Life Science Analytics Market Summary

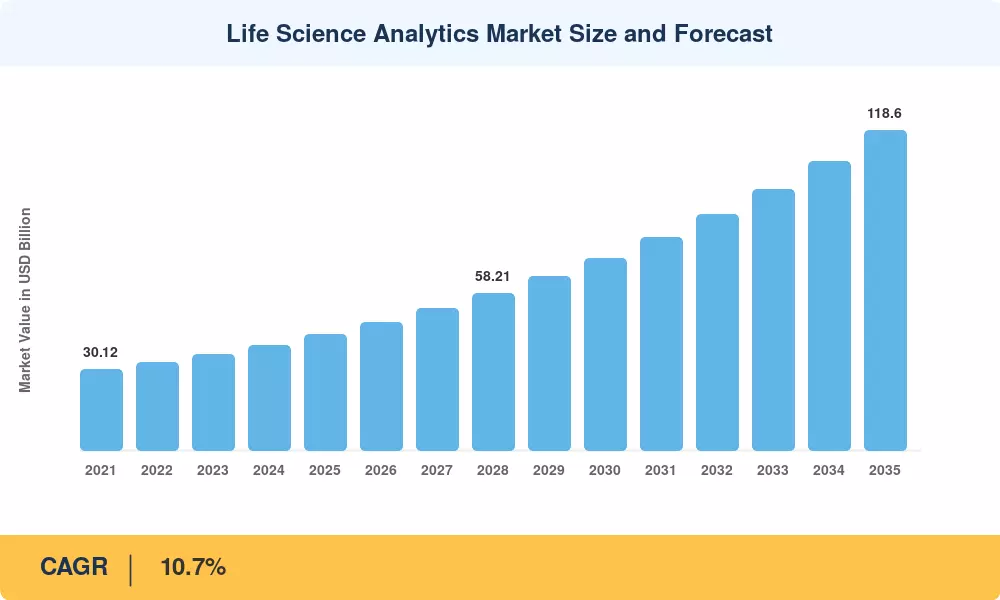

The Life Science Analytics Market size was valued at USD 42.90 Billion in 2025, and the market is projected to grow from USD 47.50 Billion in 2026 to USD 118.60 Billion by 2035, registering a CAGR of 10.7% during the forecast period 2026–2035. Two catalysts anchor this trajectory: the U.S. Food and Drug Administration's January 2024 real-world-evidence guidance, which formally endorses analytics integration across every development stage [1], and the European Medicines Agency's 2024 adaptive-trial framework promoting digital-twin simulations for dose optimization [2]. Together, these regulatory endorsements are converting analytics from an operational add-on into a compliance imperative.

A sweeping technology shift is redefining how sponsors generate evidence. Legacy retrospective reporting systems — static dashboards that summarize past performance — are giving way to predictive and prescriptive engines that anticipate adverse events, optimize patient stratification, and accelerate time-to-market. Biopharma R&D spending exceeded USD 260 Billion globally in 2024 [3], and an increasing share of that budget now flows toward advanced analytics platforms that deliver real-time insights rather than quarterly summaries. Payer pressure for value-based reimbursement has further accelerated spending on health-economics evidence generation and multichannel commercial intelligence.

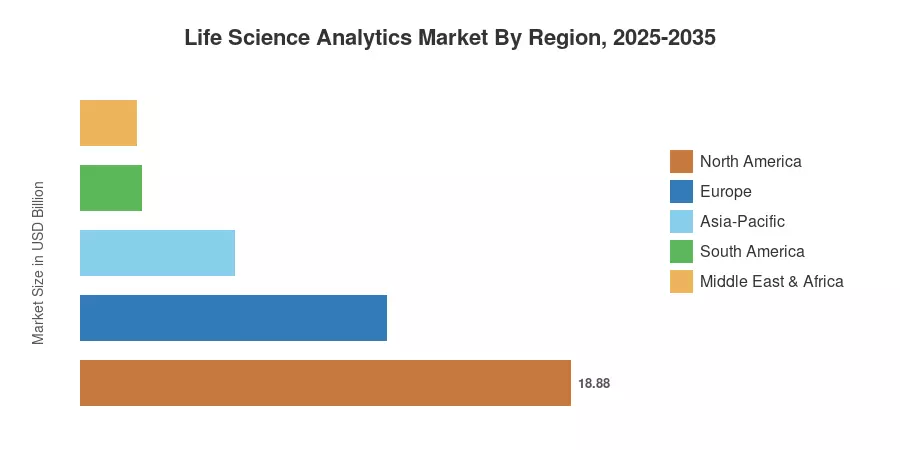

North America commands a 44.0% share of the Life Science Analytics Market, driven by concentration of top-20 pharmaceutical headquarters and robust FDA digital-health funding. Asia-Pacific is the fastest-growing region at a 13.8% CAGR through 2035, propelled by clinical-trial migration and government digitization programs in China and India. Europe holds the second-largest share at 27.5%, underpinned by the EMA's progressive data-sharing mandates. The decade ahead will hinge on how quickly sponsors operationalize generative AI within validated analytical workflows.

Key Report Takeaways

• By Product Type

- Descriptive analytics held a 48.0% revenue share of the Life Science Analytics Market in 2025, reflecting its foundational role in regulatory submissions and safety reporting.

- Prescriptive analytics is projected to expand at a 14.8% CAGR through 2035, as sponsors invest in automated decision-support engines.

• By Component

- Services accounted for 59.0% of the Life Science Analytics Market in 2025, encompassing managed analytics, consulting, and integration.

• By Deployment

- Cloud-based deployment models are advancing at a 14.9% CAGR, overtaking on-premise installations that represented a 69.0% share in 2025.

• By Application

- Research and development captured a 44.5% share in 2025, the largest application segment.

• By End User

- Medical device companies recorded the highest end-user CAGR at 15.8% through 2035.

• By Region

- North America represented 44.0% of the Life Science Analytics Market in 2025.

- Asia-Pacific is the fastest-expanding region at 13.8% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from audited company revenues, government health-IT expenditure databases, and proprietary demand-side surveys covering over 350 life-science organizations globally. Forecast projections apply a bottom-up approach calibrated against macroeconomic indicators, regulatory timelines, and technology adoption curves.