Lupus Market Summary

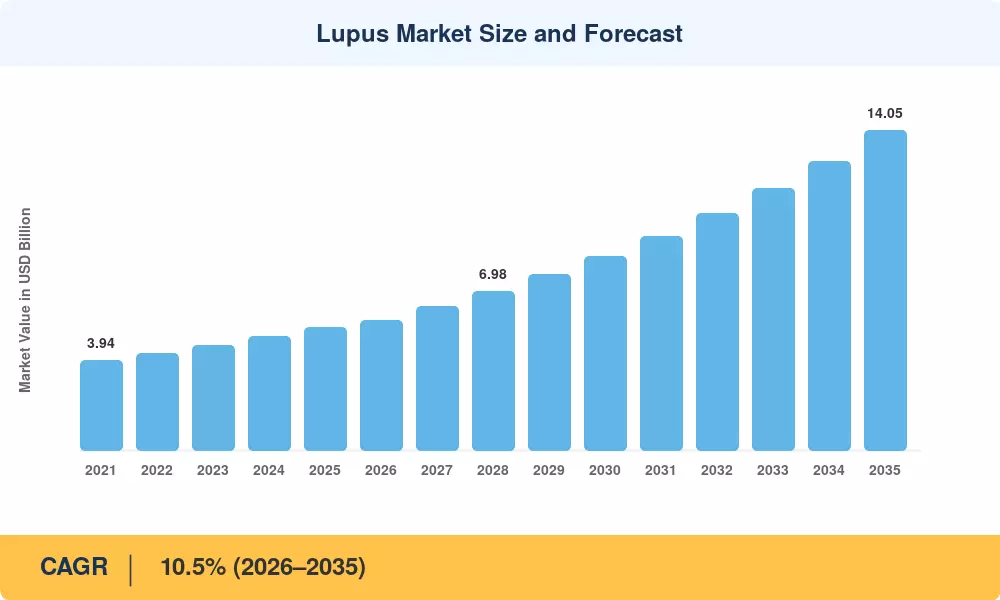

The Lupus Market size was valued at USD 5.40 Billion in 2025, and the market is projected to grow from USD 5.72 Billion in 2026 to USD 14.05 Billion by 2035, registering a CAGR of 10.5% during the forecast period 2026–2035. This expansion reflects a decisive shift in how autoimmune conditions are treated — away from broad-spectrum immunosuppression and toward targeted biologics that preserve organ function. The FDA's October 2025 approval of obinutuzumab for renal involvement in lupus marked a watershed for advanced therapies, while the 2025 American College of Rheumatology (ACR) guidelines formalized an aggressive steroid-sparing treatment philosophy that is reshaping prescribing habits across specialty clinics and hospitals [1][2].

The Lupus Market is undergoing a pronounced technology transition. Legacy corticosteroid-heavy regimens are giving way to precision biologics — B-cell depleting agents, type I interferon inhibitors, and calcineurin-targeted molecules — that offer more durable disease control with fewer systemic side effects. Cumulative biopharma investment in lupus pipeline assets exceeded USD 4.8 Billion between 2021 and 2025, underscoring the commercial conviction behind next-generation therapies [3]. Self-administration formulations and specialty pharmacy distribution networks are further disrupting the traditional hospital-infusion delivery model, reducing per-patient administration costs by an estimated 18–22% [4].

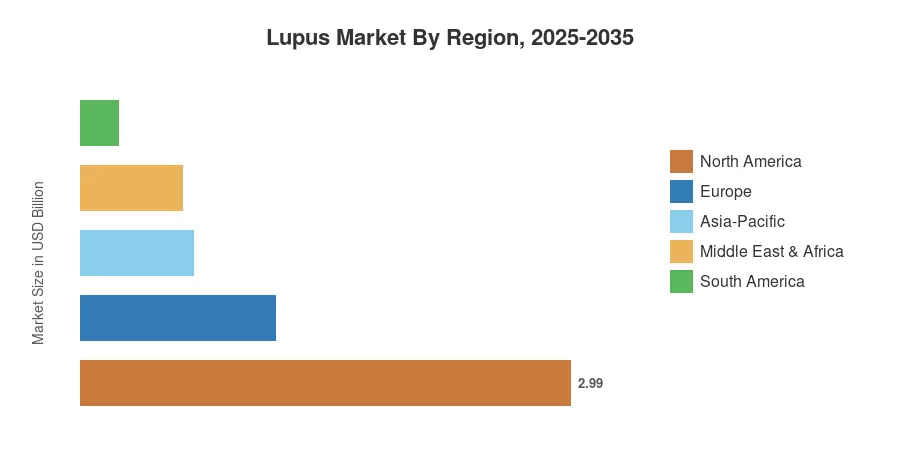

North America commands roughly 55.3% of the global Lupus Market, driven by established biologic reimbursement frameworks and high specialty diagnostic penetration. Asia-Pacific stands as the fastest-growing region at a projected 12.7% CAGR through 2035, propelled by expanding insurance coverage programs across China, India, and ASEAN nations. Europe represents the second-largest geography with approximately a 22.1% share, anchored by the UK, Germany, and France [5]. The next decade will be defined by competition among biologic originators, biosimilar entrants, and novel small-molecule candidates vying for therapeutic positioning across disease subtypes.

Key Report Takeaways

• By Disease Type

- Systemic lupus erythematosus (SLE) accounted for approximately 80.5% of the Lupus Market in 2025, reflecting its higher prevalence and broader treatment infrastructure.

- Cutaneous lupus erythematosus (CLE) is anticipated to expand at a CAGR of 11.7% through 2035, fueled by increased dermatologic awareness and dedicated diagnostic pathways.

• By Treatment and Diagnosis

- The treatment sub-segment captured roughly 65.3% of the Lupus Market in 2025, with biologics gaining share at the expense of conventional corticosteroid regimens.

- The diagnosis sub-segment is projected to grow at a 12.1% CAGR through 2035, supported by advanced laboratory testing adoption and specialty biopsy services.

• By End User

- Hospitals held approximately 38.5% of the Lupus Market in 2025, although their share is gradually declining as infusion therapies migrate to outpatient and home settings.

- Home care settings are projected to expand at a 12.7% CAGR through 2035, reflecting the availability of subcutaneous biologic formulations.

• By Region

- North America accounted for an estimated 55.3% of the global Lupus Market in 2025.

- Asia-Pacific is expected to register the highest regional CAGR of 12.7% through 2035, with China and India leading capacity expansion.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up pharmaceutical sales tracking, specialty pharmacy distribution data, payer reimbursement analytics, and prescription volume modeling across more than 40 countries. Historical estimates are triangulated against company-reported revenues and national disease registries, while forecast projections incorporate pipeline probability-adjusted sales and regulatory approval timelines.