Dairy Enzymes Market Summary

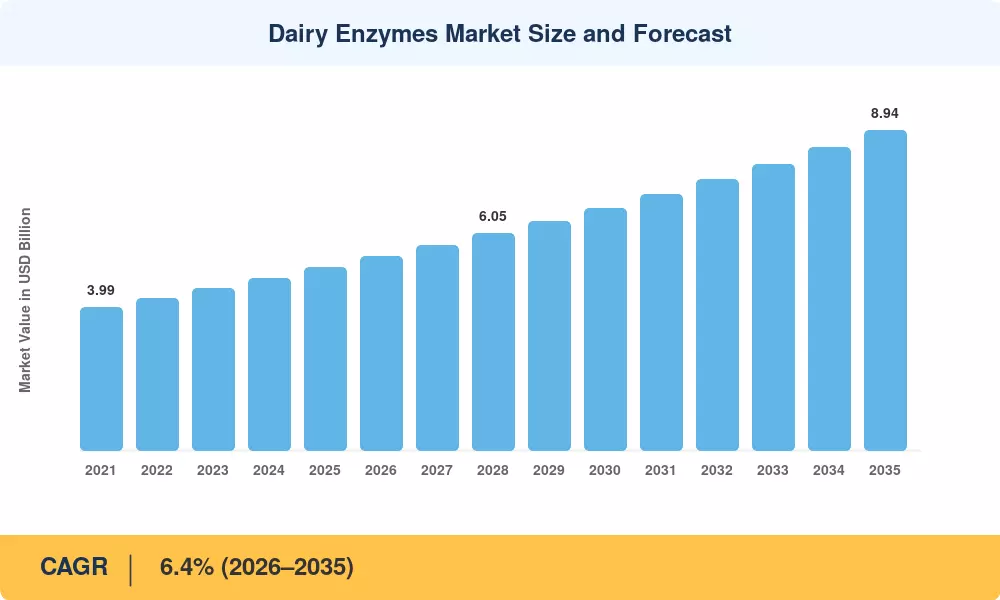

The Dairy Enzymes Market reached an estimated USD 5.12 billion in 2025 and is projected to grow from USD 5.45 billion in 2026 to USD 8.94 billion by 2035, registering a CAGR of 6.4% during 2026–2035. Two catalysts anchor this trajectory: rising global per-capita dairy consumption—up roughly 1.8% annually across developing economies [1]—and tightening food-safety regulations that push processors toward standardized enzyme dairy processing technology over traditional chemical treatments. The European Commission's updated food-enzyme authorization framework (Regulation EC 1332/2008, amended 2024) has accelerated reformulation timelines for hundreds of dairy SKUs, pulling forward capital expenditure cycles across the bloc [2].

Conventional cheesemaking and yogurt production used animal-derived coagulants and batch-level fermentation control. Today, microbial and recombinant fermentation platforms offer consistent rennet coagulation enzyme and lipase dairy taste enzyme preparations at scale, leading to dose variability reductions of up to 40% [3]. In 2024 alone, Novozymes invested more than USD 180 million in enzyme R&D, much of it in dairy applications [4]. The change of the Dairy Enzymes Market from animal-sourced to precision-fermented enzyme portfolios is the key technical transformation through 2035.

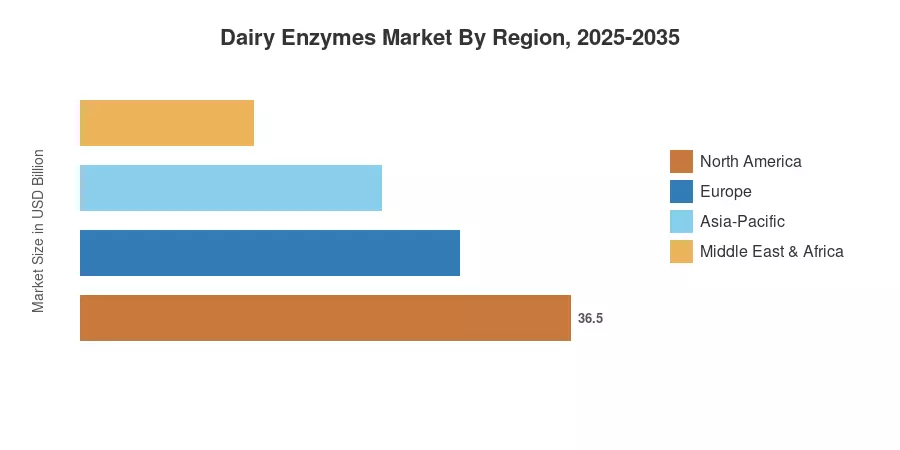

Europe holds the highest proportion of around 34% of the global revenue in the concentrated cheese and fermented-dairy market. Asia-Pacific is the fastest growing market with a predicted CAGR 8.1% driven by increasing protease dairy protein processing capacity in India and China North America represents the second-largest market of around 27%, driven by clean-label reformulation trends and the high demand for lactase cheese ripening enzyme from lactose-free dairy brands. The Dairy Enzymes Market is approaching a decade where biotechnology innovation and regulatory harmonization will jointly dictate the competitive posture.

Key Report Takeaways

• By Enzyme Type

- Rennet and coagulants lead the Dairy Enzymes Market with an estimated 38% revenue share in 2025, reflecting cheese's dominance in global dairy value chains

- Lipase enzymes are forecast to grow at a CAGR of 7.2% through 2035, propelled by demand for accelerated cheese ripening and specialty flavor profiles

- Lactase preparations represent approximately USD 0.87 billion in 2025 revenue, driven by the lactose-free dairy boom

• By Application

- Cheese production accounts for over 42% of total enzyme consumption in the Dairy Enzymes Market, far exceeding other dairy categories

- Yogurt and fermented milk applications are projected to reach USD 1.58 billion by 2035

- Infant formula and nutritional dairy segments show a CAGR of 7.8%, the fastest among application verticals

• By Region

- Europe's Dairy Enzymes Market dominance stems from its ~USD 1.74 billion contribution in 2025

- Asia-Pacific's 8.1% CAGR outpaces all other regions, with India and China as primary growth engines

- North America maintains a 27% global share, anchored by lactase cheese ripening enzyme adoption

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue estimation from enzyme manufacturers, trade-flow analysis of dairy processing inputs, and top-down cross-validation against FAO dairy production statistics and Euromonitor consumption data. Historical figures (2021–2024) are based on audited company filings and customs data; the 2025 base year blends Q1–Q3 actuals with Q4 estimates; and the forecast period (2026–2035) applies scenario-weighted CAGR modeling.

.webp?v=1782888036)