Jet Fuel Market Summary

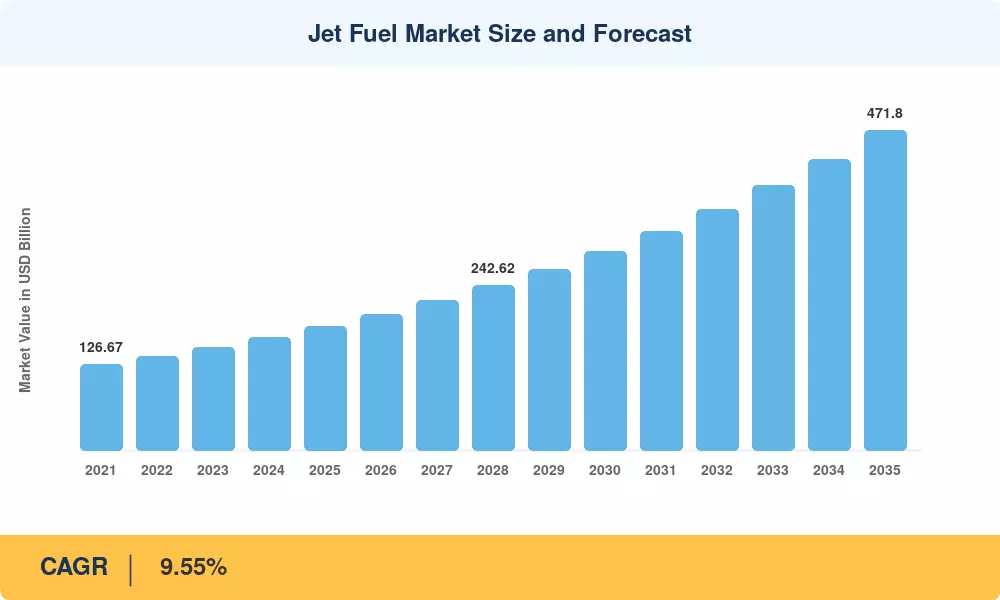

The Jet Fuel Market reached USD 182.45 billion in 2025 and is positioned to climb from a 2026 starting value near USD 200.18 billion toward USD 471.80 billion by 2035, advancing at a 9.55% CAGR across the forecast decade. Two catalysts anchor this trajectory: the European Union's ReFuelEU Aviation mandate, which legally requires escalating SAF blending jet fuel supply at member-state airports, and a wave of trans-Pacific wide-body deliveries that lift per-flight kerosene uplift. Record passenger load factors recorded in early 2025 pushed carriers to up-gauge fleets rather than trim schedules, sustaining demand growth in the Jet Fuel Market even as newer airframes burn less per seat.

Refiners across the value chain are reconfiguring product slates as conventional Jet A Jet A-1 kerosene aviation fuel coexists with certified renewable streams. Legacy straight-run kerosene production is increasingly supplemented by bio-jet fuel HEFA certification pathways and co-processed renewable feedstock, with global SAF investment commitments surpassing USD 36 billion in announced capacity through 2030. This transition reshapes procurement, since blended fuels carry slightly lower energy density and shift total liter demand upward.

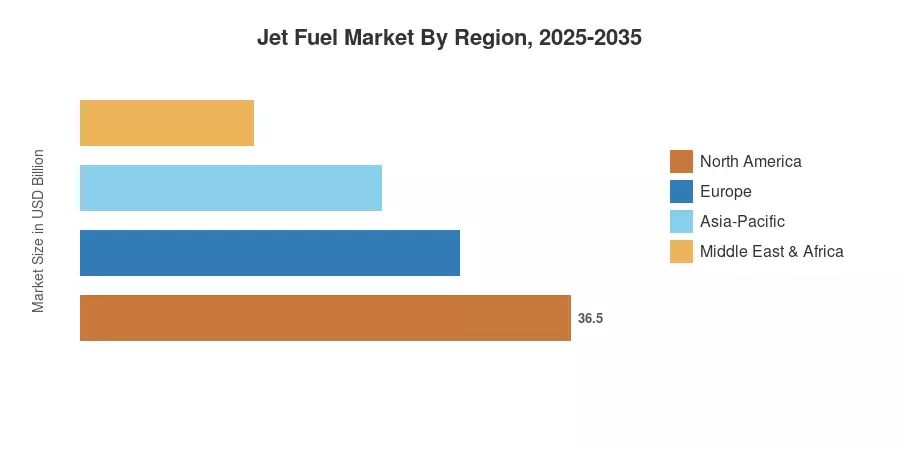

Asia-Pacific dominates the Jet Fuel Market with roughly 34.1% of global value in 2025, while the region simultaneously posts the fastest expansion at an 11.0% CAGR through the forecast window. North America stands as the second-largest contributor, supported by deep refining capacity and dense domestic networks. The next decade will reward integrated suppliers able to deliver both renewable and conventional barrels under unified airline contracts.

Key Report Takeaways

• By Technology (Fuel Type)

- Jet A-1 commanded a 66.4% share of the Jet Fuel Market in 2025, remaining the structural backbone of global aviation fuelling

- The "Others" category, led by SAF and bio-jet fuel HEFA certification streams, is forecast to expand at a 16.1% CAGR through 2035

- Jet B retains a narrow cold-climate niche valued near USD 6.20 billion in 2025

• By Sector (Application)

- Commercial aviation accounted for 72.9% of the Jet Fuel Market in 2025, the dominant demand engine

- Defense aviation is advancing at a 7.4% CAGR, supported by sustained military readiness budgets

- General aviation contributed roughly USD 14.80 billion in value during 2025

• By Region

- Asia-Pacific held a 34.1% share of the Jet Fuel Market in 2025

- Europe is expanding at a 9.9% CAGR, propelled by SAF blending jet fuel supply mandates

- North America generated about USD 52.30 billion in jet fuel value in 2025

Market Size and Forecast (2021–2035)

Market sizing blends refinery output data, airline fuel-uplift disclosures, and customs trade flows, triangulated against IEA aviation demand series and reconciled with Market Research Future (MRFR) 's proprietary estimation framework. Historical years reflect the pandemic trough and recovery; forecast years apply calibrated demand elasticity to traffic projections.

.webp?v=1783415610)