Maritime Patrol Aircraft Market Summary

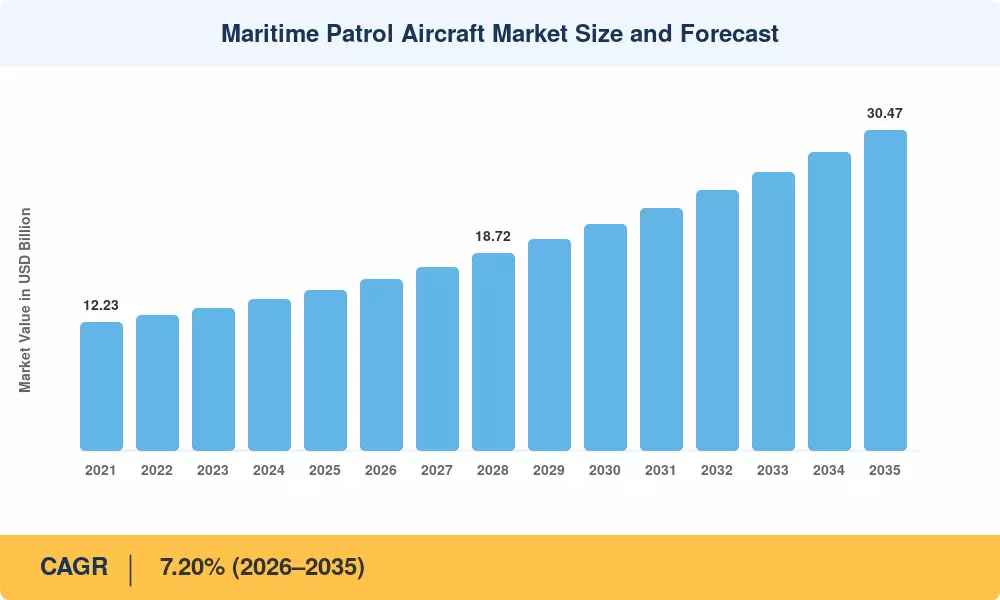

The Maritime Patrol Aircraft Market reached USD 15.20 billion in 2025 and is projected to climb from USD 16.29 billion in 2026 to USD 30.47 billion by 2035, registering a 7.20% CAGR across the forecast window. Accelerating submarine proliferation — particularly diesel-electric and nuclear-powered platforms in the Indo-Pacific — has compelled allied navies to fast-track procurement of next-generation patrol fleets. Simultaneously, the expansion of Exclusive Economic Zone enforcement under UNCLOS mandates is channeling defense budgets toward persistent airborne surveillance [1][2]. The Maritime Patrol Aircraft Market is thus underpinned by both hard-security imperatives and blue-economy governance needs.

A generational technology shift defines this decade. Cold War-era Lockheed P-3 Orions and British Aerospace Nimrods are cycling out in favor of platforms built around commercial airframes loaded with open-architecture mission systems. Boeing's P-8A Poseidon program alone has captured orders exceeding USD 50 billion cumulatively, while European nations are pivoting to Airbus C-295 MPA variants and next-generation unmanned adjuncts [3]. Modular sensor pods, synthetic-aperture radar, and AI-driven sonobuoy processing are replacing legacy analog suites, cutting maintenance costs and boosting mission flexibility.

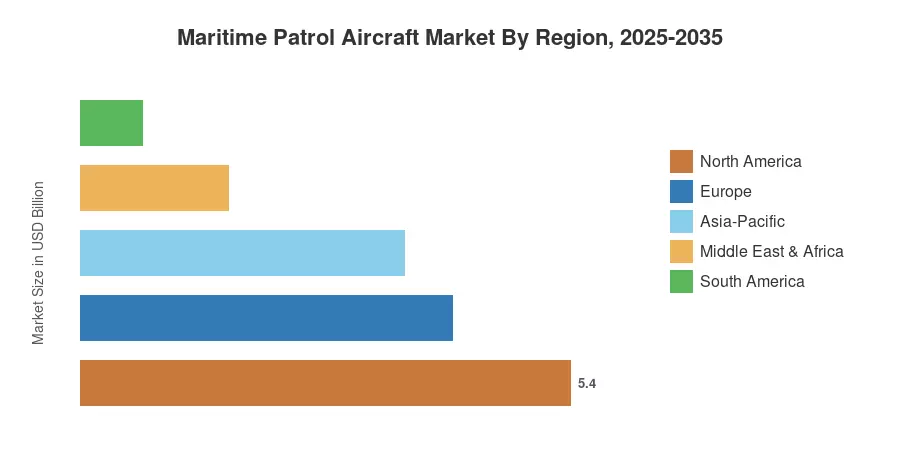

North America commands roughly 35.50% of the Maritime Patrol Aircraft Market, driven by the US Navy's multi-year P-8A production line and allied Foreign Military Sales. The Middle East & Africa region is the fastest-growing with a projected 10.75% CAGR to 2035, fueled by coastal-state investments in counter-piracy and irregular maritime threat detection. Europe holds the second-largest share at approximately 27.00%, anchored by NATO interoperability programs and German-Norwegian-French procurement cycles [4][5]. As manned-unmanned teaming matures, the Maritime Patrol Aircraft Market is poised for an inflection point that will reshape competitive dynamics through the early 2030s.

Key Report Takeaways

• By Platform

- Manned aircraft held approximately 79.60% of the Maritime Patrol Aircraft Market in 2025, reflecting continued reliance on crew-operated, multi-mission airframes.

- Unmanned systems posted the fastest platform CAGR at 10.45% through 2035, propelled by persistent-surveillance programs such as the MQ-4C Triton.

• By Propulsion

- Jet-powered platforms dominated revenue with a 79.10% share in 2025, anchored by twin-engine commercial-derivative designs.

- Electric and hybrid-electric propulsion is advancing at a 12.70% CAGR as prototype demonstrators enter flight-test phases in the Maritime Patrol Aircraft Market.

• By Mission

- Anti-submarine warfare accounted for 48.90% of spending in 2025, driven by submarine-fleet expansion among peer and near-peer navies.

- Border and EEZ patrol is emerging as the fastest-growing mission type at an 8.70% CAGR through 2035.

• By End User

- Naval forces led with a 57.95% revenue share in 2025 across the Maritime Patrol Aircraft Market.

- Coast guards recorded the highest end-user CAGR at 12.85% as maritime-security budgets expand beyond traditional defense ministries.

• By Region

- North America commanded a 35.50% share of the Maritime Patrol Aircraft Market in 2025.

- The Middle East & Africa region is projected to advance at a 10.75% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future derives historical values from verified defense-procurement databases, manufacturer delivery records, and government contract filings. Forecast projections apply a bottom-up build combining platform unit economics, fleet-replacement schedules, and regional defense-spending trajectories, cross-validated with top-down macroeconomic indicators.

.webp?v=1784638972)