Precision Medicine Market Summary

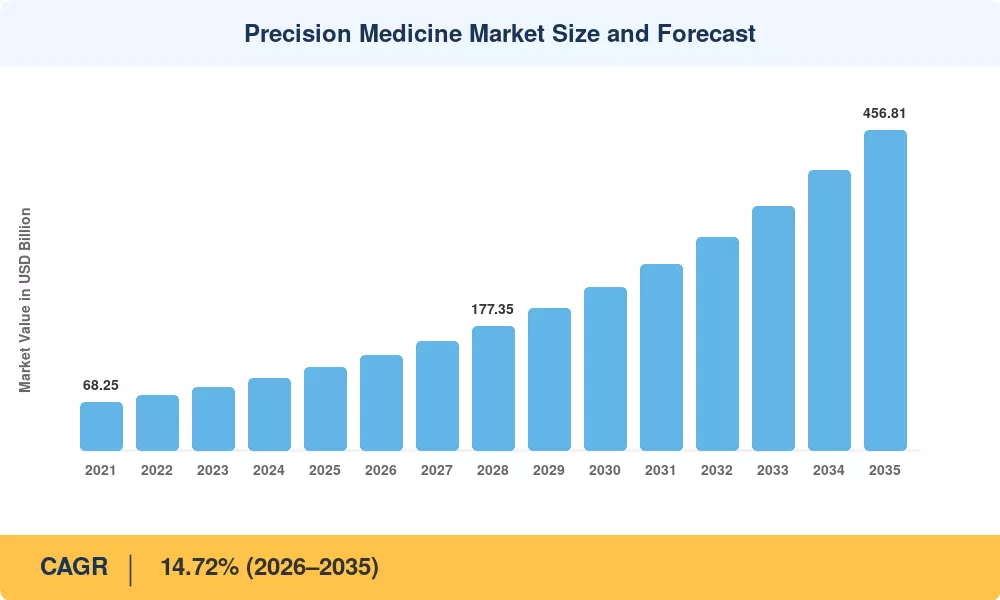

The Precision Medicine Market reached an estimated USD 118.23 billion in 2025, positioning the sector for aggressive expansion from USD 134.10 billion in 2026 to USD 456.81 billion by 2035 at a CAGR of 14.72% during 2026–2035. This trajectory is anchored in a wave of national genomics programs — the U.S. All of Us Research Initiative alone has enrolled over 800,000 participants, generating the population-scale datasets that underpin pharmacogenomics drug matching and biomarker-driven therapy development[2]. Regulatory agencies in both the U.S. and EU have introduced accelerated review pathways for companion diagnostics, compressing approval timelines by as much as 40% since 2021.

A fundamental technology shift is reshaping how therapies are designed and delivered. Legacy one-size-fits-all drug development, which historically required USD 2.6 billion per approved molecule, is giving way to targeted molecular therapy pipelines that leverage next-generation sequencing, AI-powered clinical-trial matching, and real-world evidence analytics [3]. The U.S. Inflation Reduction Act and the EU Pharmaceutical Strategy have together earmarked over USD 12 billion in incentives for personalized treatment plans and individualized cancer treatment research through 2030, accelerating platform adoption across biopharma.

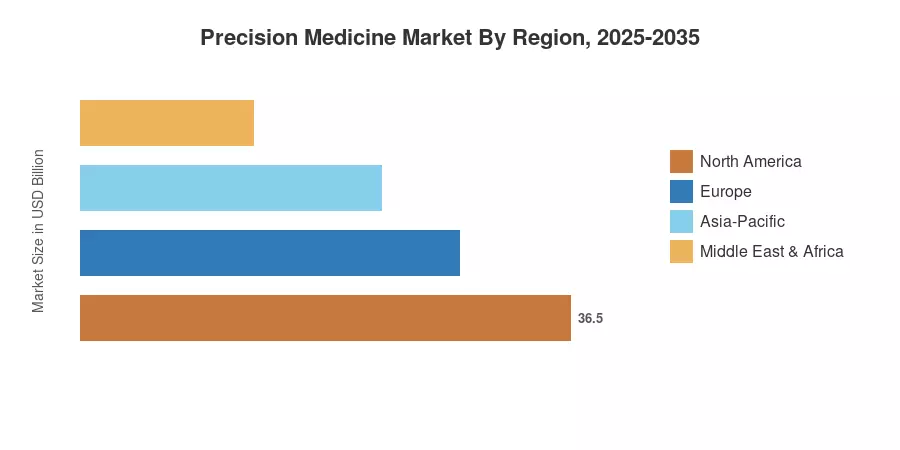

North America commands approximately 45% of the Precision Medicine Market, driven by deep payer integration and mature biobank infrastructure. Asia-Pacific is the fastest-growing region at a projected CAGR exceeding 15.8% through 2035, propelled by China's national genomics initiative and India's expanding clinical-trial ecosystem. Europe holds the second-largest share at roughly 26%, supported by cross-border data-sharing frameworks under the European Health Data Space. As computational biology and decentralized trial designs converge, the Precision Medicine Market is entering a phase of structural acceleration that will redefine healthcare economics through 2035.

Key Report Takeaways

• By Technology

- Next-generation sequencing captured approximately 38% of the Precision Medicine Market in 2025, reflecting widespread clinical adoption for biomarker-driven therapy identification

- AI and machine-learning diagnostic platforms are expanding at a 19.3% CAGR through 2035, making them the fastest-growing technology segment in the Precision Medicine Market

- Bioinformatics and big data analytics together accounted for USD 28.4 billion in 2025 revenue, underscoring the shift toward computational drug discovery

• By Application

- Oncology led all applications with 43.5% of Precision Medicine Market revenue in 2025, driven by expanding panels for individualized cancer treatment

- Rare and genetic disorders are forecast to grow at a 17.1% CAGR to 2035, reflecting orphan drug incentives and improved genomic screening

• By Region

- North America accounted for 45% of the global Precision Medicine Market spending in 2025

- Asia-Pacific is projected to grow at a 15.8% CAGR between 2026 and 2035, the fastest of any region

- Europe held approximately USD 30.7 billion in revenue in 2025, anchored by the UK Biobank and Nordic health registries

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue estimates from 120+ precision medicine companies, cross-validated against top-down expenditure data from WHO, CMS, and national health ministry budgets. Historical figures reflect audited company filings and published reimbursement data, while forecast values apply a calibrated compound growth model adjusted for regulatory pipeline velocity and payer adoption curves[4].