Lithium-ion Battery Recycling Market Summary

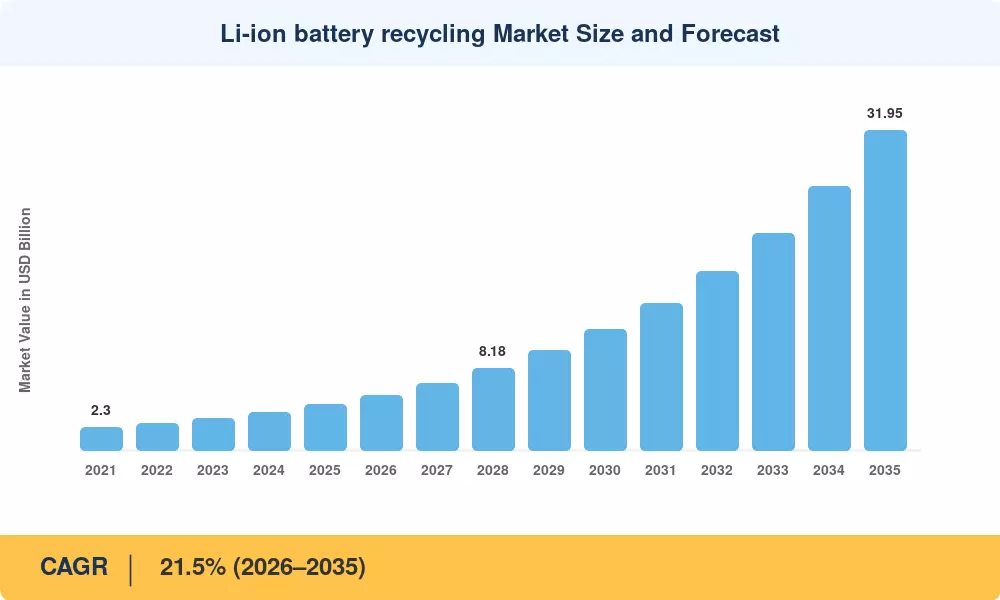

The Lithium-Ion Battery Recycling Market was valued at USD 4.56 Billion in 2025 and is projected to grow from USD 5.54 Billion in 2026 to USD 31.95 Billion by 2035, registering a CAGR of 21.5% during the forecast period (2026–2035). Two catalysts stand behind this trajectory: the European Union's Battery Regulation, which mandates minimum recycled-content thresholds for cobalt, lithium, and nickel starting in 2031, and the U.S. Inflation Reduction Act, whose domestic-content requirements for EV tax credits channel capital toward onshore recycling capacity [1][2]. Together, these policies transform end-of-life battery processing from a voluntary sustainability exercise into a compliance-driven cost line.

The technology landscape is shifting away from energy-intensive pyrometallurgical smelting toward hydrometallurgical and direct recycling routes that recover more lithium at lower operating temperatures. BloombergNEF estimates that global investment in battery recycling capacity topped USD 8 billion between 2022 and 2024, with at least 35 commercial-scale facilities either commissioned or under construction across three continents [3]. This investment wave is creating a two-tier market: vertically integrated recyclers that feed recovered cathode precursors directly back into cell production, and independent processors that sell intermediate black mass into spot commodity channels.

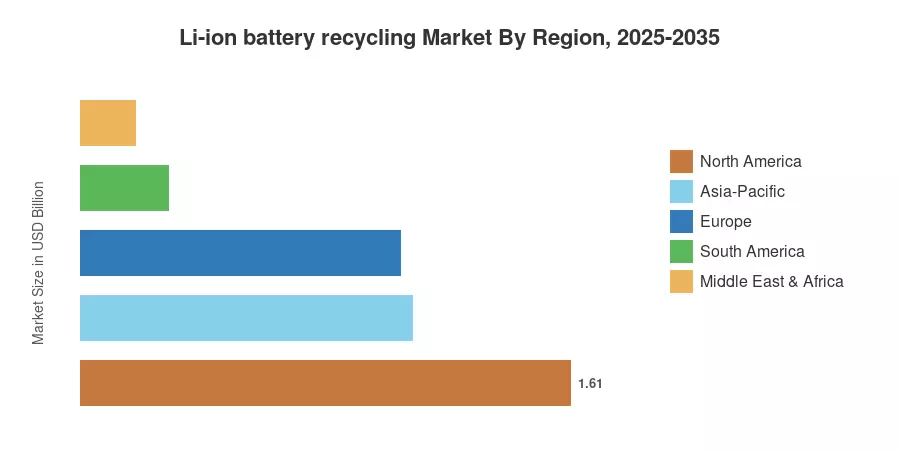

North America currently leads the lithium-ion battery recycling market with an estimated 35.4% share of global revenue, driven by IRA-linked tax incentives and Department of Energy loan guarantees exceeding USD 2 billion [4]. Asia-Pacific is the fastest-growing region, expanding at a 23.8% CAGR as Chinese and South Korean cell makers internalize recycling within their gigafactory complexes. Europe holds the second-largest share at roughly 23% of the market, underpinned by the EU Battery Regulation's producer-responsibility mandates [5]. As first-generation EV batteries reach end of life in volume from 2028 onward, throughput constraints — not demand — will likely become the binding variable for growth.

Key Report Takeaways — Lithium-ion Battery Recycling Market

By Recycling Technology

- Hydrometallurgical processes accounted for 58.4% of the Lithium-ion battery recycling market in 2025, reflecting their superior lithium recovery rates compared with thermal alternatives.

- Direct and mechanical recycling methods are forecast to post a 30.7% CAGR through 2035, attracting investment from automakers seeking shorter closed-loop turnaround times.

By End-of-Life Source

- Automotive batteries held a 68.1% share of the Lithium-ion Battery Recycling Market in 2025, as first-wave EV packs entered retirement in China and Europe.

- Consumer electronics batteries contributed USD 0.48 Billion in 2025 revenue, with growth moderating as device lifespans extend.

By Region

- North America led the Lithium-ion Battery Recycling Market with a 35.4% revenue share in 2025, anchored by policy-driven capacity buildouts.

- Asia-Pacific is projected to expand at a 23.8% CAGR through 2035, the fastest of any region.

Lithium-Ion Battery Recycling Market Size and Forecast (2021–2035)

Data for historical years (2021–2024) derive from company disclosures, trade-association tonnage reports, and secondary literature cross-referenced with customs data on black-mass shipments. Forecast projections (2026–2035) apply a bottom-up model aggregating installed processing capacity by region and chemistry, calibrated against announced capital expenditure pipelines and regulatory timelines.