Instant Noodles Market Summary

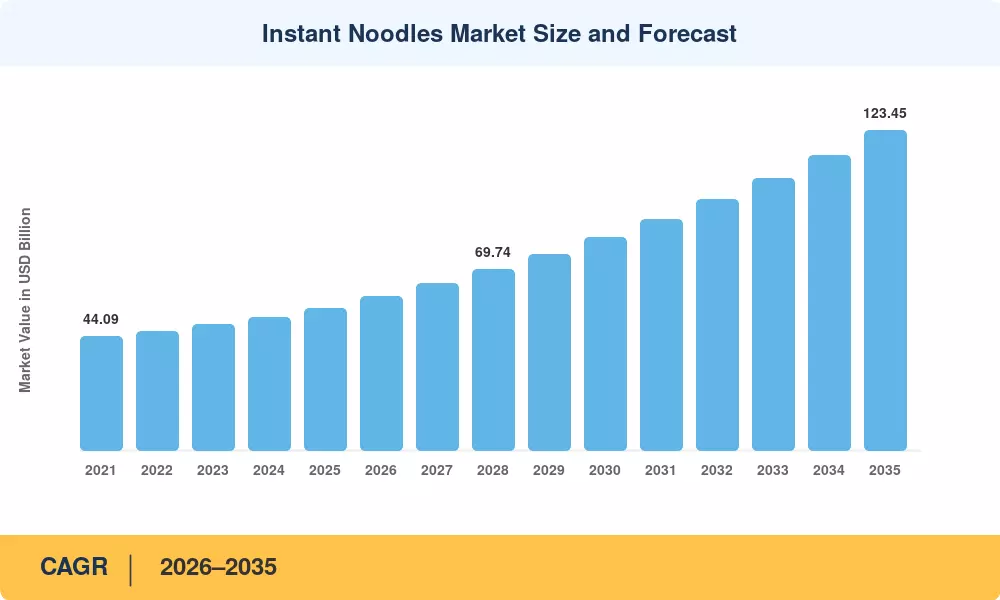

The Instant Noodles Market was valued at USD 54.60 billion in 2025 and is projected to reach USD 59.24 billion by 2026, climbing to USD 123.45 billion by 2035 at a CAGR of 8.50% during the forecast period. Urbanization rates exceeding 56% globally and rising dual-income household penetration have positioned convenience foods as a structural growth category rather than a cyclical one [1]. Government food-security programs across Southeast Asia and South Asia, which collectively allocated over USD 18 billion toward processed-food infrastructure between 2022 and 2025, continue to underpin supply-side expansion in the Instant Noodles Market [2].

The Instant Noodles Market is experiencing a transition in production technique from traditional deep-frying lines to air-drying and steam-flash methods, which can lower oil content by up to 40% and per-unit energy usage. From 2023 to 2025, major businesses are expected to invest USD 2.3 billion in retort packaging and smart-factory automation. This is part of a broader shift towards Industry 4.0 compliance in Asian and European production centers. The change also lends support to a clean-label stance, a priority for firms targeting health-conscious customers in North America and Western Europe.

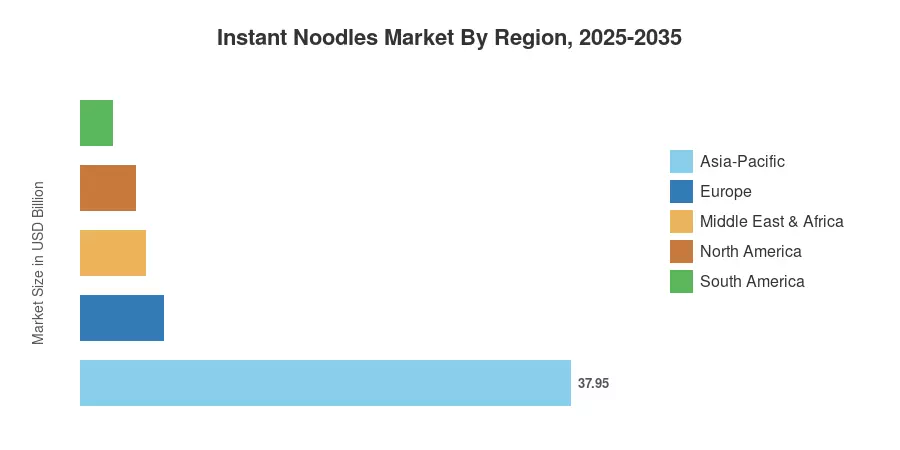

The Asia-Pacific region is the largest market for Instant Noodles, accounting for around 69.50% of the market by value, with per-capita consumption rates in China, Indonesia, and South Korea at 40 servings per year [4]—the fastest expanding region with an expected CAGR of 10.15% through 2035. Europe is the second-largest region, with around 11.8%, buoyed by premiumization trends in Germany, the UK and the Nordics. Emerging sectors of the Instant Noodles Market are on track for continuous double-digit expansion, powered by the momentum of plant-based diets and functional-food regulations building around the world.

Key Report Takeaways

• By Product Type

- Non-vegetarian variants captured 47.20% of the Instant Noodles Market share in 2025, driven by strong demand for chicken- and seafood-flavored SKUs across Southeast Asia.

- Vegetarian SKUs are forecast to register the fastest segment CAGR of 9.10% through 2035, propelled by plant-based dietary shifts in Europe and North America.

• By Packaging Type

- Packets accounted for USD 32.10 billion in Instant Noodles Market revenue during 2025, reflecting their dominant shelf presence in price-sensitive developing economies.

- Cup and bowl formats are on track to achieve a 9.90% CAGR to 2035, benefiting from on-the-go consumption and premium positioning.

• By Region

- Asia-Pacific contributed 69.50% of the Instant Noodles Market value in 2025, with China and Indonesia representing the two largest national markets.

- North America is expected to grow at a 7.85% CAGR through 2035, supported by expanding ethnic-food retail channels and e-commerce penetration.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework combines primary surveys of 120+ manufacturers and distributors with secondary validation from trade-association filings, customs data, and retail-audit panels. The table below presents the complete Instant Noodles Market trajectory from 2021 through 2035.

.webp?v=1784551653)