Knee replacement Market Summary

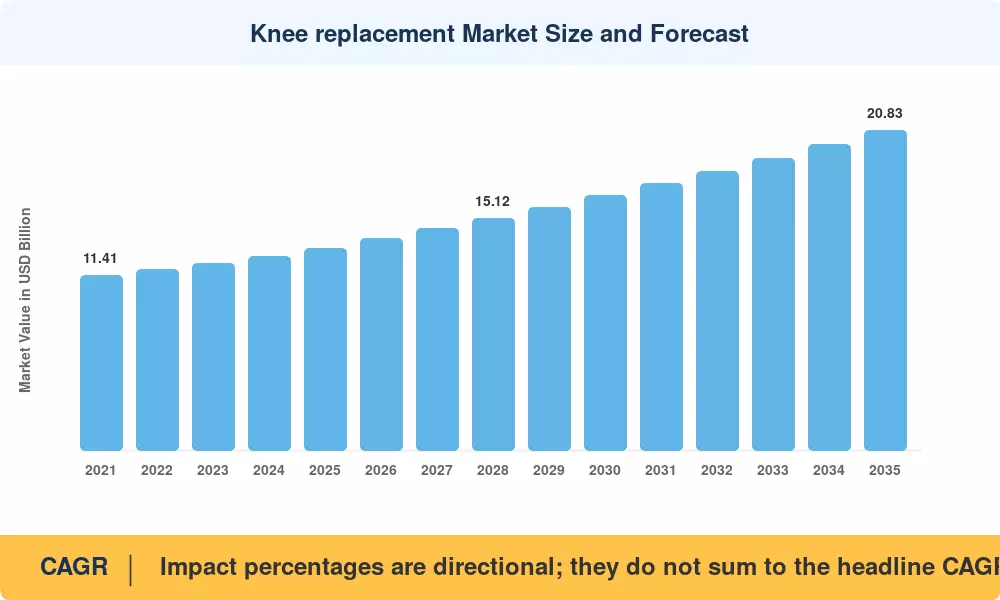

The Global Knee Replacement Market size was valued at USD 13.17 Billion in 2025, and the market is projected to grow from USD 13.79 Billion in 2026 to USD 20.83 Billion by 2035, registering a CAGR of 4.69% during the forecast period 2026–2035. This trajectory is propelled by two powerful forces: a global population aged 65 and older that the United Nations projects will surpass 1.6 billion by 2050 [1], and obesity rates that the WHO estimates now affect more than 890 million adults worldwide [2]. Governments from the US to Japan have responded by extending reimbursement coverage for outpatient joint procedures, making surgery accessible to a wider patient pool.

Technology is changing how surgeons do knee replacements. Robotic-assisted platforms are no longer the exclusive domain of top academic facilities. They are already being embraced by mid-tier hospitals and ambulatory surgical clinics seeking finer alignment tolerances and shorter recovery windows. Global capital expenditure on these systems approached USD 1.8 billion in 2024 [3]. OEMs are coupling hardware with AI-enabled preoperative planning software that maps patient-specific implant location. The biggest clinical change to the Knee Replacement Market in the past decade has been the move from entirely manual instruments to workflows supported by digital technology.

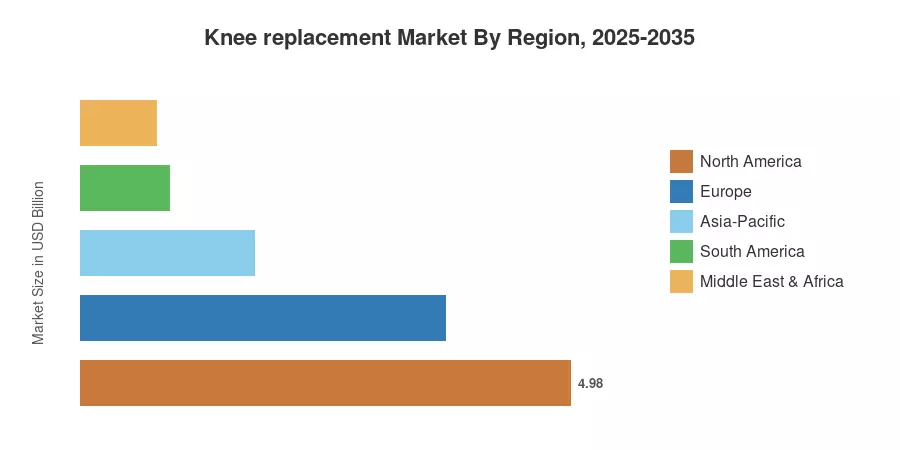

North America is the anchor, with the US Medicare population and strong private payer reimbursement arrangements, accounting for around 37.8% of global income. Asia-Pacific is the fastest-growing region at a CAGR of 13.45%. The growth in this region is driven by the rising healthcare insurance mandate in China and the Ayushman Bharat program by India, which now covers joint replacement treatments. Europe takes the second biggest proportion at around 28.2%, backed by aging demographics in Germany, France and the Nordic countries. The Knee Replacement Market is set to experience sustained, innovation-driven growth through 2035 with the increasing adoption of value-based care models in both developed and emerging economies.

Key Report Takeaways

• By Product

- Total knee replacement systems accounted for 65.5% of the Knee Replacement Market in 2025, reflecting sustained preference among surgeons for full condylar solutions.

- Partial knee replacement procedures are expanding at a 5.95% CAGR through 2035, benefiting from improved patient selection criteria and longer survivorship data.

- Patellofemoral replacement remains a niche segment, generating approximately USD 0.42 billion in 2025.

• By Surgical Technology

- Manual surgical techniques retained 48.0% revenue share in 2025, though their dominance is eroding as hospitals invest in guided platforms.

- Robotic-assisted procedures are the fastest-growing technology segment in the Knee Replacement Market, tracking an 11.85% CAGR.

• By End User

- Hospitals controlled 57.5% of end-user revenue in 2025, benefiting from complex revision case volumes.

- Ambulatory surgical centers are forecast to grow at a 9.25% CAGR, driven by same-day discharge protocols and bundled payment incentives.

• By Geography

- North America led the Knee Replacement Market with a 37.8% share, underpinned by Medicare reimbursement reforms.

- Asia-Pacific is projected to record a 13.45% CAGR, making it the fastest-growing geography through 2035.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s estimates blend bottom-up device-level revenue analysis with top-down macroeconomic and demographic modeling. Historical statistics (2021–2024) are derived from manufacturer filings, hospital procurement databases, and national joint registry publications. Forecast forecasts (2026-2035) incorporate implant adoption curves, reimbursement trajectory models and surgical volume growth rates across five geographical regions.