Internal Combustion Engine Market Summary

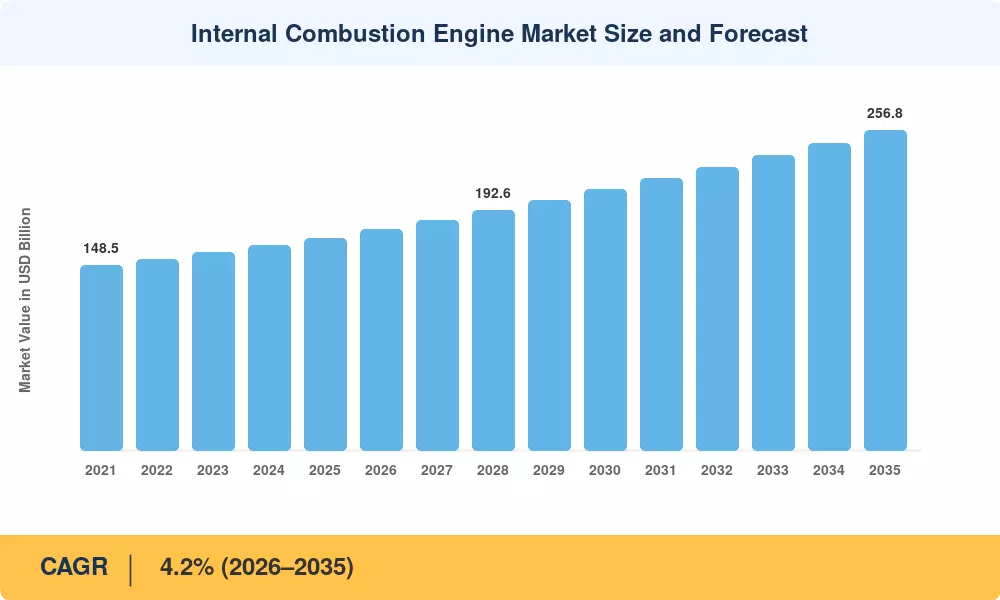

The Internal Combustion Engine Market was valued at USD 170.2 billion in 2025 and is projected to reach USD 177.3 billion in 2026 before climbing to USD 256.8 billion by 2035, expanding at a compound annual growth rate of 4.2% during the 2026–2035 forecast period. Two catalysts underpin this trajectory: the accelerating global demand for commercial freight transport, which the International Energy Agency estimates will grow cumulative diesel fuel demand by 18% through 2035 [1], and rising industrial backup power requirements across data-center-heavy economies. The Internal Combustion Engine Market retains its scale not because alternatives are absent but because the installed base, fuel infrastructure, and cost dynamics remain difficult to displace quickly.

A significant technology transformation is reshaping how combustion engines are designed, manufactured, and deployed. Legacy naturally aspirated configurations are giving way to advanced turbocharged, downsized architectures that extract more power per liter while cutting CO₂ output by 15–20%. Governments in the EU, China, and Japan have introduced progressively tighter emissions mandates — the European Commission's Euro 7 standard, effective 2025, alone forced OEMs to invest an estimated EUR 12 billion in powertrain redesign [2]. Hybrid integration is bridging the gap between pure combustion and full electrification across passenger and commercial segments.

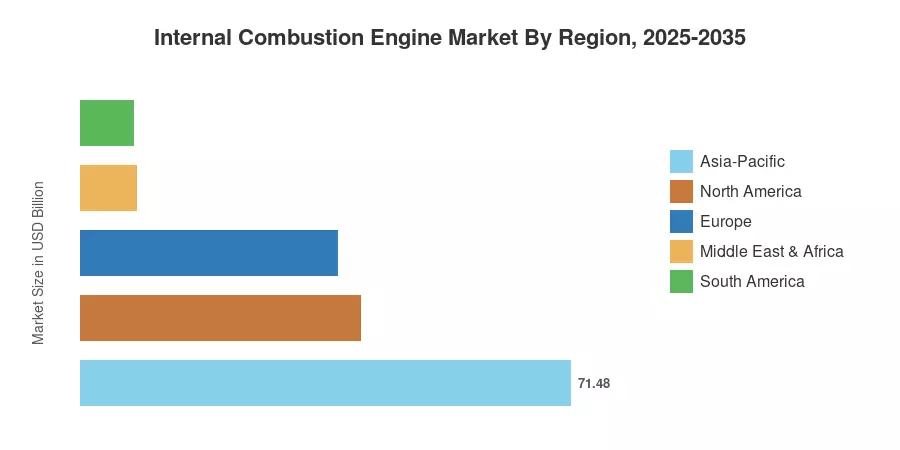

Asia-Pacific dominates the Internal Combustion Engine Market with roughly 42% of global revenue, driven by manufacturing scale in China, India, and Japan. The region also registers the fastest CAGR at 5.1% through 2035. North America holds approximately 24% share, anchored by heavy-duty trucking and oil-and-gas sector demand. Europe contributes around 22%, where stringent emissions rules paradoxically stimulate premium engine innovation. The decade ahead will hinge on how effectively OEMs balance regulatory compliance with profitability across these three regions.

Key Report Takeaways

• By Fuel Type

- Gasoline engines command the largest share of the Internal Combustion Engine Market at approximately 48% of 2025 revenue, supported by passenger vehicle volume in Asia-Pacific and North America.

- Diesel engines are projected to grow at a CAGR of 3.8% through 2035, sustained by heavy-duty trucking, marine propulsion, and off-highway equipment demand.

- Natural gas engines represent a USD 12.4 billion segment in 2025, benefiting from LNG-fueled power generation in the Middle East and Southeast Asia.

• By Application

- Automotive applications account for approximately 58% of the Internal Combustion Engine Market, with light commercial vehicles driving incremental growth in emerging economies.

- Industrial and power generation applications are expanding at a CAGR of 5.3%, the fastest among application segments, as data centers and mining operations scale backup capacity.

• By Region

- Asia-Pacific leads the Internal Combustion Engine Market with 42% revenue share, while North America contributes approximately USD 40.8 billion in 2025.

- The Middle East & Africa region posts the second-fastest regional CAGR at 4.8%, fueled by oil-and-gas infrastructure and distributed power generation.

Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining top-down industry revenue estimates, bottom-up OEM shipment data, and cross-validation against trade statistics from the United Nations Comtrade database and national automotive industry associations. Historical values (2021–2024) reflect audited annual reports and industry body filings; the 2025 base year integrates preliminary OEM guidance and production data through Q3 2025. Forecast values (2026–2035) apply segment-level regression models calibrated against macroeconomic indicators including industrial output, vehicle production forecasts from OICA, and energy demand projections from the IEA [3].