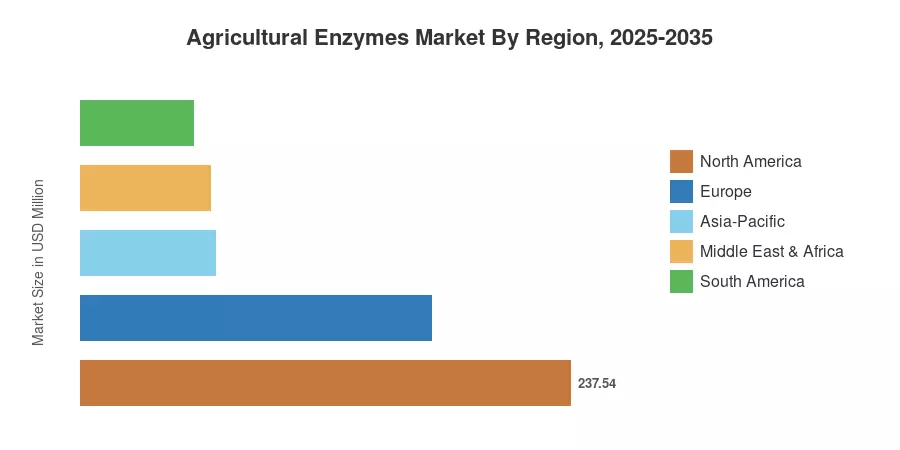

Driven by high-input row-crop agriculture and robust biotech infrastructure, North America held the highest share of the Agricultural Enzymes Market in 2025, at over 37%. With a predicted 10.2% CAGR through 2035, Asia-Pacific is the fastest-growing region as China and India direct subsidies into biologicals that increase yield [5]. Due to strict pesticide-reduction laws and the quick adoption of integrated pest management practices, Europe gained the second-largest share, at about 26.5%. The agricultural enzymes market is expected to change significantly over the course of the next ten years due to the confluence of cost-competitive fermentation, digital agronomy, and regulatory pressure.

Key Report Takeaways

• By Enzyme Type

- Phosphatases led the Agricultural Enzymes Market with approximately 39% share in 2025, driven by phosphorus-mobilization demand in nutrient-depleted soils.

- Cellulases are projected to register the fastest CAGR at 14.0% through 2035, reflecting expanded use in crop-residue management and composting acceleration.

• By Formulation & Application

- Liquid formulations accounted for roughly 49% of the Agricultural Enzymes Market in 2025, favored for drip-irrigation and foliar-spray compatibility.

- Crop protection applications are expected to expand at a 12.1% CAGR, fueled by biopesticide integration mandates in the EU and California.

• By Geography

- North America dominated with a 37% share of the Agricultural Enzymes Market, underpinned by mature distribution networks and biotech R&D clusters.

- Asia-Pacific is forecast to grow at a 10.2% CAGR as government subsidy programs in India and Southeast Asia drive adoption among smallholder farmers.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates bottom-up revenue estimates from enzyme manufacturers, import-export trade data, and top-down validation against crop-input spending tracked by the FAO and USDA. Historical figures reflect reported revenues adjusted for currency fluctuations, while forecast values apply a calibrated compound growth trajectory anchored to the 2025 base year.

.webp?v=1783929907)