Medical Alert Systems Market Summary

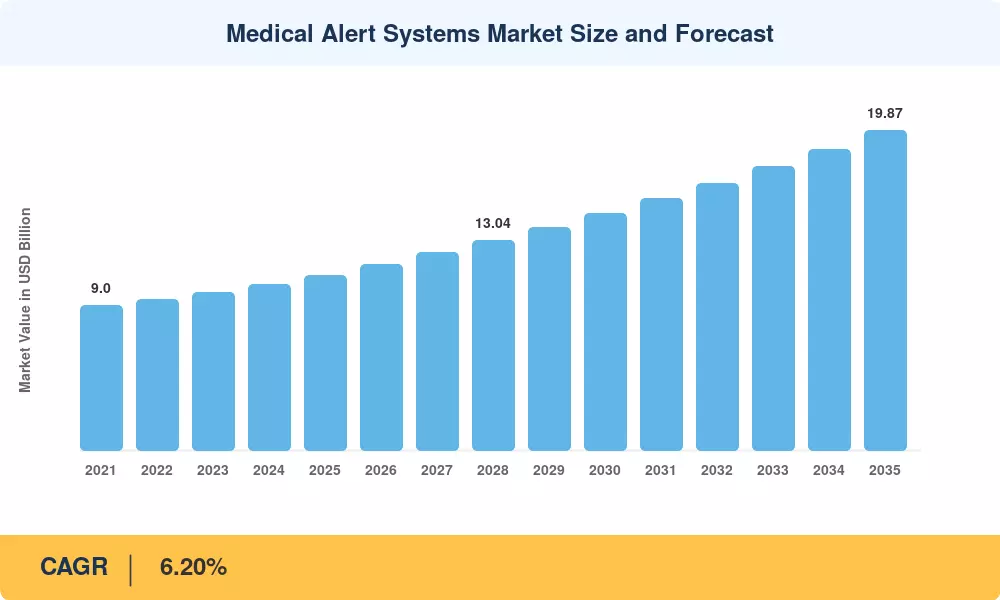

The Medical Alert Systems Market reached USD 10.89 Billion in 2025 and is projected to climb to USD 19.87 Billion by 2035, registering a 6.20% CAGR across the 2026–2035 forecast window. Two intersecting forces are accelerating adoption: Medicare Advantage plan expansions that now reimburse personal emergency response hardware as a supplemental benefit, and employer duty-of-care mandates requiring lone-worker monitoring across oil-and-gas, utilities, and home-healthcare sectors [1]. These policy catalysts convert what was once a consumer-pay niche into a payer-funded growth channel with predictable subscription economics.

Technology-wise, the Medical Alert Systems Market is transitioning from legacy landline-tethered units to cellular- and GPS-enabled platforms that pair with voice assistants and remote patient monitoring hubs. Vendors are investing heavily in 4G LTE base stations and cloud-hosted triage dashboards; an estimated USD 1.3 billion in cumulative R&D flowed into connected PERS hardware between 2022 and 2024 [2]. This shift allows insurers to quantify avoided emergency-department visits, creating a measurable ROI narrative that broadens reimbursement eligibility.

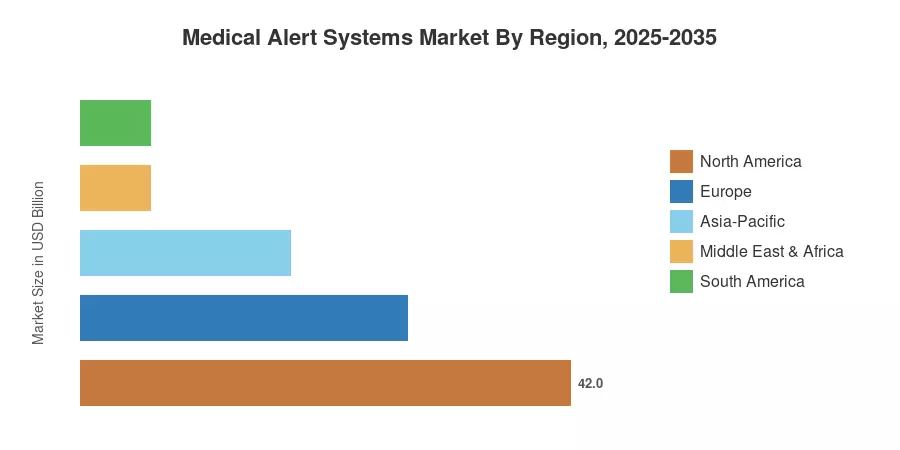

North America commands roughly 42% of global revenue, anchored by the United States' large Medicare-eligible population and well-established monitoring-center infrastructure. Asia-Pacific represents the fastest-growing region at a projected 7.45% CAGR, driven by Japan's super-aged demographics and China's expanding community-care pilot programs [3]. Europe holds the second-largest share near 28%, underpinned by the United Kingdom's NHS telecare contracts and Germany's aging-in-place subsidies. As 5G rollouts compress alert-to-dispatch latency below five seconds, the Medical Alert Systems Market is positioned for a decade of compounding growth.

Key Report Takeaways

• By Type

- Landline PERS accounted for 52.1% of the Medical Alert Systems Market share in 2025, sustained by an installed base of home-based subscribers on copper networks.

- Mobile PERS is expected to register a 6.52% CAGR through 2035, powered by cellular miniaturization and caregiver-app integration.

• By End User

- Hospitals and clinics represented 56.9% of the Medical Alert Systems Market revenue in 2025, reflecting institutional procurement cycles.

- Senior housing and assisted living facilities are forecast to expand at a 6.85% CAGR, driven by regulatory mandates for on-premises emergency response.

• By Region

- North America generated USD 4.57 billion in 2025 revenue, led by the United States' Medicare supplemental benefit programs.

- Asia-Pacific is projected to achieve a 7.45% CAGR through 2035.

Medical Alert Systems Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated approach combining bottom-up revenue modeling from device-shipment databases, top-down validation against payer-reimbursement records, and primary interviews with monitoring-center operators across 22 countries.