Brewing Enzymes Market Summary

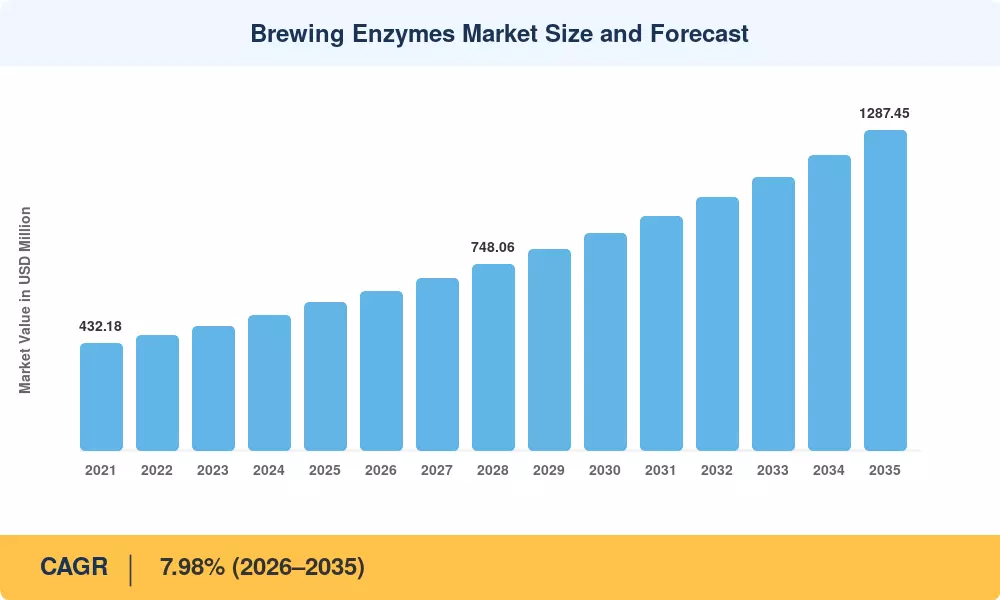

The Brewing Enzymes Market stood at an estimated USD 596.26 Million in 2025 and is projected to reach USD 641.53 Million in 2026 before climbing to USD 1,287.45 Million by 2035, registering a CAGR of 7.98% across the forecast window. This trajectory reflects a structural shift in the global beverage industry, where brewers increasingly rely on enzymatic solutions to control fermentation outcomes, cut water and energy usage, and meet tightening sustainability mandates. The European Commission's Farm to Fork Strategy, which targets a 50% reduction in chemical pesticide use by 2030, has indirectly accelerated the adoption of microbial-derived brewing enzymes as clean-label processing aids [1].

Legacy adjunct-dependent brewing processes are giving way to precision fermentation platforms that leverage tailored enzyme cocktails for amylase mashing, glucanase beer filtration, and protease wort clarity optimization. AB InBev's USD 30 Million investment in enzyme-driven water-reduction technology across 15 breweries signals the scale of capital flowing into brewing enzyme efficiency yield improvements [2]. Craft brewery enzyme application is equally reshaping the landscape, as independent operators seek consistent batch quality without the capital expense of traditional malt houses.

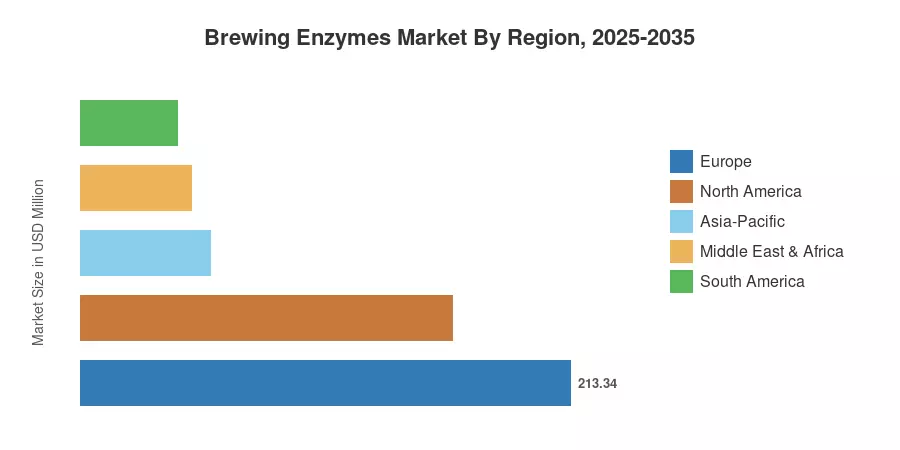

Europe captured roughly 35.78% of the Brewing Enzymes Market revenue in 2025, anchored by Germany's Reinheitsgebot-adjacent innovation corridors and Belgium's specialty ale tradition. Asia-Pacific is the fastest-growing region at a projected 9.48% CAGR through 2035, fueled by surging beer consumption across China, India, and Vietnam. North America, the second-largest region at approximately 27.14% share, benefits from the craft brewing revolution and expanding low-alcohol and gluten-free product lines The decade ahead will be defined by enzyme customization, sustainability-linked procurement, and digital fermentation monitoring.

Key Report Takeaways

• By Enzyme Type

- Amylase mashing accounted for approximately 40.12% of the Brewing Enzymes Market in 2025, driven by its essential role in starch-to-sugar conversion during the mashing stage

- Beta-glucanase is forecast to grow at an 8.55% CAGR through 2035, as glucanase beer filtration demands rise alongside the shift to barley-heavy grain bills

- Protease wort clarity applications are expanding among craft brewers seeking haze-free lagers without extended cold conditioning

• By Source

- Microbial enzymes commanded a dominant position in the Brewing Enzymes Market in 2025, with revenue exceeding USD 450 Million

- Plant-derived enzymes are growing at a 6.92% CAGR, supported by clean-label consumer preferences in organic brewing

• By Application

- Beer production represented the overwhelming majority of the Brewing Enzymes Market demand in 2025, underpinned by the global expansion of microbreweries and brewpubs

- Wineenzyme applications are projected to advance at a 9.42% CAGR as winemakers adopt pectinase and glucanase formulations for juice clarification

• By Region

- Europe held the largest regional share of the Brewing Enzymes Market, led by Germany, the UK, and France

- Asia-Pacific is the fastest-growing region, with craft brewery enzyme application gaining rapid traction in China and India

Market Size and Forecast (2021–2035)

The estimates below integrate primary interviews with enzyme manufacturers, brewery procurement officers, and trade association databases, triangulated against customs and production data. Historical figures (2021–2024) reflect actual market performance, while the base year (2025) uses a blend of trailing twelve-month shipment data and forward purchase orders.