Life Science Tools Market Summary

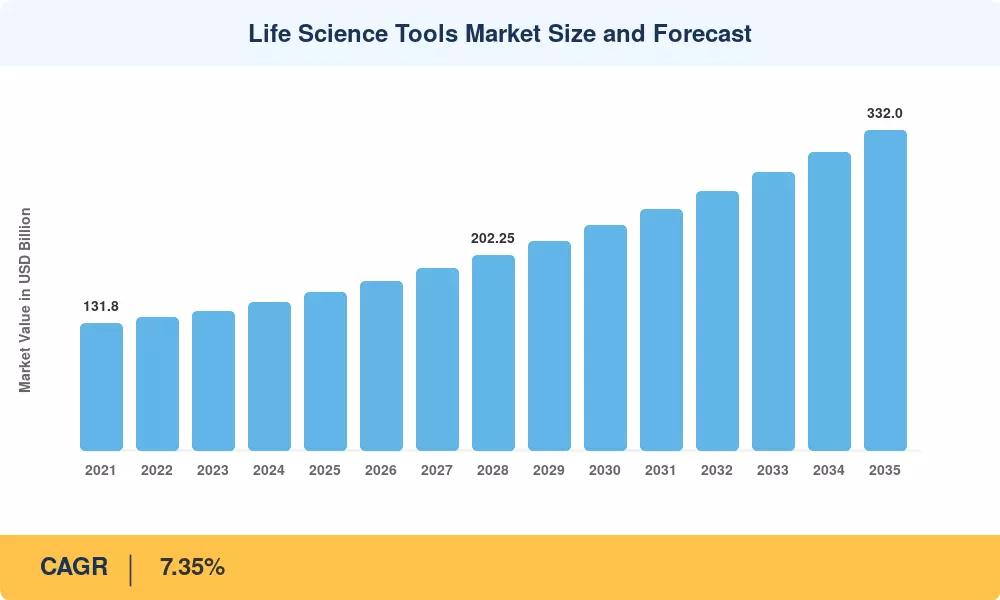

The Global Life Science Tools Market size was valued at USD 163.50 Billion in 2025, and the market is projected to grow from USD 175.50 Billion in 2026 to USD 332.00 Billion by 2035, registering a CAGR of 7.35% during the forecast period 2026–2035. Government-led funding packages — including a proposed USD 88 billion biotechnology allocation by the United States Congress for 2025 — are channeling fresh capital into validated instruments, sequencing platforms, and compliance-ready consumables [1]. Stricter FDA oversight of lab-developed tests is simultaneously creating new procurement cycles across hospital networks and reference laboratories, adding a regulatory tailwind to an already expanding life science tools market.

Automated high-throughput platforms combining robots, microfluidics and artificial intelligence–driven data interpretation are replacing manual bench operations, and the way we do things is changing dramatically. In clinical contexts, the cost of per-genome sequencing has dropped to USD 200, allowing next-generation sequencing to become available to community hospitals and mid-tier diagnostic chains that have relied on outsourced testing up until now [2]. The use of multi-omics, or the combination of genomic, proteomic, and metabolomic readouts in a single pipeline, is driving higher equipment refresh rates, particularly in academic medical institutes that receive grants from the NIH and Horizon Europe [3].

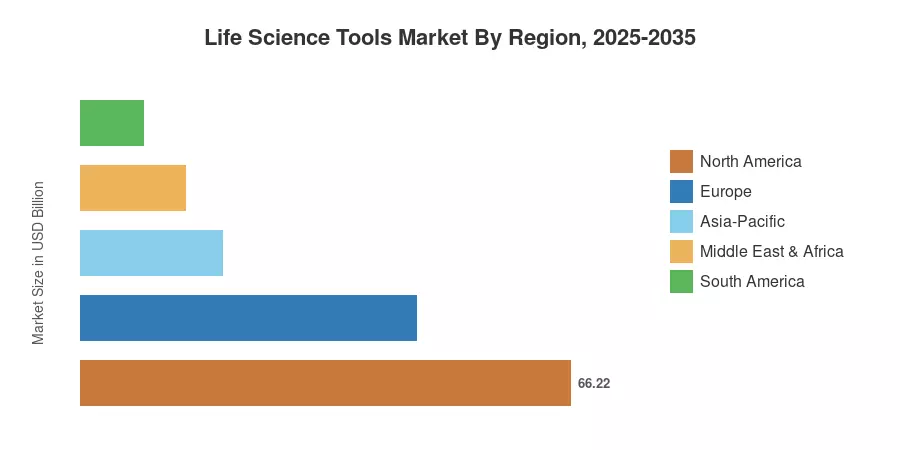

With continued federal research support and a large installed base of analytical equipment, North America is the largest market for life science tools, representing around 40.5% of the total. The Asia-Pacific area is predicted to be the fastest-growing region with a CAGR of 11.75% due to the growth of biotech parks in China and the Production-Linked Incentive program for medical devices in India [4]. Europe maintains the second-highest proportion of 27.8%, driven by the EU’s Innovative Health Initiative and state genomic-medicine projects. The life science instruments market is expected to continue double-digit growth in high-growth areas through 2035 as precision medicine continues to revolutionize clinical and research processes.

Key Report Takeaways

• By Type

- Services recorded the fastest expansion at a 12.15% CAGR (2026–2035), as laboratories pivot to outsourced validation and pay-per-use models that lower capital expenditure barriers.

- Instruments retained a 46.5% share of the life science tools market in 2025, reflecting strong demand for next-generation sequencing and mass spectrometry platforms.

• By Technology

- Next-generation sequencing expanded at an 18.2% CAGR, fueled by falling per-genome costs and broadening clinical utility.

- PCR & qPCR led the life science tools market with a 24.2% technology share in 2025, sustained by infectious-disease surveillance and molecular diagnostics.

• By Application

- Proteomics technology advanced at a 14.1% CAGR as drug developers increasingly adopt mass spectrometry–based biomarker discovery.

- Genomic technology accounted for 35.4% of the life science tools market in 2025.

• By End User

- Diagnostic laboratories grew the fastest at a 12.75% CAGR, propelled by LDT regulation and point-of-care testing expansion.

- Research laboratories held 62.0% of the life science tools market in 2025.

• By Geography

- Asia-Pacific posted the highest regional CAGR of 11.75%, while North America remained the dominant region with 40.5% share.

Life Science Tools Market Size and Forecast (2021–2035)

Market size estimates are derived from bottom-up revenue modelling spanning instruments, consumables and services and cross-validated top-down with publicly published firm revenues and government expenditure data. Historical numbers are yearly reports of major suppliers, and projected predictions are capital-expenditure surveys, grant-funding pipelines, and regulatory-impact studies.