Leather Goods Market Summary

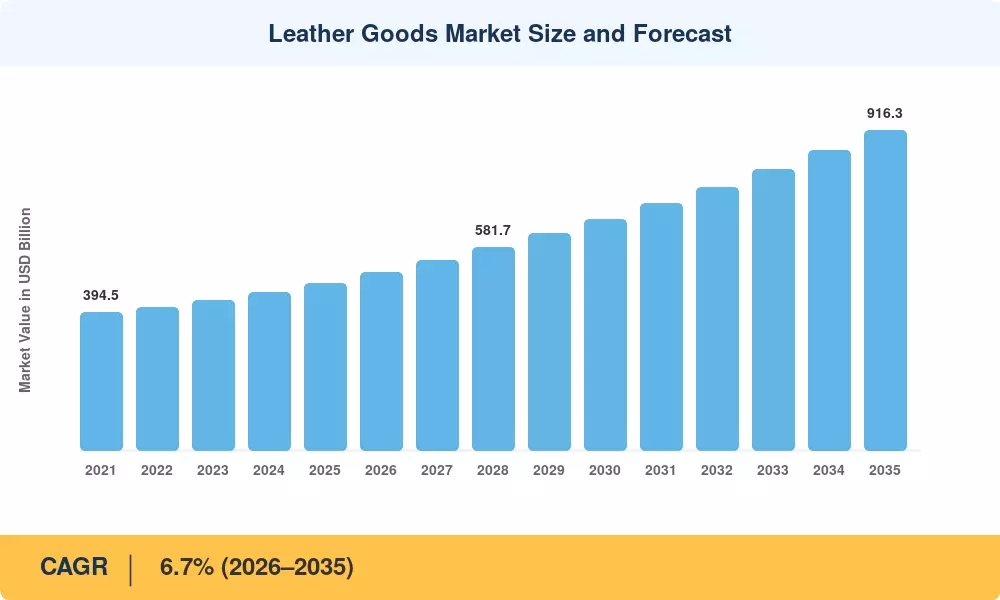

The global Leather Goods Market was valued at USD 478.8 billion in 2025 and is projected to reach USD 510.9 billion by 2026, growing to USD 916.3 billion by 2035 at a CAGR of 6.7% during the 2026–2035 forecast period. Rising disposable incomes across emerging economies, coupled with a cultural shift toward premium lifestyle products, underpin this expansion. Government-backed programs promoting domestic manufacturing — such as India's Production-Linked Incentive scheme allocating over USD 500 million toward leather sector modernization — have injected fresh momentum into the Leather Goods Market supply chain [1].

A manufacturing transformation is reshaping how the Leather Goods Market operates at scale. Traditional manual tanning and stitching workflows are giving way to laser cutting, automated quality inspection, and water-recycling tannery systems. The European Commission's Circular Economy Action Plan has accelerated investment in bio-based tanning agents, with the continent's top five tanneries collectively committing EUR 320 million toward chemical-free processing by 2028 [2]. These shifts are compressing production lead times by 15–20% while reducing water consumption per hide by nearly 40% [3].

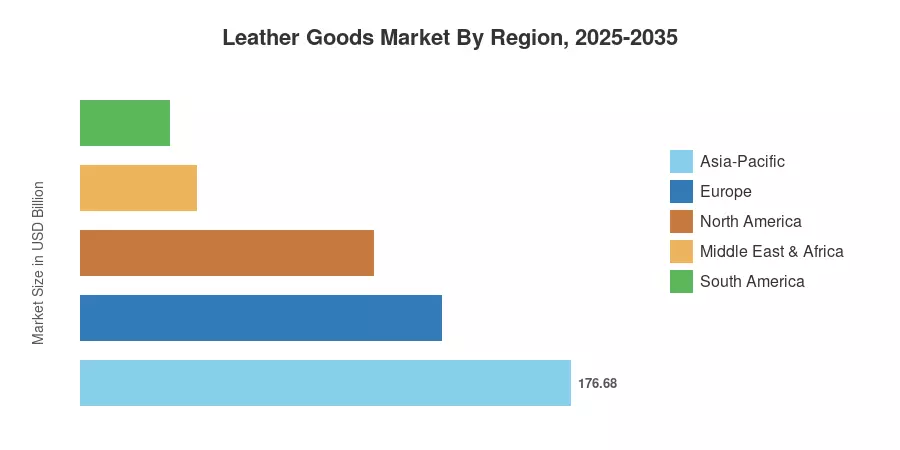

Asia-Pacific commands 36.9% of the global Leather Goods Market revenue, driven by China's export dominance and India's growing domestic consumption. The Middle East & Africa region is the fastest-growing, with a projected CAGR of 8.7%, fueled by luxury retail expansion in the UAE and Saudi Arabia's Vision 2030 spending. Europe holds the second-largest share at 27.2%, anchored by Italian and French heritage brands. As sustainability regulations tighten and consumer expectations evolve, the Leather Goods Market is poised for structural reinvention over the coming decade.

Key Report Takeaways

• By Product Type

- Footwear accounted for 36.1% of Leather Goods Market revenue in 2025, reflecting its status as the highest-volume product category globally.

- Accessories are forecast to expand at a 7.6% CAGR through 2035, outpacing all other product segments as demand for small leather goods intensifies.

• By End User & Category

- Male consumers held a 48.4% share of the Leather Goods Market in 2025, though the female segment is advancing at a faster 7.15% CAGR.

- Mass products represented 58.5% of total sales, yet the premium tier is climbing at a 7.85% CAGR between 2026 and 2035.

• By Region

- Asia-Pacific dominated the Leather Goods Market with 36.9% of global revenue in 2025.

- The Middle East & Africa region is projected to record the highest regional CAGR at 8.7% over the forecast period.

Leather Goods Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up revenue modeling from trade databases, customs records, company financials, and proprietary primary research across 42 countries. Historical figures (2021–2024) are reconciled against industry association data, while the forecast (2026–2035) applies regression-adjusted demand modeling calibrated to macroeconomic indicators including GDP per capita growth and urbanization rates.

.webp?v=1783951685)