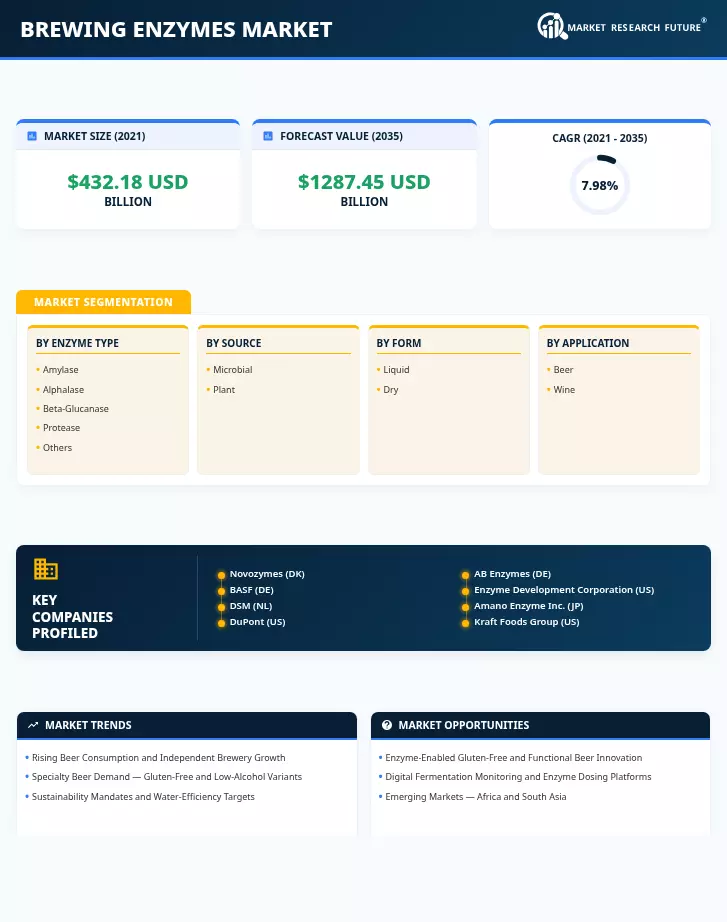

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Enzyme Type | Amylase, Alphalase, Beta-Glucanase, Protease, Others | Amylase | Beta-Glucanase |

| Source | Microbial, Plant | Microbial | Plant |

| Form | Liquid, Dry | Liquid | Dry |

| Application | Beer, Wine | Beer | Wine |

| Region | North America, Europe, Asia-Pacific, South America, Middle East & Africa | Europe | Asia-Pacific |

Market Segmentation Overview

By Enzyme Type

| Sub-Segment | Key Trend |

| Amylase | Thermostable alpha-amylase variants dominate; high-gravity brewing adoption rising |

| Alphalase | Industrial liquefaction applications expanding in adjunct-heavy brewing regions |

| Beta-Glucanase | Filtration efficiency gains driving adoption in craft and mid-size breweries |

| Protease | Gluten-reduction protocols and haze-free lager demand accelerating uptake |

| Others | Lipase, pullulanase, and specialty blends for flavor and foam modification |

Enzyme type segmentation reflects the functional specificity that brewers require at each stage of the production process. Amylase remains the volume leader because every brewery — regardless of size or style — depends on starch-to-sugar conversion, while beta-glucanase is the growth engine as filtration bottlenecks become the binding constraint in high-throughput brewing operations.

By Source

| Sub-Segment | Key Trend |

| Microbial | Engineered Aspergillus and Trichoderma strains delivering higher specific activity |

| Plant | Organic and clean-label positioning sustaining a niche but loyal customer base |

Microbial-source enzymes dominate because fermentation platforms scale economically and allow precise activity standardization. Plant enzymes retain relevance in heritage and organic brewing contexts where GMO-free sourcing is a regulatory or marketing requirement.

By Form

| Sub-Segment | Key Trend |

| Liquid | Preferred for automated dosing in large and mid-size brewhouses |

| Dry | Growing fastest due to shelf stability, reduced cold-chain costs, and emerging-market logistics advantages |

Form selection increasingly depends on brewery location and scale. Liquid enzymes suit automated, climate-controlled facilities, while dry formulations are gaining share in regions where cold-chain infrastructure is limited and storage conditions are variable.

By Application

| Sub-Segment | Key Trend |

| Beer | Core application spanning lager, ale, stout, and specialty styles globally |

| Wine | Pectinase and glucanase crossover from brewing driving rapid adoption in winemaking |

Beer remains the overwhelming application for brewing enzymes, but the wine segment is attracting cross-functional R&D investment as enzyme companies adapt existing filtration and clarification products for grape-must processing.

By Region

| Sub-Segment | Key Trend |

| North America | Craft brewery density and gluten-free innovation driving enzyme demand |

| Europe | Regulatory maturity and sustainability mandates sustaining the largest market |

| Asia-Pacific | Volume growth in China and India; fastest regional CAGR |

| South America | Adjunct-heavy brewing modernization led by Brazil's Ambev operations |

| Middle East & Africa | Non-alcoholic malt beverages and sorghum-based brewing creating new demand pockets |

Regional dynamics are shaped by the intersection of brewing tradition, regulatory environment, and consumer taste evolution. Europe's size advantage reflects decades of enzyme integration, while Asia-Pacific's growth rate mirrors the explosive expansion of per-capita beer consumption across developing economies.