Industrial Fabrics Market Summary

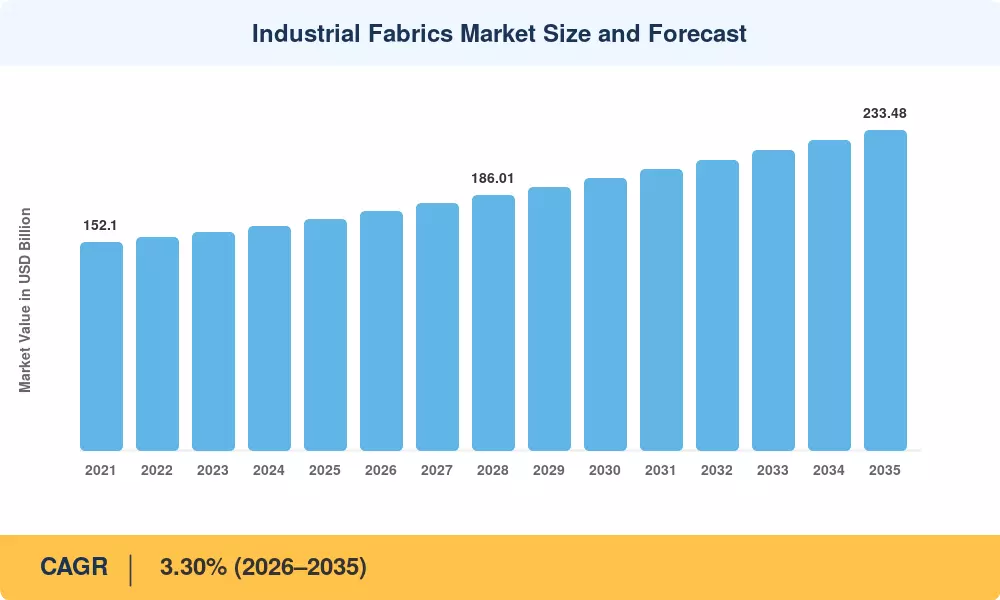

The Industrial Fabrics Market was valued at USD 168.75 billion in 2025 and is projected to reach USD 233.48 billion by 2035, registering a CAGR of 3.30% during the forecast period (2026–2035). Two converging forces are driving this expansion: a global infrastructure spending wave — anchored by the US Bipartisan Infrastructure Law's USD 1.2 trillion allocation and China's 15th Five-Year Plan capital commitments — and an accelerating transition toward high-specification fiber systems demanded by renewable energy, automotive lightweighting, and cleanroom manufacturing [9][16].

Although volume is still dominated by legacy commodity polyester, specialty fibers are the true margin story. Older materials are being replaced by aramid, carbon, and hybrid blends in ISO 8 gigafactory cleanrooms, 100-meter wind-blade spar caps, and crash-absorbing vehicle components. As a result of the industry's shift from tonnage to performance, capital investment in these advanced fiber lines exceeded USD 3.8 billion globally in 2024 [14][16].

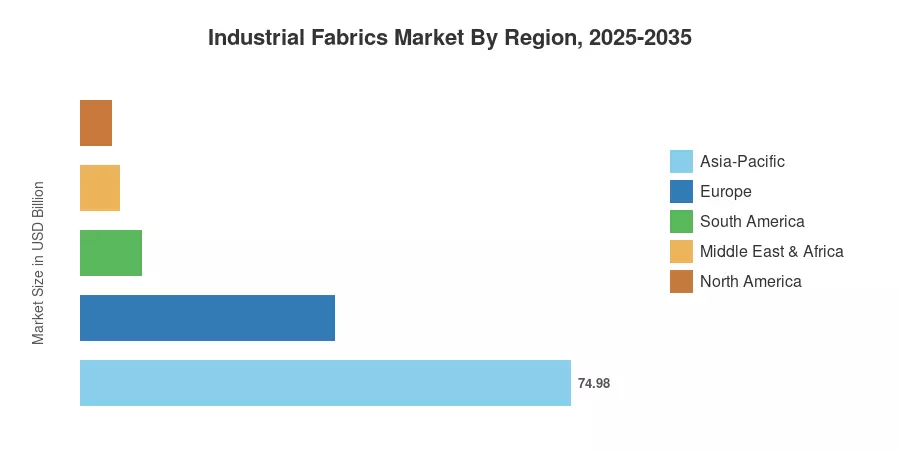

As the largest production base and the fastest-growing demand center through 2035, the Asia-Pacific region has 44.43% of the Industrial Fabrics Market. With a roughly 23% stake, Europe is in second place thanks to stringent worker safety regulations and wind energy fabric requirements. North America completes the top three thanks to gigafactory expansion and reshoring incentives. Over the next ten years, companies that can include recycled feedstock without compromising tensile performance will be rewarded as sustainability regulations become more stringent in every country.

Key Report Takeaways

• By Fiber Type

- Polyester accounted for 42.36% of the Industrial Fabrics Market in 2025, underpinned by its cost advantage and Asia-Pacific capacity dominance.

- Aramid fibers are projected to register a 6.36% CAGR through 2035, fueled by fire-protective and ballistic applications.

• By Fabric Construction

- Woven fabrics captured 48.91% of the Industrial Fabrics Market in 2025, maintaining leadership across conveyor, geotextile, and structural reinforcement end uses.

• By Application

- Conveyor belts held a 30.25% revenue share in 2025, reflecting record installation volumes in mining and automated logistics.

- Fire-protective apparel is forecast to grow at a 5.55% CAGR to 2035, driven by NFPA 2112 and EN ISO 11612 mandate adoption.

• By End-User

- Construction captured 27.49% of 2025 revenue in the Industrial Fabrics Market, supported by geotextile and roofing membrane demand.

• By Region

- Asia-Pacific held 44.43% of the global Industrial Fabrics Market revenue in 2025, reinforcing its polyester cost leadership.

- Europe represented the second-largest regional share at approximately 23%, anchored by automotive and wind energy fabric specifications.

Industrial Fabrics Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates bottom-up plant-capacity audits, top-down trade-flow analysis, and proprietary primary interviews with over 120 fabric converters, fiber producers, and industrial end users across 22 countries.