Refurbished Medical Devices Market Summary

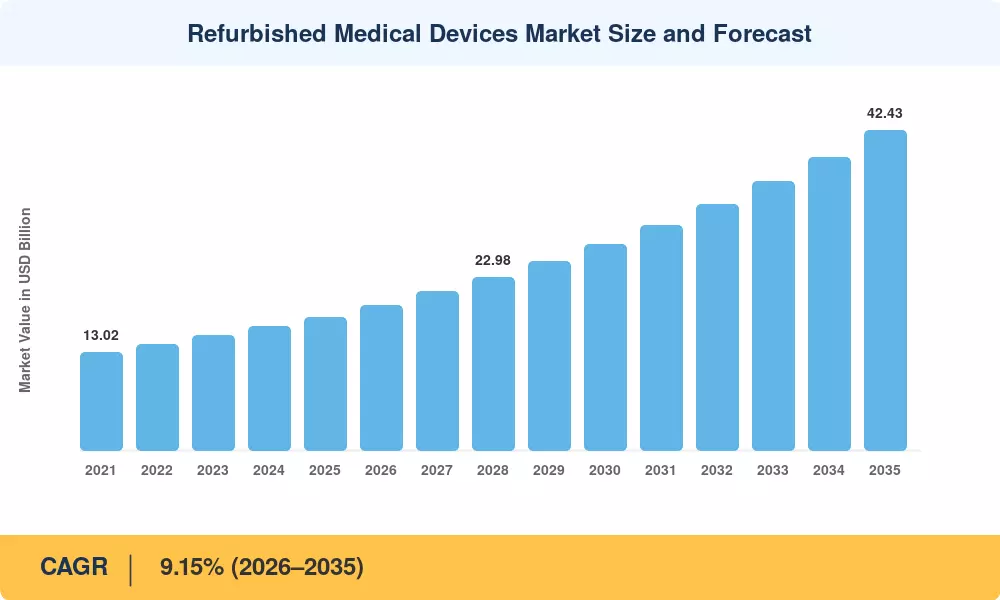

The Refurbished Medical Devices Market size was valued at USD 17.67 Billion in 2025, and the market is projected to grow from USD 19.29 Billion in 2026 to USD 42.43 Billion by 2035, registering a CAGR of 9.15% during the forecast period 2026–2035. Two catalysts are driving this trajectory: persistent hospital capital budget pressures that push procurement teams toward certified second-life equipment, and a wave of government green-procurement mandates — the EU Medical Device Regulation (MDR 2017/745) revision cycle and the U.S. FDA's expanded guidance on refurbishment standards — that legitimize the secondary equipment channel [1][2].

A generational technology refresh is underway across diagnostic imaging and surgical suites. Hospitals replacing analog X-ray and single-slice CT systems are finding that refurbished 64-slice CT scanners and 1.5T MRI units deliver 85–90% of new-unit performance at 40–55% lower acquisition cost. The World Health Organization estimated that low- and middle-income countries face a USD 40 billion annual deficit in medical device access, and refurbished channels are absorbing a growing share of that gap [3][4].

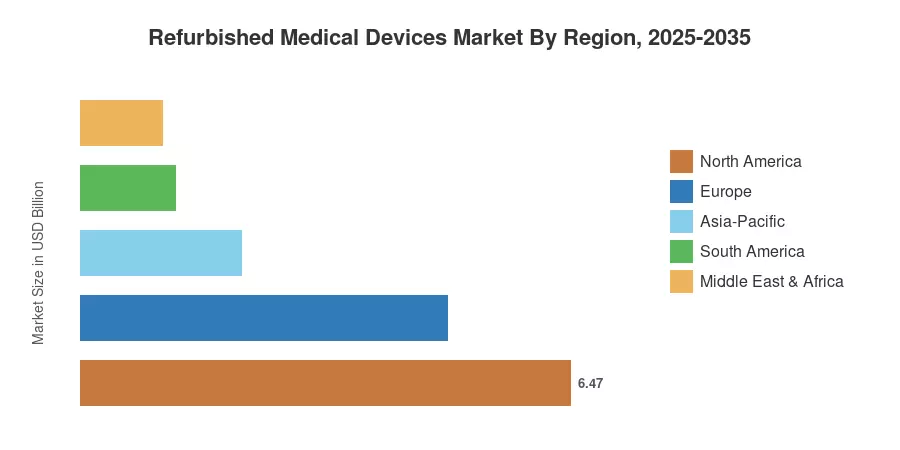

North America commands roughly 36.6% of the Refurbished Medical Devices Market, anchored by established OEM refurbishment programs from GE HealthCare and Siemens Healthineers. Asia-Pacific is the fastest-growing region at a 12.01% CAGR through 2035, propelled by India's Ayushman Bharat hospital modernization initiative and China's county-hospital equipment upgrade cycle. Europe holds the second-largest position with a 27.4% share, reinforced by NHS procurement frameworks that actively score sustainability credentials. As digital auction platforms and AI-driven equipment grading mature, the Refurbished Medical Devices Market is poised to evolve from a cost-saving alternative into a mainstream procurement channel.

Key Report Takeaways

• By Product Category

- Medical imaging equipment held 36.6% of the Refurbished Medical Devices Market in 2025, reflecting steady demand for CT, MRI, and ultrasound systems across hospital networks.

- Operating room and surgical equipment is forecast to expand at a 12.56% CAGR through 2035, driven by ambulatory surgical center build-outs in emerging economies.

• By Refurbishment Provider

- OEM-certified channels accounted for a 59.3% share of the Refurbished Medical Devices Market in 2025, benefiting from brand trust and integrated service contracts.

- Independent and in-house refurbishers are growing at an 11.39% CAGR, targeting underserved geographies with faster turnaround times.

• By End User

- Hospitals represented USD 10.34 billion of the Refurbished Medical Devices Market in 2025, underscoring their role as the primary demand anchor.

- Ambulatory surgical centers are advancing at a 12.24% CAGR through 2035, as outpatient procedure volumes shift outside traditional hospital walls.

• By Region

- North America commanded 36.6% of the Refurbished Medical Devices Market in 2025, led by mature OEM programs in the United States.

- Asia-Pacific is projected to post the fastest 12.01% CAGR between 2026 and 2035, fueled by government-backed hospital infrastructure investments.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up revenue analysis from OEM refurbishment divisions, independent refurbisher financials, customs trade data on second-hand medical equipment, and validated hospital procurement surveys across 42 countries. Historical data (2021–2024) reflects audited company filings and WHO medical device trade databases, while the forecast period (2026–2035) applies econometric modeling calibrated against healthcare capital expenditure projections.