Medical Devices Market Summary

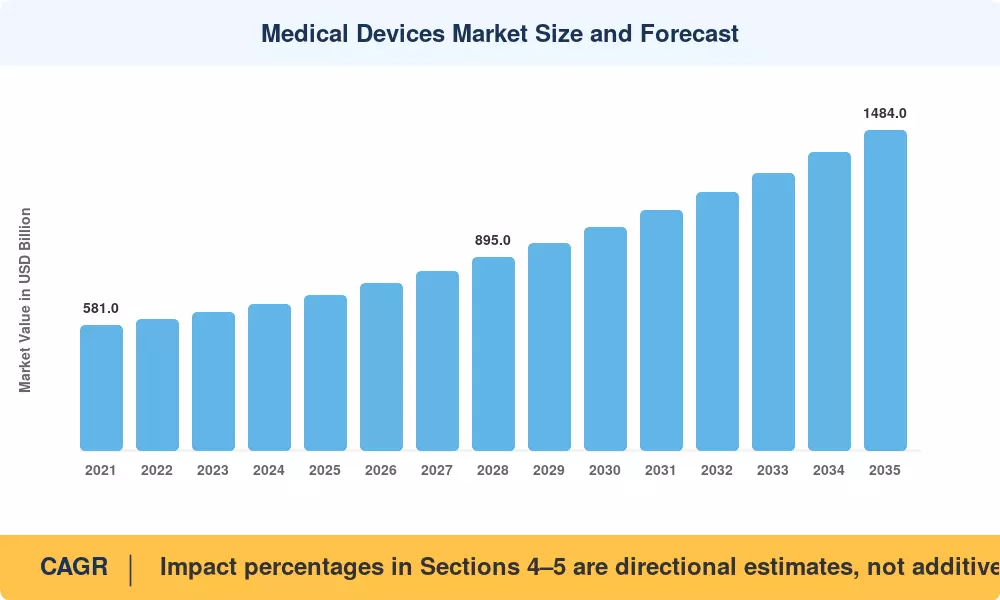

The Medical Devices Market reached an estimated USD 720 billion in 2025 and is projected to grow from USD 774 billion in 2026 to USD 1,484 billion by 2035, registering a CAGR of 7.5% across the forecast window. Two catalysts are reshaping capital allocation in this space: the U.S. Centers for Medicare & Medicaid Services expanded reimbursement for remote patient monitoring codes in 2024, unlocking billions in connected-sensor revenue, while the EU Medical Device Regulation (MDR) enforcement deadlines are compelling manufacturers to re-certify legacy portfolios — an exercise that alone is estimated to cost the European industry over EUR 10 billion cumulatively [1][2].

A technology inflection is well underway. Legacy electro-mechanical platforms that dominated hospital procurement for decades are giving way to AI-embedded diagnostics, miniaturized wearable sensors, and nanocoating-enabled implantables. The U.S. FDA cleared 168 machine-learning-enabled devices in 2024, with the vast majority routed through the 510(k) pathway — a signal that algorithmic diagnostics have crossed from pilot programs into standard-of-care procurement [3]. Hospital-at-home programs and ambulatory surgical centers are creating entirely new endpoints of care that demand smaller, smarter, and more connected device architectures.

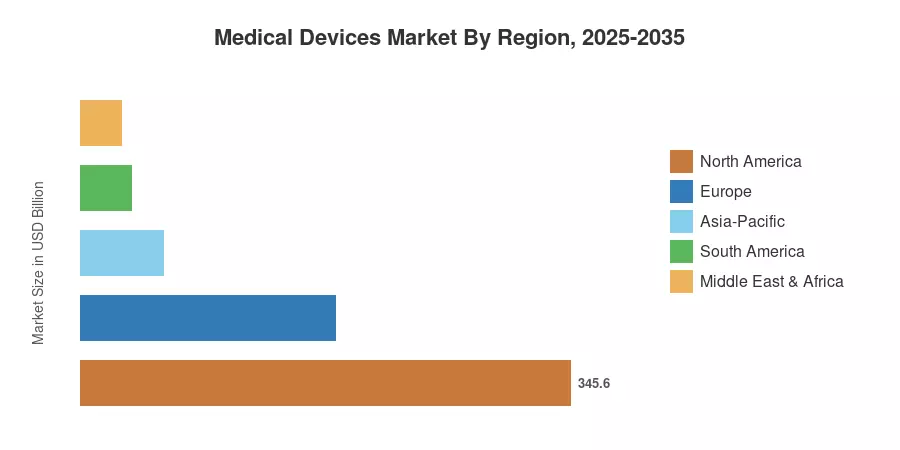

North America commands roughly 48% of the Medical Devices Market, driven by the world's highest per-capita device spending and a mature reimbursement infrastructure. Asia-Pacific carries the strongest growth trajectory at an 8.1% CAGR to 2035, fueled by rising insurance penetration in India, medtech manufacturing expansion in China, and Japan's robotics-led surgical automation push. Europe holds the second-largest share, near 25%, anchored by Germany, France, and the UK. As demographic aging accelerates globally and surgical volumes recover post-pandemic, the Medical Devices Market is positioned for sustained double-digit capital inflows through the mid-2030s.

Key Report Takeaways

• By Device Type

- Diagnostic Devices held approximately 42% of the Medical Devices Market in 2025, led by advanced imaging modalities and point-of-care testing platforms.

- Monitoring Devices are expanding at a 7.8% CAGR through 2035, propelled by continuous glucose monitors and remote cardiac telemetry.

• By Technology Platform

- Conventional Electro-mechanical & Disposable systems accounted for 60% of the Medical Devices Market share in 2025.

- Nanotechnology & Smart Materials are advancing at an 8.7% CAGR to 2035, addressing infection-resistant coatings and drug-eluting implant surfaces.

• By Therapeutic Area

- Cardiology retained a 24% share of the Medical Devices Market in 2025, reflecting sustained demand for interventional and structural heart devices.

- Neurology is growing fastest at an 8.2% CAGR to 2035, supported by neuromodulation and brain-computer interface development.

• By End User

- Hospitals controlled 61% of device procurement in 2025.

- Ambulatory Surgical Centers are projected to grow at 8.6% through 2035 as outpatient procedure volumes increase.

• By Region

- North America captured 48% of the Medical Devices Market revenue in 2025.

- Asia-Pacific carries the highest forecast CAGR at 8.1% to 2035.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework triangulates revenue data from company filings, import-export records, regulatory clearance databases, and hospital procurement disclosures. Historical figures (2021–2024) reflect audited actuals where available; the base year (2025) incorporates preliminary H2 run-rate extrapolations. Forecast values (2026–2035) apply a calibrated compound growth model validated against macroeconomic health expenditure projections from the WHO and OECD [4][5].