Laboratory Chemicals Market Summary

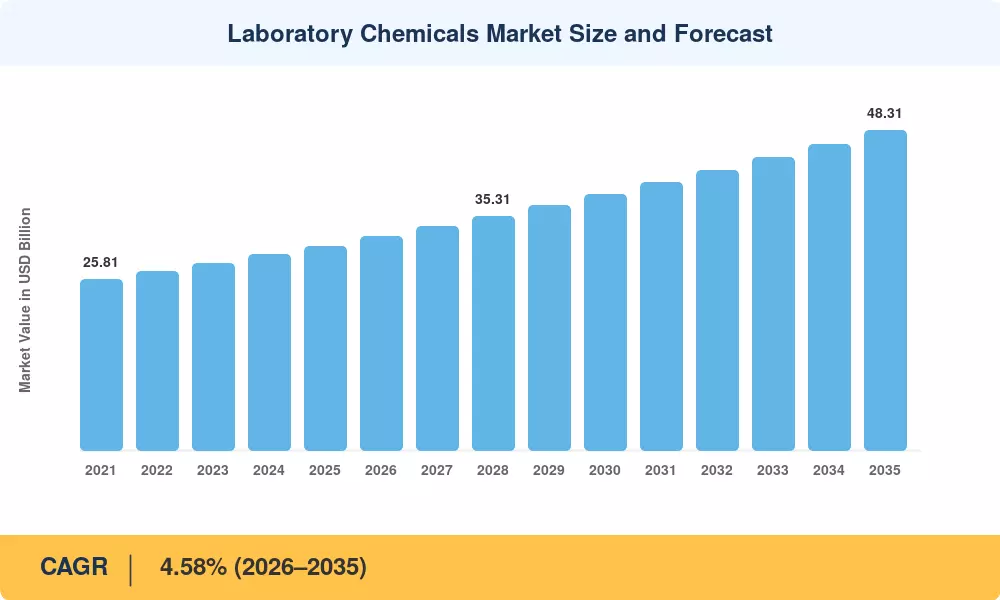

The Global Laboratory Chemicals Market size was valued at USD 30.87 Billion in 2025, and the market is projected to grow from USD 32.28 Billion in 2026 to USD 48.31 Billion by 2035, registering a CAGR of 4.58% during the forecast period 2026–2035. Life-science R&D spending continues to be the primary catalyst — global pharmaceutical companies alone directed more than USD 215 billion into research pipelines in 2024, sustaining demand for high-purity reagents, certified reference materials, and specialty solvents across clinical, academic, and industrial laboratories [1].

A broader transformation is reshaping laboratory procurement and workflows. Legacy manual dispensing and batch-quality testing are giving way to automated liquid-handling platforms and digitally tracked inventory systems. The European Union's revised REACH compliance framework and the U.S. EPA's updated Toxic Substances Control Act listings have compelled labs to transition toward certified, traceable chemistries — a shift that the International Council of Chemical Associations valued at USD 4.6 billion in incremental compliance spending through 2028 [2]. These regulatory mandates are raising the floor for product quality while simultaneously contracting the supplier base that can meet tighter specifications.

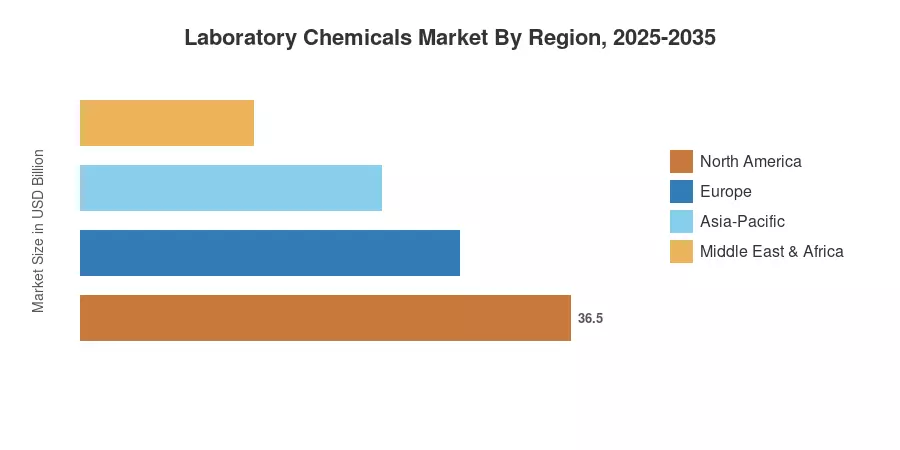

North America holds the largest share of the Laboratory Chemicals Market at approximately 31.9% of global revenue in 2025, anchored by the depth of the U.S. biotech and pharma cluster. Asia-Pacific is the fastest-growing region with a projected CAGR of 5.03%, driven by China's and India's expanding research infrastructure and government science funding programs. Europe remains the second-largest region, contributing roughly 27.5% of revenue, supported by Germany's chemical-industry ecosystem and the EU Horizon Europe research budget. The Laboratory Chemicals Market is poised for a decade of compounding growth as research complexity and regulatory rigor keep intensifying worldwide.

Key Report Takeaways

• By Type

- Biochemistry chemicals accounted for 29.3% of the Laboratory Chemicals Market in 2025, reflecting persistent demand from drug-discovery and proteomics research workflows.

- Healthcare/pharmaceutical reagents are expanding at the fastest pace, with a projected CAGR of 5.35% through 2035, fueled by precision-medicine diagnostics and biomarker validation programs.

- Molecular biology reagents held a 2025 valuation of approximately USD 5.87 billion, supported by genomics and next-generation sequencing adoption.

• By Application

- Academia and educational institutions represented 33.1% of the Laboratory Chemicals Market in 2025, the largest application segment globally.

- The healthcare/pharmaceutical application segment is forecast to record a 5.0% CAGR through 2035, the highest among all application categories.

- Industrial laboratories contributed an estimated USD 6.79 billion in 2025 revenue, driven by quality-control testing in food, petrochemicals, and materials science.

• By Region

- North America led the Laboratory Chemicals Market with 31.9% of global revenue in 2025.

- Asia-Pacific is projected to be the fastest-growing region at a 5.03% CAGR through 2035.

- Europe generated approximately USD 8.49 billion in 2025, ranking as the second-largest regional contributor.

Laboratory Chemicals Market Size and Forecast (2021–2035)

Market sizing draws on bottom-up demand modeling across six chemical type segments, four application verticals, and five geographic regions. Historical estimates (2021–2024) are calibrated against trade-flow data, company filings, and government science-funding disclosures, while the forecast (2026–2035) applies segment-level growth assumptions validated through primary interviews with procurement officers and R&D directors at 120+ laboratories globally.