Isopropyl Alcohol Market Summary

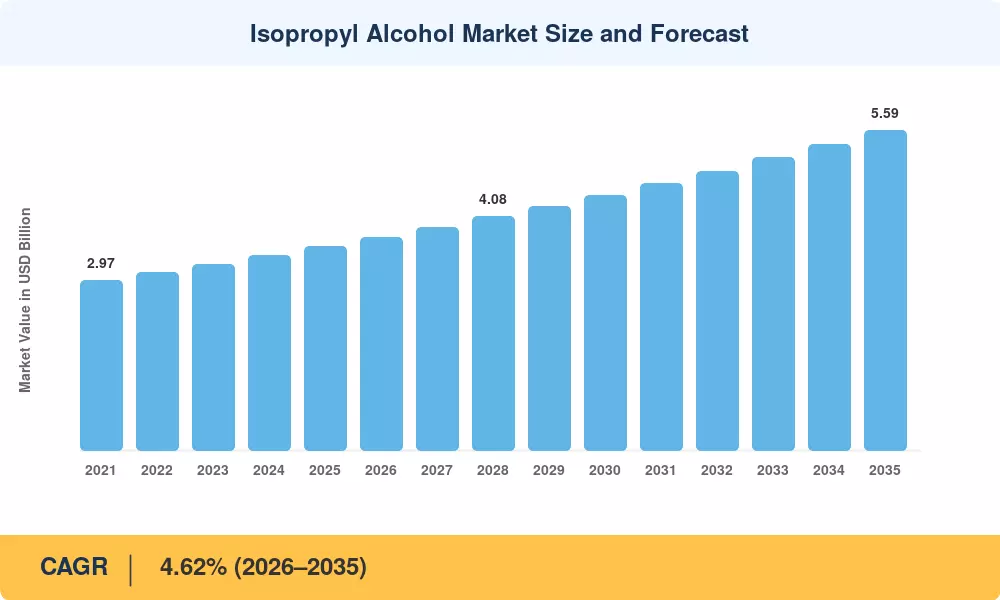

The Isopropyl Alcohol Market was valued at USD 3.56 Billion in 2025 and is projected to grow from USD 3.72 Billion in 2026 to USD 5.59 Billion by 2035, registering a CAGR of 4.62% during the forecast period (2026–2035). Propylene integration economics and rising demand for pharmaceutical alcohol across regulated formulations anchor this trajectory. The U.S. CHIPS and Science Act's semiconductor fab buildout — representing over USD 52 Billion in committed investments — directly amplifies consumption of ultra-high-purity industrial solvents required for wafer cleaning and lithographic processes [2].

A significant transformation is reshaping production methods across the Isopropyl Alcohol Market. Legacy acetone hydrogenation routes are steadily yielding ground to direct propylene hydration with advanced catalyst systems that deliver higher selectivity and lower energy consumption. The European Union's REPowerEU initiative, targeting 10 million metric tons of domestic green hydrogen by 2030, introduces a pathway for bio-based chemical processing solvents that could fundamentally alter feedstock economics for IPA producers [3].

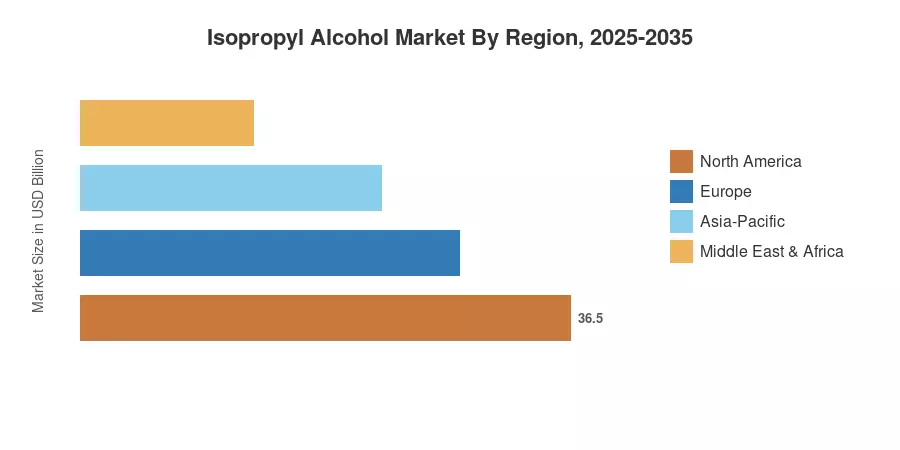

Asia-Pacific commands the dominant position in the Isopropyl Alcohol Market with a 45.2% revenue share in 2025, driven by semiconductor fabrication expansion in Taiwan and South Korea and robust healthcare disinfection demand across India and China. North America holds 24.8% of the total market value, supported by reshoring incentives and growing consumption of medical-grade alcohol. Europe — the second-largest region at 19.5% — benefits from tightening EU Biocidal Products Regulation standards that elevate demand for compliant disinfectant chemicals and antiseptic solutions

Key Report Takeaways

• By Application

- Process and Preparation Solvents accounted for 46.0% of the Isopropyl Alcohol Market share in 2025, reflecting the dominance of industrial cleaning alcohol in pharmaceutical and electronics manufacturing

- Cleaning and Drying Agents are expanding at the fastest pace, driven by surging demand for high-purity cleaning solvent chemicals in semiconductor fabrication

- Coating and Dye Solvents contributed USD 0.59 Billion in 2025 revenue, supported by reformulation trends in low-VOC industrial coatings

• By End-User Industry

- Healthcare captured 38.7% of the Isopropyl Alcohol Market size in 2025, underpinned by ongoing procurement of antiseptic solutions for hospital sterilization protocols

- Cosmetics and Personal Care is projected to post a 5.14% CAGR through 2035, driven by rubbing alcohol products in skincare formulations

• By Region

- Asia-Pacific held 45.2% of the Isopropyl Alcohol Market share in 2025 and is forecast to register the fastest CAGR of 5.62% through 2035

- North America accounted for USD 0.88 Billion in 2025, supported by pharmaceutical alcohol capacity additions in New Jersey and Texas

Market Size and Forecast (2021–2035)

MRFR employs a bottom-up estimation methodology triangulated with supply-side production data from major propylene hydration facilities, trade flow databases, and demand-side consumption across healthcare, electronics, and chemical intermediates end-users. All forecast projections are benchmarked against primary interviews with industry stakeholders and validated through secondary cross-referencing of published capacity announcements.