Indian EV Market Summary

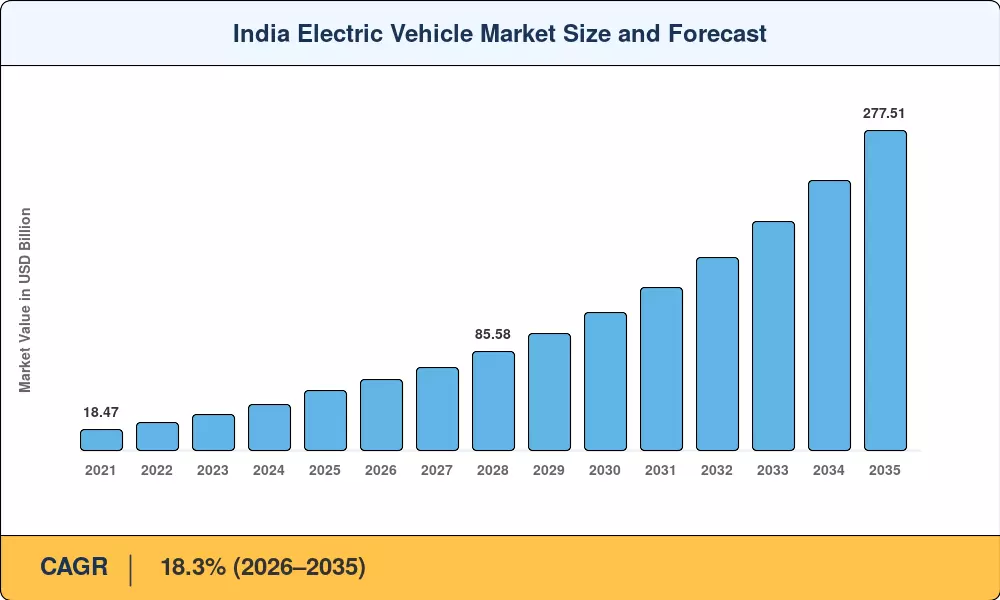

The India Electric Vehicle Market reached an estimated USD 51.69 billion in 2025, and the market is projected to grow from USD 61.15 billion in 2026 to USD 277.51 billion by 2035, registering a CAGR of 18.3% during 2026–2035. Two catalysts are reshaping this trajectory: the central government's commitment to 30% EV penetration in new vehicle sales by 2030 and cumulative Production-Linked Incentive (PLI) allocations exceeding INR 25,000 crore across advanced chemistry cells and automotive components [1][2]. These policy anchors have converted what was a subsidy-dependent niche into a structurally investable sector.

India's internal combustion engine (ICE) fleet — the third-largest globally — is being displaced by a generation of domestically designed battery-powered platforms. Tata Motors, Ola Electric, and Ather Energy have each committed over USD 1 billion in combined capital expenditure toward gigafactory-scale battery cell production, localized powertrain engineering, and software-defined vehicle architectures [3][4]. The India Electric Vehicle Market is benefiting from battery pack costs that dropped below USD 120 per kWh domestically in 2024, narrowing the total-cost-of-ownership gap with ICE equivalents to under 10% for urban commuters.

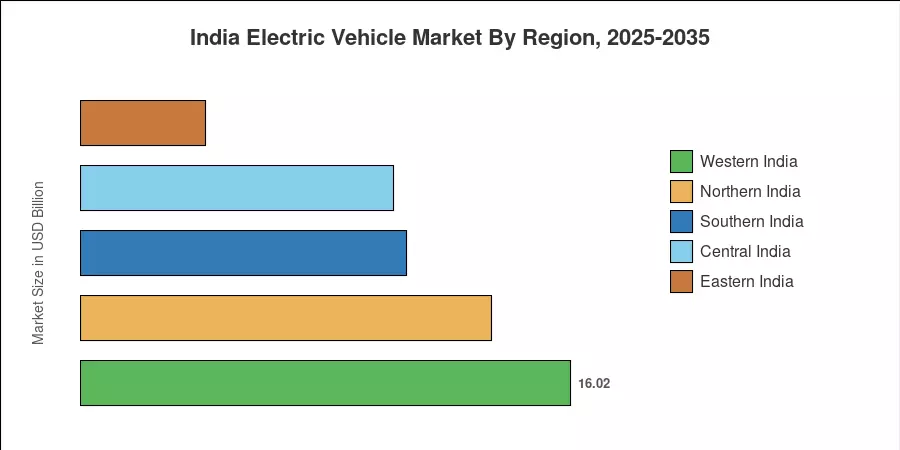

Western India — led by Maharashtra and Gujarat — commands approximately 31% of the India Electric Vehicle Market, driven by dense urban corridors and aggressive state-level incentive stacking. Southern India is the fastest-growing region at a projected CAGR of 20.6%, anchored by Karnataka's position as the country's largest EV charging hub and Tamil Nadu's manufacturing cluster. Northern India holds the second-largest share at roughly 26%, with Delhi recording among the highest EV penetration rates nationally. The India Electric Vehicle Market stands at an inflection point where demand pull has begun to outpace policy push.

Key Report Takeaways

• By Vehicle Type

- Two-wheelers account for approximately 57% of the India Electric Vehicle Market by unit volume, underpinned by affordability and urban last-mile convenience.

- Passenger cars represent the fastest-growing vehicle segment at a projected CAGR of 22.4% through 2035, driven by SUV-format launches in the INR 10–25 lakh price band.

- Commercial vehicles — including electric buses and cargo vans — are projected to reach USD 28.5 billion by 2035, fueled by fleet electrification mandates and total-cost-of-ownership advantages.

• By Propulsion Type

- Battery electric vehicles (BEVs) dominate approximately 89% of the India Electric Vehicle Market value, reflecting India's policy bias toward pure-electric drivetrains.

- Plug-in hybrid electric vehicles (PHEVs) are growing at a CAGR of 24.1%, attracting buyers in range-constrained intercity corridors.

• By Region

- Western India holds the largest regional share of the India Electric Vehicle Market, contributing an estimated USD 16.0 billion in 2025.

- Southern India is expected to grow at a CAGR of 20.6% through 2035, led by Karnataka's technology ecosystem and Tamil Nadu's PLI-backed manufacturing base.

- Northern India's India Electric Vehicle Market share stands at roughly 26%, with Delhi NCR acting as the policy laboratory for urban EV adoption.

Market Size and Forecast (2021–2035)

The India Electric Vehicle Market sizing draws on VAHAN registration data, SIAM wholesale figures, Ministry of Heavy Industries reports, IEA Global EV Outlook datasets, and proprietary primary interviews with OEM commercial leads, fleet operators, and battery technology engineers. Historical values (2021–2024) reflect audited industry actuals; the 2025 base year is triangulated from annualized Q1–Q3 run rates and dealer-channel intelligence. Forecast projections (2026–2035) incorporate scenario-weighted assumptions across policy continuity, battery cost trajectories, and charging infrastructure buildout.