Light Therapy Market Summary

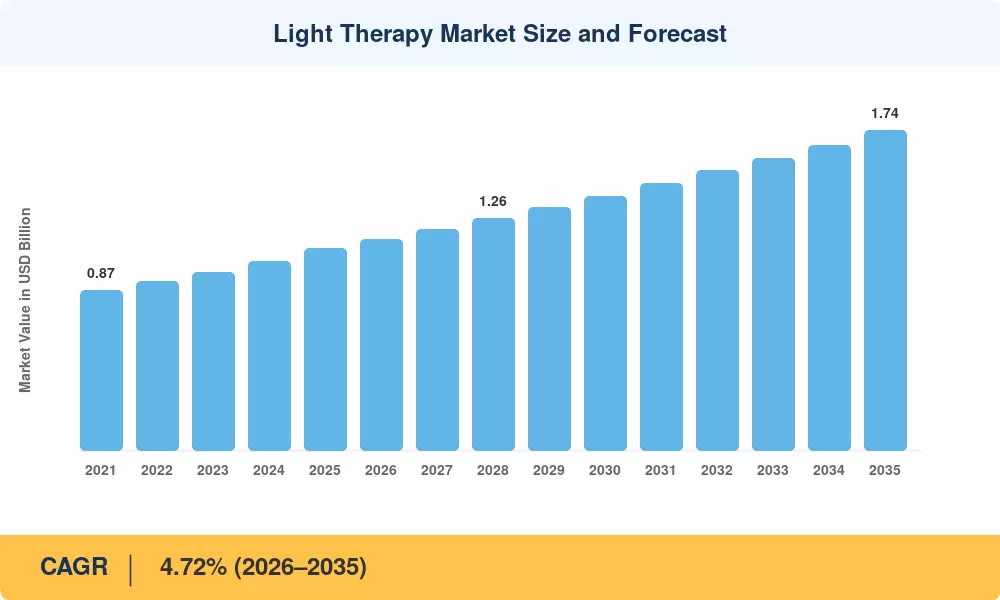

The Global Light Therapy Market size was valued at USD 1.10 Billion in 2025, and the market is projected to grow from USD 1.15 Billion in 2026 to USD 1.74 Billion by 2035, registering a CAGR of 4.72% during the forecast period 2026–2035. Clinical validation across dermatology, psychiatry, and ophthalmology continues to propel adoption. The FDA's 2024 authorization of the Valeda Light Delivery System for dry age-related macular degeneration represented a pivotal regulatory inflection point, catalyzing renewed investment into device development and reimbursement pathway expansion [1].

The Light Therapy Market is undergoing a paradigm transition as classic fluorescent-based phototherapy systems are being replaced by modern LED platforms that provide targeted wavelength output at a fraction of legacy power usage. The LITE randomized controlled trial showed that home narrowband UV-B phototherapy is non-inferior to clinic-based treatment for chronic plaque psoriasis, validating a decentralized care model that could redirect more than USD 450 million in annual clinic-based spending to home-use devices by 2030 [2]. Since 2021, LED component costs have fallen by 18%, enabling device makers to deliver consumer-friendly price points without compromising therapeutic efficacy.

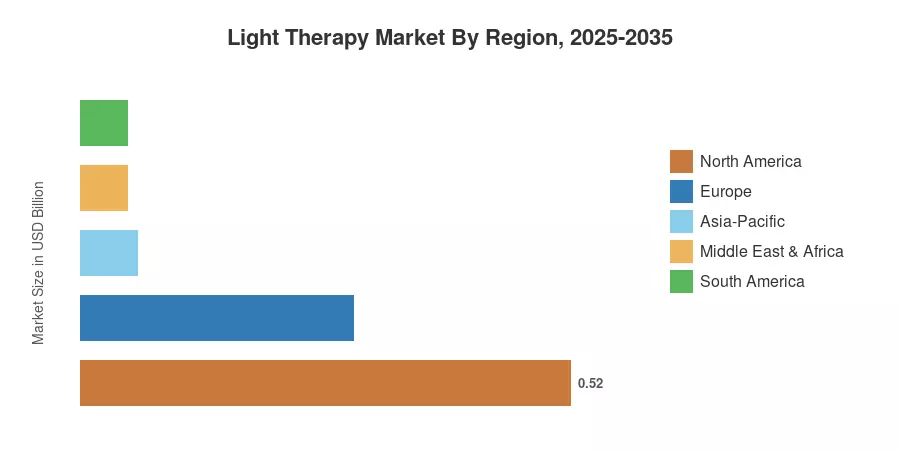

North America accounts for 47.4% of the Light Therapy Market, driven by strong insurance reimbursement policies and high per capita spending on dermatology. The Asia-Pacific region is the fastest-growing market with a CAGR of 5.39% through 2035, fueled by the increasing demand for cosmetic operations from the middle class in China, India and South Korea. Europe has the second-largest proportion of the market, with over 26.0%, with a robust public health system and increased awareness of Seasonal Affective Disorder in Nordic nations. The Light Therapy Market is poised for long-term growth across all geographies till the end of the decade and beyond, with telehealth integration and AI-driven dosimetry coming of age.

Key Report Takeaways

• By Product Type

- Light Boxes led the Light Therapy Market in 2025, capturing a 29.1% revenue share, driven by widespread adoption for mood disorder management and clinical dermatology applications.

- Hand-held Devices are poised to expand at a 5.20% CAGR through 2035 as portable, app-connected units gain traction among home-care users seeking targeted treatment convenience.

• By Light Type

- Blue light wavelength platforms accounted for 37.9% of the Light Therapy Market revenue in 2025, reflecting strong demand from acne treatment and circadian rhythm regulation applications.

- Red light platforms are forecast to grow at a 5.08% CAGR to 2035, fueled by expanding evidence for wound healing and anti-aging skin rejuvenation protocols.

• By Application

- Skin Disorders represented the largest application segment, holding 31.8% of the Light Therapy Market in 2025.

- Depression & Sleep-Cycle Disorders are advancing at a 5.30% CAGR through 2035, supported by rising mental health awareness and SAD lamp therapy adoption.

• By End User

- Dermatology Clinics held 43.2% of the Light Therapy Market revenue in 2025.

- Home-care Settings are projected to rise at a 5.34% CAGR to 2035 as patient preference shifts toward decentralized phototherapy.

• By Geography

- North America commanded the dominant regional position in the Light Therapy Market with a 47.4% revenue share in 2025.

- Asia-Pacific represents the fastest-growing region at a 5.39% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market size is determined using bottom-up device shipping data, clinical reimbursement data, and distributor channel audits across 32 countries, using the sizing approach of Market Research Future (MRFR). Historical values are benchmarked against regulatory clearance databases and reported clinical adoption rates. At the same time, forecast predictions are based on segment-weighted growth assumptions established through primary interviews with dermatologists, device OEMs, and hospital procurement officers.