India Rigid Plastic Packaging Market Summary

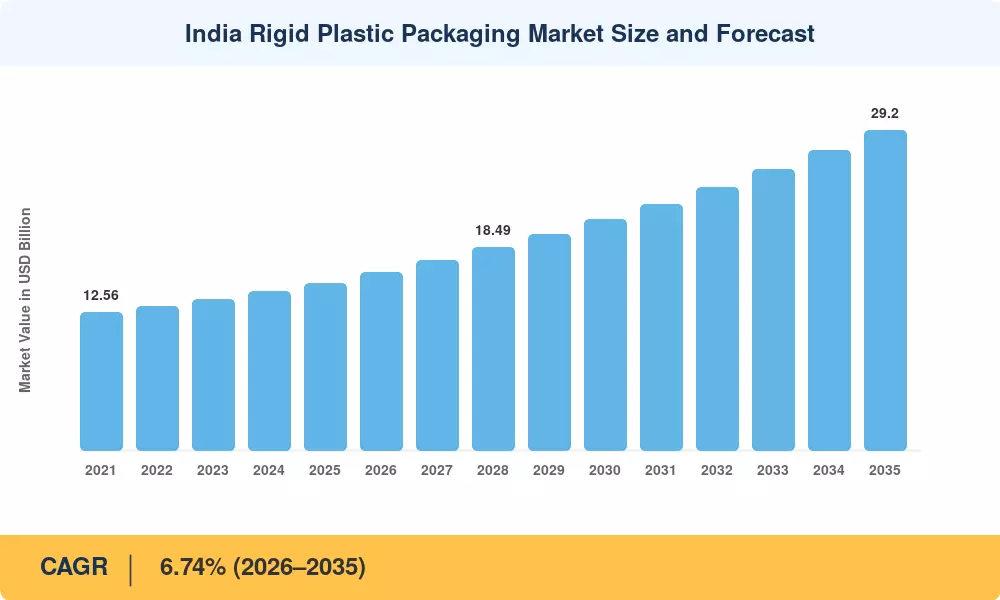

The India Rigid Plastic Packaging Market reached an estimated USD 15.28 Billion in 2025 and is projected to expand from USD 16.23 Billion in 2026 to USD 29.20 Billion by 2035, registering a CAGR of 6.74% during the forecast period. Growth hinges on two catalysts: India's National Dairy Plan Phase-II, which has driven a surge in processed dairy output requiring tamper-proof packaging, and the government's ethanol blending programme, which mandates dedicated HDPE and PP containers for fuel-grade ethanol logistics across the country [1][2]. These policy-backed demand pools give converters long-horizon order books that commodity-cycle volatility alone cannot derail.

The technology landscape within the India Rigid Plastic Packaging Market is shifting rapidly. Legacy single-layer extrusion lines are giving way to multi-layer co-extrusion and high-cavitation injection platforms that cut per-unit resin consumption by 12–18% while improving barrier performance [3]. Leading converters have collectively committed over USD 480 million in capex between 2023 and 2025 to upgrade blow-molding and thermoforming capacity, much of it targeting food-grade rPET processing where India's collection infrastructure now supports viable input supply [4].

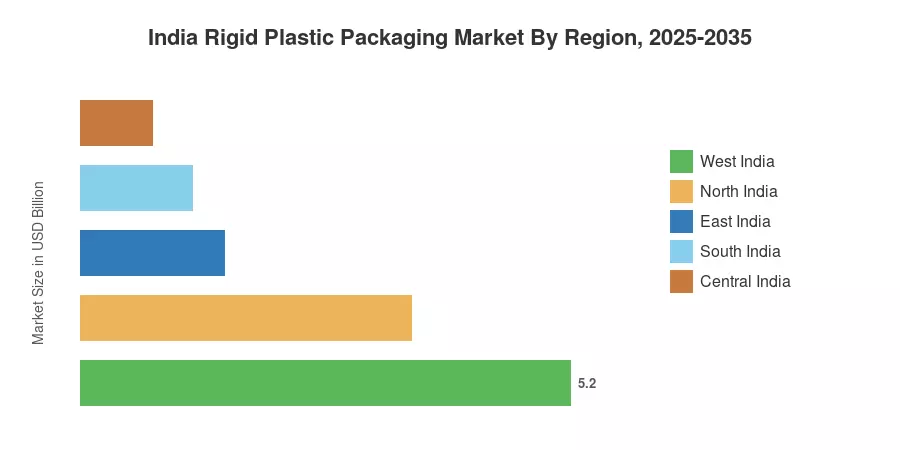

West India — anchored by Maharashtra and Gujarat — commands roughly 34% of total market value, driven by the country's densest concentration of food-processing clusters and pharmaceutical manufacturing hubs. South India is the fastest-growing region, expanding at an estimated 7.8% CAGR through 2035, buoyed by aggressive cold-chain investments in Tamil Nadu and Karnataka. North India, with roughly a 23% share, rounds out the top three, powered by dairy cooperatives in Haryana and the booming e-commerce fulfillment sector radiating from the Delhi NCR corridor. As urbanisation pushes India's packaged-food penetration toward 45% by the early 2030s, the India Rigid Plastic Packaging Market is poised for structural gains well beyond the current forecast window.

Key Report Takeaways

• By Resin Type

- Polyethylene Terephthalate (PET) held approximately 35.5% of the India Rigid Plastic Packaging Market in 2025, underpinned by carbonated-beverage and edible-oil bottle demand.

- Polypropylene (PP) is forecast to record the fastest CAGR of 8.05% through 2035, driven by microwavable food containers and pharmaceutical blister packs.

• By Product Type

- Bottles & Jars accounted for an estimated 37.8% share of the India Rigid Plastic Packaging Market in 2025, reflecting the dominance of single-serve beverage and personal-care formats.

- Trays & Containers are expected to grow at a 7.25% CAGR between 2026 and 2035, propelled by ready-to-eat meal kits and fresh-produce clamshell adoption.

• By End-Use Industry

- The Food segment retained approximately 27.0% share in 2025, led by snack pouches-to-rigid conversion trends and dairy cup demand.

- Pharmaceuticals are projected to expand fastest at an 8.77% CAGR, reflecting unit-dose blister packaging and cold-chain vial demand.

• By Production Process

- Extrusion dominated at an estimated 73.2% share in 2025, reflecting its cost advantage in high-volume sheet and container output.

- Injection Molding is forecast to register the highest growth at a 6.10% CAGR to 2035.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing framework combines bottom-up resin-consumption data with top-down trade-flow analysis, triangulated against converter capacity utilisation rates reported by the Indian Plastics Institute and the Ministry of Chemicals & Fertilizers [5]. Historical values (2021–2024) reflect published industry production statistics, while forecast values (2026–2035) apply demand-side econometric modelling calibrated to GDP growth, urbanisation rate, and FMCG penetration assumptions.