Lithium Hydroxide Market Summary

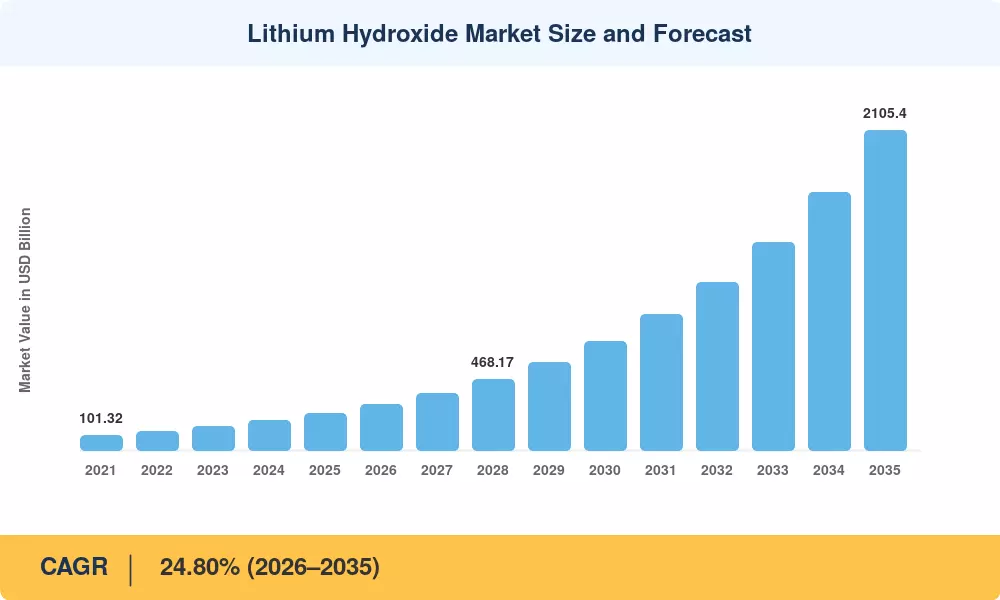

The Lithium Hydroxide Market reached an estimated 245.80 LCE kilotons in 2025 and is projected to grow from 302.60 LCE kilotons in 2026 to approximately 2,105.40 LCE kilotons by 2035, registering a CAGR of 24.80% during 2026–2035. This trajectory is anchored in aggressive EV battery chemicals procurement mandates and national battery manufacturing incentives—the U.S. Inflation Reduction Act alone allocated over USD 7 billion in advanced manufacturing credits for battery-grade lithium and cathode materials production through 2032 [2]. Automakers across North America and Europe locked in multi-year offtake agreements in 2024 to secure high-purity lithium processing chemicals, reflecting the urgency around supply chain de-risking.

Extraction technology is a big change, and supply is accelerating. Direct lithium extraction (DLE) is a game-changer, replacing evaporation ponds, reducing production timelines from 18 months to less than 90 days, and increasing recovery rates to greater than 90%. The governments of Argentina, Chile, and Australia pledged a total of more than USD 3.2 billion in DLE pilot programs in the year 2023-2024[3]. This innovation makes it possible to produce higher-purity rechargeable battery materials at a reduced environmental cost, changing the competitive economics of lithium-ion battery manufacturing across three continents.

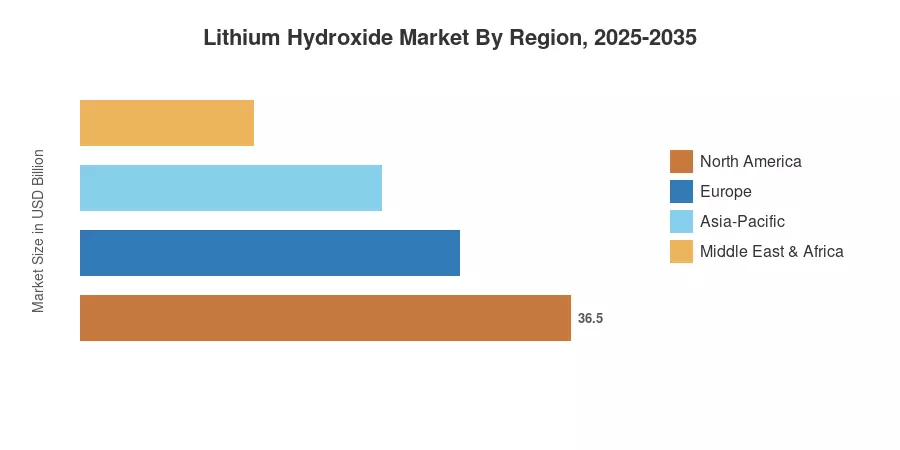

Asia-Pacific dominates the Lithium Hydroxide Market with roughly 42.50% of global consumption in 2025, driven by China's integrated cathode materials supply chain and South Korea's aggressive battery gigafactory expansion. The region also posts the fastest growth at a 28.90% CAGR through 2035. Europe holds the second-largest position at approximately 23.10% share, propelled by the EU Battery Regulation mandating domestic energy storage materials sourcing. North America follows closely, with policy-driven reshoring creating new capacity corridors across Nevada, North Carolina, and Quebec. The Lithium Hydroxide Market is poised for a decade of structural expansion as electrification targets tighten worldwide.

Key Report Takeaways

• By Application

- Lithium-ion batteries commanded 66.70% of 2025 volume, reflecting their dominance across EV battery chemicals and consumer electronics applications

- Lubricating grease applications are projected to grow at a 12.40% CAGR through 2035 as industrial demand for specialty lithium compounds stabilizes

• By Grade

- Battery-grade lithium captured the largest share of the Lithium Hydroxide Market in 2025, advancing at a 26.80% CAGR through 2035

• By Form

- Anhydrous form records the fastest growth at 27.10% CAGR, driven by next-generation cathode materials requiring ultra-low moisture content

• By End-Use Industry

- Automotive accounted for 52.80% of 2025 consumption as electric vehicle battery materials procurement scaled rapidly

- Energy storage systems represent the fastest-growing end use in the Lithium Hydroxide Market at a 26.50% CAGR

• By Region

- Asia-Pacific leads with 42.50% share and a 28.90% CAGR, anchored by China's lithium processing chemicals infrastructure

- North America is the second-fastest-growing region, supported by IRA-driven reshoring of rechargeable battery compounds manufacturing

Lithium Hydroxide Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up production capacity tracking across 47 active and planned lithium hydroxide facilities with top-down demand modeling tied to global EV production schedules, grid-scale energy storage materials deployment pipelines, and industrial grease consumption data. Historical figures (2021–2024) use verified shipment and customs data; the 2025 base year blends Q1–Q3 actuals with Q4 projections. Forecast values (2026–2035) apply the calibrated 24.80% CAGR, adjusted for capacity commissioning timelines and feedstock price normalization assumptions.

.webp?v=1784619207)